Allocation of Bond Premium to Charters

As we saw in Part II, Jeffco’s Board of Education unanimously adopted a Bond Proceed Sharing Resolution that clearly states “the Board of Education will allocate a percentage of the bond proceeds equal to the percentage of full-time district students enrolled in district-authorized charter schools”.

Yet, Jeffco did NOT allocate ANY of the bond premium to District Charters. That was a loss of at least 9.29% of the Bond Premium of $50M or $4,660,360. If the share percentage was calculated correctly with 2019 student count numbers as explained in Part II, that revenue share loss is $4,745,642.

Why didn’t Jeffco schools share the Bond Premium? We weren’t part of the conversations and no discussion took place at the Board table, but we can only surmise that Jeffco is attempting to make a distinction between Bond “proceeds” and Bond “premium”, essentially saying that the bond premium is not part of the bond proceeds in order to keep the $4.7M for District projects.

That is just plain wrong!

While this attempted distinction has worked to silence the meek District Charter schools who are afraid of losing their Charter authorizations, the District knows that the IRS does not make that same distinction.

26 U.S. Code § 148.Arbitrage

Defines Proceeds as:

Proceeds means any sale proceeds, investment proceeds, and transferred proceeds of an issue.

And sale proceeds as:

Sale proceeds

Sale proceeds means any amounts actually or constructively received from the sale of the issue, including amounts used to pay underwriters’ discount or compensation and accrued interest other than pre-issuance accrued interest. Sale proceeds also include, but are not limited to, amounts derived from the sale of a right that is associated with a bond, and that is described in 1.148-4(4). See also 1.148-4(h)(5) treating amounts received upon the termination of certain hedges as sale proceeds.

Jeffco agrees with this definition as in a May Alameda presentation to the BoE, Tim Reed included the Bond Premium in his calculation used to determine arbitrage requirements.

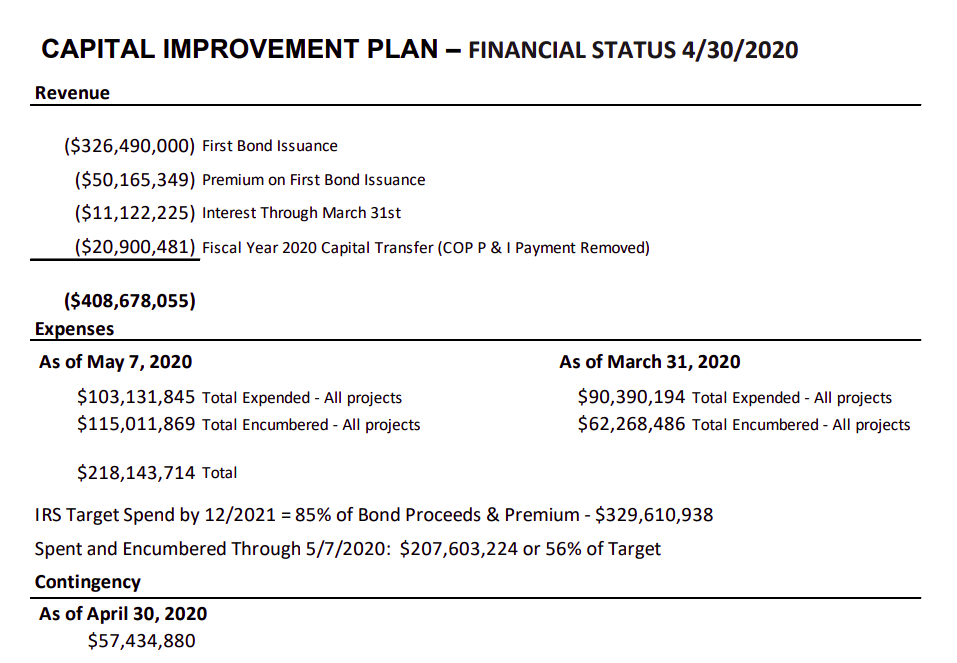

IRS Target Spend by 12/2021= 85% of Bond Proceeds & Premium $329,610,938

It is obvious that Jeffco knows that the IRS considers Bond Premium to be part of Bond proceeds.

Therefore, Jeffco has violated its own Sharing Resolution and defrauded the District Charters of over $4.6M by not sharing all of the Bond Proceeds, in this case the Bond Premium, with them.

In essence, Jeffco got the Charters to support, and campaign for, 5B, but in the end isn’t holding up its end of the bargain.

Shame on Jeffco schools!