The latest version of the November Moss Adams report was inaccurate, delivered no value and provides even more evidence for why full forensic and performance audits are needed on the Capital Improvement Program. This doesn’t even take into account the version of the Moss Adams report that was given to the Board in November that was rife with literally dozens of errors.

For months the expectations were set that the Moss Adams report would give the Board and district an accurate number for the amount of money remaining in the Capital Improvement Program. Ideally, this number would have tied directly back to the monthly CAAC report and even better, it would have provided totals of how much has been spent on each school. The Moss Adams report achieved none of these expectations. Instead, what the Board got was a rambling 73 page document and a meaningless “$74M Remaining to be Committed” number.

That $74M “Remaining to be Committed” number was meaningless for a number of reasons:

- It was 7 months old and was not accompanied by a staff reconciliation to bring it up-to-date

- It was an aggregate remaining capital funds number and did not separate out CIP funds from regular Capital Reserve Fund funds

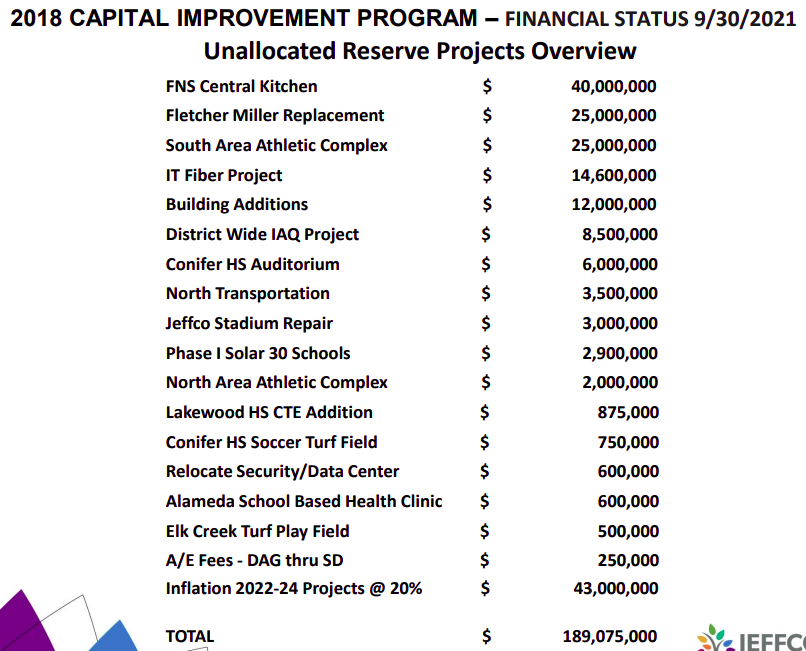

- It did not factor in CIP committed projects that have not yet been started and entered into the district’s financial systems. For instance, until a formal decision is made otherwise, Jeffco is still committed to building 2 new elementary schools, for which Tim Reed has allocated $59.6M. These are accounted for in the CAAC report, but not the Moss Adams report. In addition, the Moss Adams report did not account for the $10M in upgrades for Bergen Valley for ROTS I or many other unstarted projects.

- The report contained errors and its methodology did not align with the manner in which Tim Reed develops the monthly CAAC report. For instance, page 17 of the report lists a Meyers Pool project at more than $500k as a “School-Specific Project”. That is absolutely incorrect and calls into question the accuracy and validity of every other single number in the report.

A reasonable expectation would have been that Jeffco staff would have taken this report and reconciled it with the CAAC report to identify if there were any discrepancies and to arrive at exactly how much money was currently left in the bond program. Shockingly, that didn’t happen. The response I received when I asked for that reconciliation as part of CORA Request PR-2324-177 was the following:

Our subject matter expert provided that the transaction level detail that we’ve already shared with you is drawn directly from the accounting system – which is the same system driving the CAAC reports.

If there was no reconciliation, what was the purpose of the Moss Adams review? What exactly did Jeffco schools get out of the close to $200k that Moss Adams was paid?

Second, there were several discrepancies between the Moss Adams report and the CAAC report. Yes, I realize that the Moss Adams report was conducted from a point in time, but my examples transcend the time issue. Note also that I only looked at approximately 25 projects that were listed as “100%” on the April 2023 CAAC report, the month Moss Adams used as their baseline.

- Moss Adams identified $185,156 in actual expenditures for the Sheridan Green ES FF&E project. Yet, from at least March 2023 to November 2023 the CAAC report states that the project only has a cost of $173,067 in costs. Did Moss Adams make up expenditures or is the CAAC report wrong? How many other discrepancies like this are there? A full reconciliation with the CAAC report should have been performed to identify issues such as this.

- Moss Adams used Project Commitments, or “Costs approved with executed purchase orders or contracts” to determine the total project cost. There are numerous instances of where the Moss Adams number does not reconcile with numbers reported in the CAAC report. Take as one example the Kendrick Lakes FF&E project that was listed as “100% Complete” in the March 2023 CAAC report with a cost of $612,175. This project is still listed at that same cost in the November 2023 CAAC report. Yet, Moss Adams reported Commitments for that project at $628,563. This would result in the Moss Adams report over-stating project costs and under-stating the remaining available funds. Once again, this discrepancy is not identified unless a full reconciliation to the CAAC report is performed.

- There are numerous instances of where costs listed on the CAAC report exceed project Commitments on the Moss Adams report. This is possibly understandable as project costs may have increased, but these discrepancies contribute to the inaccuracy of the Moss Adams number with relation to the CAAC reported number which, once again, are only resolved through a complete reconciliation.

Finally, the report highlighted some very troubling aspects of the bond and capital programs.

1. The report identified more than $34M in “Other Expenditures” from the Capital Fund and then went on to define “Other Expenditures” as:

OTHER EXPENDITURES

Other program charges not project-specific or not yet allocated to projects and debt service costs (i.e. Project ID P91700P98A and P000000001). These costs include, but are not limited to, the following expenditure categories: vacation, software and IT, interest payment, cell phone and telephone, printing and copying, loan payoff, advertising, mileage, and payroll.

“Vacation”, “payroll”? Other than debt service, these expenditures sound very suspicious and have the indications of being an unaccountable slush fund.

2. Moss Adams identified close to an additional $55M in “Other Expenditures” just in the CIP projects. This money is not used for interest or debt service, so what was all of this money used for? Isn’t that a question that should be answered? That’s an awful lot of money.

3. There is an additional $12M in district projects where contract costs were less than $50k and were not validated by Moss Adams. These small expenditures and contracts are areas ripe for fraud. Has anyone seriously looked at them?

4. There are multiple questionable projects that show up in the Moss Adams report. Projects such as $212k for the Candelas Regional Trail and $115k for the Meyers Pool parking lot. Why is Jeffco spending one cent more than the $17.5M already committed for the Meyers Pool? Who approved these when Jeffco has to go begging for money to replace Fletcher Miller?

The bottom line is that the Moss Adams report provided absolutely zero insight into the key question of how much unallocated money remained in the CIP. It did however prove, once again, that both a full forensic audit and a performance audit, as recommended by Moss Adams in their first report, need to be performed as there are just far too many troubling aspects surrounding the $160M over budget Capital Improvement Program.