Last

week Jeffco citizens heard the Moss Adams presentation relating to

their review of the Capital Improvement Program.

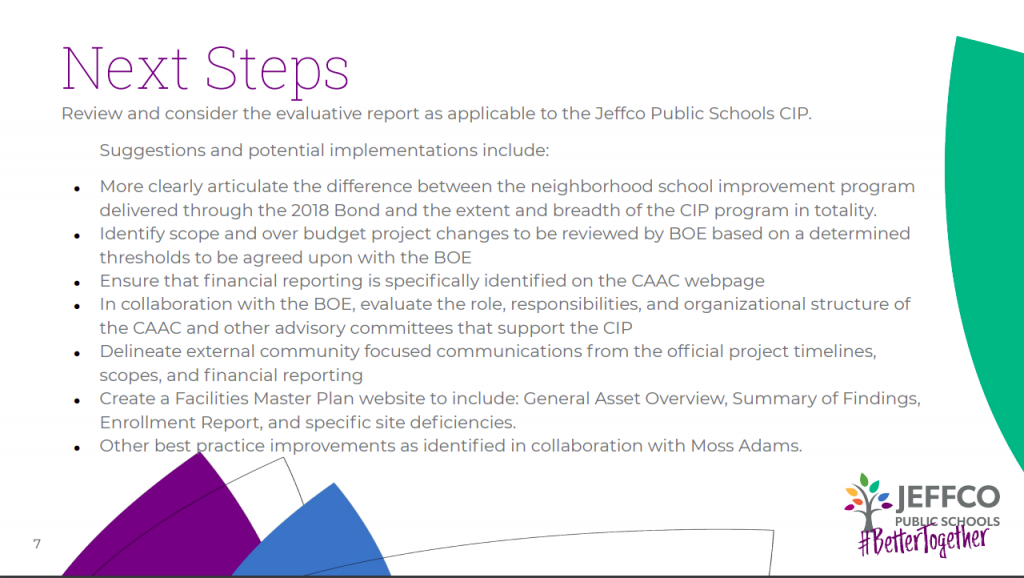

If you looked at Jeffco’s Next Steps slide, you would think that only a few simple communications tweaks were needed.

This

was reinforced by Superintendent Dorland telling the Board that “Most

projects are at or near budget”.

However, if you read the full report, this couldn’t be farther from the truth.

First,

it is completely false that most district projects are at or near

budget.

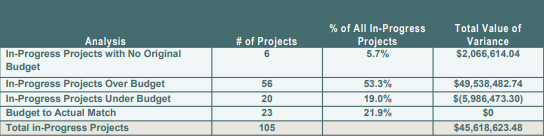

The

Moss Adams report shows that 59% of In-progress projects are over

budget, with 19% of all projects expected to exceed their budget by

over $500,000.

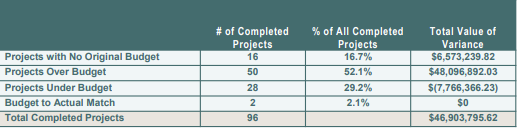

It

is worse for Completed projects where 67.8% are over budget, with

18.8% exceeding their budget by more than $500,000.

Dorland

was wrong. If someone gave her that faulty information they should be

fired. If she said that without doing the proper research, then she

should be reprimanded. She should always give the Board accurate

information.

Regarding the report, the findings and recommendations were much more serious than Jeffco staff wants people to believe.

Here

are the highlights:

The

current program cost estimate is now $136M more that what was

initially shown to voters in 2018.

Bid

tabulations or evaluations for the selection and award of projects

were not available.

The

District does not have policies and procedures specific to the

change order process (i.e., review process, thresholds, approval

process, approval levels, etc.).

These are egregious. Jeffco is talking about nearly 25% cost overruns (above the included 10% project contingency), with Reed telling the Board to expect another $43M in overages before the program is over.

Not

having project selection evaluations means that the program is not

transparent and is ripe for favoritism and or kick backs.

The

same can be said regarding the change order process. This leaves the

program ripe for vendor overcharging or kick backs.

None

of these are good, but all were glossed over in the report review

session.

To

make matters worse, instead of acknowledging and addressing the Moss

Adams findings and recommendations, all Director Rupert did was fault

the consultants, make excuses and praise staff for the program.

It

was appalling.

In addition, Rupert made a point that the program was not based on the 2016 Facilities Master Plan, when former CFO Kathleen Askelson, in her January 2021 bond review report stated that it was.

Rupert

was wrong and Dorland was wrong.

The

report was more damning than anyone wants to admit.

We

can only hope that Dorland can clean the mess up, but her statements

and actions to date don’t give me much hope.

Jeffco is falsely telling taxpayers that school projects are under budget

Jeffco’s Flipbook (and here if Jeffco deletes or changes it) is declaring multiple schools are under their bond program budget when they clearly aren’t.

I will document two of the schools here, Fremont ES and Belmar, but there are many more, including Arvada K-8, Columbine Hills, West Jeff MS, Welchester, Eiber and Semper.

Why

is this happening? There are only two answers, either complete

incompetence on the part of staff or a desire to mislead the public

into believing the management of the program is not as bad as it

really is.

Belmar

–

tagged

with a green arrow in the Flipbook

The Flipbook states that Belmar has a budget of $1,068,000.

This

is nearly $250,000 over budget and does not include additional costs

such as security glass, site lighting, IT cameras and network

upgrades.

Fremont

ES

The Flipbook states that Fremont has a budget of $1,289,000.

The

current CAAC report shows Fremont costs as:

Efficiency

& Future Ready

$1,087,700

FF&E

Costs

$334,083

Hazmat

Costs

$102,186

Total

$1,523,969

or

more than $230,000 over budget, not including additional costs such

as security glass, site lighting, IT cameras and network upgrades.

Jeffco

is lying to the public to present a picture that they are good

managers and stewards of our money, when the exact opposite is true.

This is not a good look.

Jeffco should fix this immediately. In addition, Jeffco should show the total costs for each school project so that voters and taxpayers can see the truth.

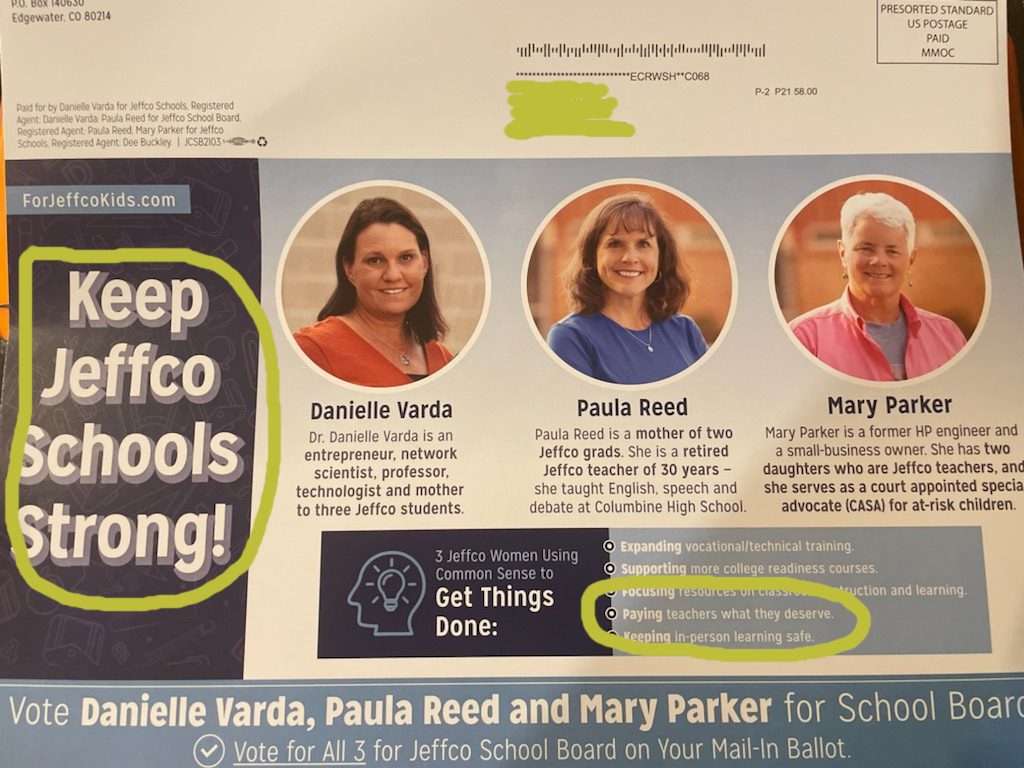

Varda, Reed and Parker are running on a platform of “Paying Teachers What They Deserve”.

Obviously, they want people to believe that teachers are underpaid for what they are doing. But, what does that really mean in an era of declining results in Jeffco Schools?

In any private company I’ve ever been at a salary increase would be looked at very closely when organization objectives weren’t met. In many instances, annual increases would be limited to COLA increases or less, and it would stay that way until objectives were met.

For instance, taking last year’s DUIP, how can anyone justify salary increases when Jeffco wasn’t even close to achieving their goals, that were set during the pandemic?

Yet, Varda, Parker and Reed think that teachers “deserve’ more pay. Their definition of “deserve” is far different than mine. A salary increase above COLA would be hard to justify in my mind.

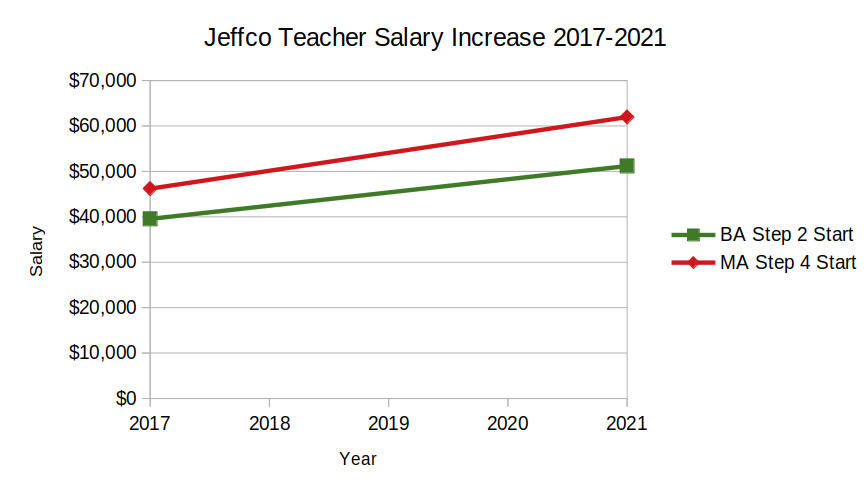

In fact, over the past 4 years teachers’ salaries have increased significantly, far outpacing the 11% Denver inflation rate.

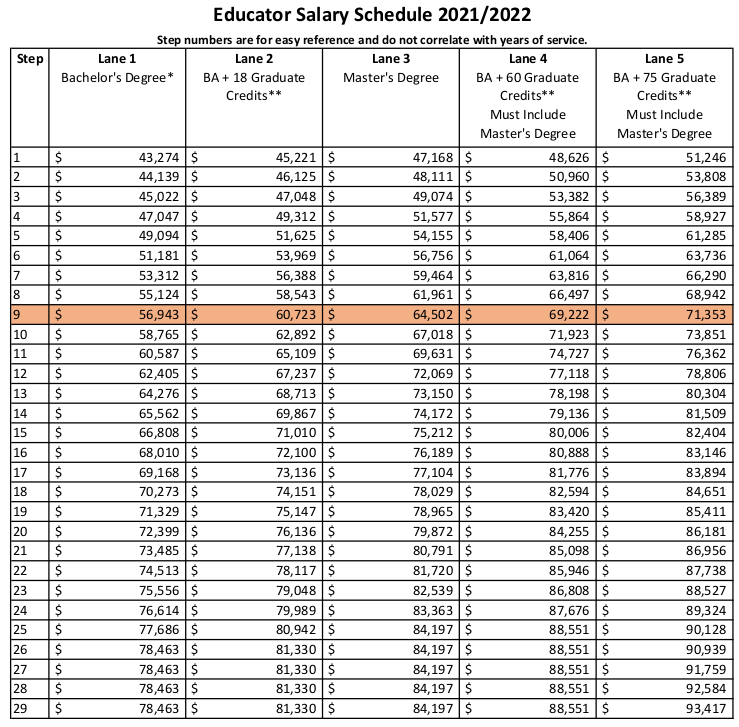

For example, a teacher w/BA @ Step 2 and a teacher w/MA @ Step 4 would have each seen salary increases of approx. 30% including the 4 steps awarded by Jeffco. These teachers now make $51k and $61k respectively, before benefits.

Approximately

40% of Jeffco teachers have salaries over $70k and 20% make over

$80k.

That’s

not bad for:

185 working days

Job Security

Ability to retire w/75% salary @55 & 30 years

In

addition, Jeffco currently pays teachers based on their level of

education along with years of service. Yet, study after study show

that, with only limited exceptions (e.g. math and science), advanced

degrees do not correlate to increased teacher effectiveness.

(https://www.mhec.org/sites/default/files/resources/teacherprep1_20170301_2.pdf)

Therefore, why is Jeffco paying more to teachers with those degrees?

Do those teachers really “deserve” higher salaries? Not in my

mind.

With

year

after year of

declining education results, just how

much do Varda, Parker and Reed think these teachers deserve in

salary? They’re

not saying, but you can be darn sure a salary increase wouldn’t be

the topic of discussion on any corporate Board.

Jeffco schools is not an organization that is showing that it “deserves” salary increases for teachers and admin. It’s time to take a realistic look at total teacher compensation, not just salaries. It’s time to push back on the same old union rhetoric that teachers are underpaid because they aren’t for the results they are delivering.

And

it is absolutely wrong for teacher pay to be one of Varda, Reed and

Parker’s top priorities when Jeffco’s education results are so

atrocious.

They

aren’t a good fit for what Jeffco’s kids need now.

Jeffco Schools Capital Asset Advisory Cmte can’t be trusted to make good financial decisions and gets played as fools by Tim Reed and Steve Bell. They are utter failures at being good stewards of Jeffco’s taxpayers’ money.

They

are responsible for overseeing now $110M in cost estimate overages of

the Capital Improvement Program and recently

agreed to spend an additional $17M for a new gold-plated

swimming

pool for the community of Arvada.

The

$17M and decision process for a new Arvada community pool is

egregious. Here’s why:

1.

Jeffco swim teams will use the pool approximately 10% of the time,

Arvada

residents the rest. Yet

Jeffco will

pay

for 50% of the $33M-$35M construction costs. That

doesn’t seem equitable. Not one CAAC member questioned that

arrangement or

suggested that Jeffco’s share be reduced to something reasonable

like

$7M.

2.

Reed told the CAAC that construction costs for a Jeffco owned 50

meter pool would be $15M-$20M. Not

one CAAC

member asked

if Arvada was taking advantage of Jeffco by building a gold plated

facility that would

cost $15M more than Reed’s estimate.

3. No one asked what was even included in that additional $15M.

4. Other area rec center pools in Wheat Ridge and Evergreen are 25yd pools. No one asked why the Arvada facility had to be a 50 meter pool. No one asked what a 25 yard facility would cost.

5.

No one asked what the cost would be to add 25

yard pools

at High Schools.

Smaller

pools, locker rooms already in place and possibly shared walls would

result in lower costs.

6. Not one CAAC member asked what the implications and precedent would be set for the other 4 Rec Districts in Jeffco when their pools “age out”. Would Jeffco help those Rec Districts fund their new pools in the future? Or, would Arvada residents be “winners”? In 2018 Evergreen voters rejected a bond package that included pool upgrades to their 50 year old failing facility.

7.

No

one asked about the equity. No

one asked why Reed and Bell thought it was fair for Lakewood or

Evergreen residents to pay for an Arvada community pool.

7. Not one CAAC member asked what Jeffco schools facility needs would not get accomplished because $17M went into Arvada’s new pool. Taxpayers were told that Jeffco had $1.3B in facilities needs when they were asked to approve the $567M bond. Are those not real needs now? Shouldn’t there be a prioritized list of projects awaiting funding that this project is compared against? Replacement schools for example? Isn’t prioritization a key function of the CAAC? Yet, trade-offs weren’t even discussed.

8.

Not

one CAAC member asked about the certainty of Arvada voters passing a

bond to fund the facility. A recent bond to fund upgrades in

Evergreen Rec district, including pool upgrades failed.

9. Not one CAAC member questioned Reed when he said that the pool would be funded from Capital Transfer, like Cap Xfer is some unlimited source of funds. Jeffco Schools promised voters that Capital Xfer would be committed to the CIP for 6 years. There is no additonal money. In fact, Jeffco is already shortchanging the CIP by $12M

10. Not one CAAC member asked how funding Arvada’s pool would affect voter sentiment District wide when Jeffco needs another capital bond passed in a few years. The current bond was carefully crafted so that everyone got something and still just barely passed. If Jeffco schools pays for Arvada’s gold plated facility, you can be guaranteed it will not sit well with Lakewood, Wheat Ridge and Evergreen voters in the future.

In a 6-0 (one absent) vote, the CAAC recommended to endorse the project.

The committee’s failure to ask reasonable questions relating to spending $17M on a pool facility for a specific community is indicative of the overall lax oversight and general negligence in the CAAC’s role as stewards of Jeffco taxpayers’ money.

Jeffco’s CAAC can’t be trusted to make good financial decisions.

Jeffco taxpayers deserve better!

Jeffco's Capital Improvement Program is currently $110M over initial cost estimates

Recently, Colorado Community Media, including Jeffco Transcript and Arvada Free Press printed an article by writer Bob Wooley about Jeffco’s Capital Improvement Program.

For

the most part, Wooley did a good job of attempting to explain a

financially complex program. However, there were some comments and

statements made by Jefferson Public Schools’ officials that were

misleading or downright false.

I’ve

outlined several of those areas below:

1.

The article states:

After

the Bond passed, the project’s estimated costs were increased by

nearly $32 million for a revised total of just under $737 million for

the program.

TRUE

– $32M

in hidden

costs were added to the program

After

the bond passed, $32M in costs were added to the flipbook for

the same list of projects.

The

use of $32M in contingency to

cover these costs was

essentially hidden.

2.

The article states:

District

officials say the increase was a result of changes in scope, market

conditions, incorrect estimates or various other factors like

asbestos removal, which were determined once the District was able to

perform more in-depth evaluations of each individual project.

While I agree that factors such

as scope changes, market conditions and incorrect estimates can

result in changed estimates, that doesn’t fully explain the extent

of the cost estimate changes between the first and second flipbooks.

The project costs for 81 schools, or nearly 60% of the total,

increased by EXACTLY 5%. This is not indicative of changes in

scope or incorrect estimates. That’s indicative of using Excel to

pad costs.

3.

The article states:

“We

told voters we would accumulate six

years of approximately $20 million

at the back-end to fill up the program,” Reed says.

FALSE

– Voters were told $23M

Voters

were told that exactly

$23M

annually in Capital Transfer would be accumulated. In reality only

$20.9M

annually is currently being transferred. That means

there is a

$12.6M shortfall in

stated revenue, again made up with Contingency.

4.

The article states:

“and

over $3.5 million was spent on hazmat expenses (which technically, do

not count as overages).”

FALSE

– Hazmat

costs ARE overages

Why

aren’t $3.5M in hazmat expenses considered overages? Any

decent construction project manager with 50 year old buildings

knows there is asbestos in those

buildings that will have to be mitigated. Mitigation costs should

have been factored into the original estimates.

Where

is the money coming from to pay for the hazmat expenses? It’s

coming from the District’s program contingency. Therefore,

technically, and for all intents and purposes, hazmat expenses are

program costs that reduce available contingency This is merely an

attempt by Reed to put lipstick on a pig to make $3.5M in overages

not seem like the $3.5M in overages hazmat costs really are.

5.

The

article states:

In

a document Reed says is now posted to the Capital Asset Advisory

Committee (CAAC) website, all budget variances are listed with

specific overage amounts and the reason for the cost variance.

FALSE

– This

document

lists variances against revised cost estimates, not original

estimates

This

document hides $32M in cost increases. That’s deception.

6.

The article states:

Therefore,

the precise amount of contingency that’s been spent on actual

projects thus far is $65,815,424.

FALSE

– The amount of contingency allocated is currently over $110M

$65M

from what Reed wants people to believe is the contingency spent, plus

$3.5M in hazmat, plus $32M in increased estimates plus $9M from

recent fields project = $110M in contingency allocated.

7.

The article states:

“I’m

not a construction guy,” Bell said. “But we have a construction

guy and I was speaking to him this morning and he said “you know, a

year ago the cost of steel was $53 a ton — today it’s $79.” A

year ago did anybody know it was going to go from $53 to $79? No.”

MISLEADING

– Cost of steel is only one small component of cost increases

Both Tim and Steve have told the Board on several occasions that they have been getting good pricing due to the pandemic. And, this report shows that non-residential construction costs have been relatively flat in Denver for the last 2 years, increasing by only 2.1% total over that time. In addition, there are numerous projects that had no steel involved that are significantly over budget. This is a misleading and deceptive statement.

8.

The

article states:

“According

to Tim Reed, Jeffco’s Executive Director Facilities &

Construction, the amount of contingency that had been spent as of

Feb. 22, was just over $81 million, of which nearly $12 million went

to charter schools…”

MISLEADING

to FALSE – $12M to Charters came from Bond Premium

The

agreement with District Charters was that Jeffco would share

approximately 10% of all bond proceeds with Charter schools. The $12M

Tim Reed is referring to is based on Charters’ share of accrued

interest and bond premium. This has nothing to do with District

contingency.

The

bottom line is that the Capital Improvement Program has already

spent

or allocated $24M over its original $86M contingency budget ($110M

total) only

2.5 years into the program. In addition, Jeffco has hidden

a $12M revenue shortfall from

Capital Transfer.

The

amount

of deception and lack of accountability for large cost increases is

truly unbelievable.

Below are the

observations I made to the Capital Asset Advisory Committee on

November 4, 2020, Tim Reed’s Response, my rejoinder and a current

update..

Letter to CAAC –

24 November 2020

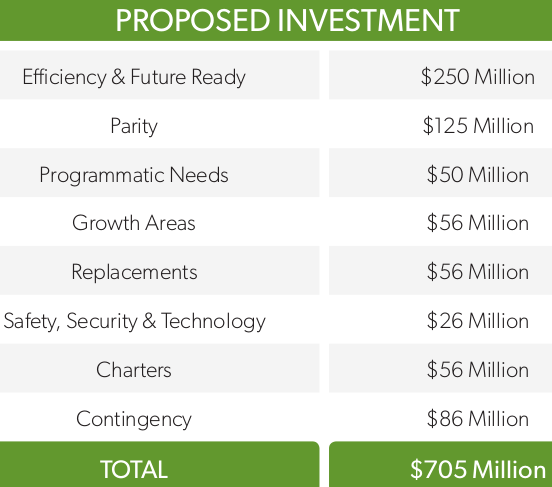

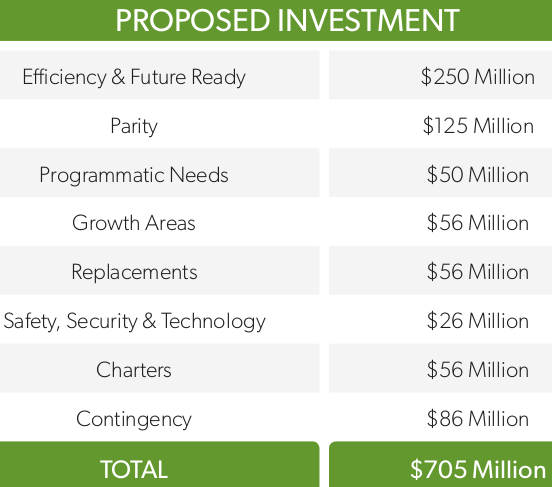

$57M

over budget. On its own, a program that is $57M over

budget less than 2 years into a 6 year plan should automatically

trigger a Performance Audit. Just to recap, voters were told the

Capital Improvement Program would cost $705M. At the CAAC’s last

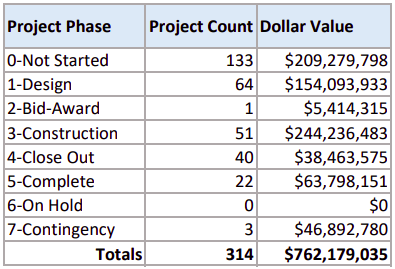

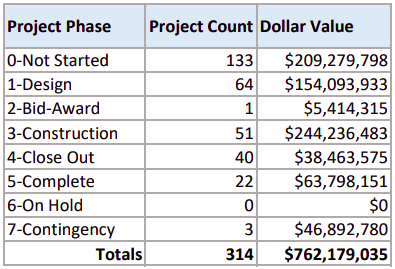

meeting in November, it had a $762,179,035 price tag.

Tim Reed’s

Response – 10 December 2020

Response: The $705M that is cited does not take into consideration premium or accrued interest that in accordance with the bond language and IRS Arbitrage regulations are to be applied to capital projects. At the time of publication the district had no knowledge of what premium or interest earnings there would be. When the amount of those funds were identified the project costs were increased to compensate for future inflation. The budget has been adjusted to reflect the revenue ($762,179,035) available as of October 31, 2020. The remaining bonds are about to be issued and could have a premium associated with them as well as interest on those bond proceeds that will accrue over the next three years resulting in an increase in Program revenue.

Rejoinder to Reed

– 4 January 2021

The Capital

Improvement Program is $57M over budget, no matter how Tim tries to

spin it. Taxpayers gave Jeffco $649M to complete $563M worth of

projects. That was the approved budget. Neither taxpayers, nor the

Board, gave Tim Reed anything additional to complete the $563M worth

of projects. Yes, the Bond market gave Jeffco schools an additional

$50M, but there was NEVER any implicit or explicit approval,

anywhere, to use that additional money on the same projects that

taxpayers already approved a budget for. Let me be blunt. I’m angry

that when $86M in contingency was already allocated to a program and

with District stated maintenance needs of $1.3B, that $50M in “bonus”

money gets shadily added to contingency and essentially squandered

when it could have been been used for other needs. Let me ask you as

CAAC members a question. Did you or the Board explicitly approve the

use of Bond premium for added contingency to the Capital Improvement

Program or did Tim Reed merely add it to the “pot”? Was there a

discussion on what else could be prioritized and done with that

money? Do you not understand the implications of Tim’s actions when

it comes time to ask taxpayers for another Bond? Tim can’t tell me

in the answer to my Question 9 that Jeffco couldn’t use the $50M in

Bond Premium for 2 replacement schools because taxpayers didn’t

approve it and then turn around and tell me here that taxpayers

approved $50M in added contingency for the CIP. That logic doesn’t

hold. The program is $57M over budget, plain and simple and Tim Reed

squandered the $50M bond premium.

Current Status –

6 March 2021

Anyway you look at it Jeffco’s Capital Improvement Program is over budget. Taxpayers were told that District projects (excluding Charters) were going to cost $563M with an additional $86M in program contingency. That’s a total of $649M. As of the February 21 CAAC meeting, the total estimated cost of all District projects is $662M (Total less Contingency and $65M for Charters). That’s $13M over the total original budget. Add in the additional $8M+ in contingency the Board just approved for fields and the total budget is now $21M over assuming ZERO remaining contingency. That overage is only going to get worse.

This is not what taxpayers were promised. Taxpayers were promised an on-budget program. $86M in contingency usage to date plus an additional $21M is way over reasonable expectations and over budget in anyone’s definition of over budget.

Where is the promised annual independent audit of Jeffco's Capital Improvement Program?

To assure voters

that the $705M 2018 bond program would be well managed, Jeffco wrote

into the ballot language that the program would be subject to an

“annual independent audit”. The implication being that the

program would be scrutinized on a yearly basis by a firm without

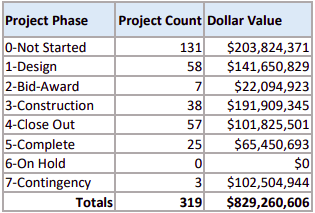

financial ties to the District. Yet, two and a half years into what

is now an $832M program only a very basic financial audit has been

conducted, by the same firm that has deep and long standing ties to

the District.

The ballot language

implied that voters would get more than that. Now, with multiple

questionable practices and current cost estimates $110M over what

were presented to voters, Jeffco’s staff, Board and CAAC have all

balked at providing the transparency and accountability that we all

thought we would get when we entrusted Jeffco with our money. It is

just incomprehensible to me that there is so much resistance to

providing the transparency that was promised. It seems that if there

was nothing to hide a Performance Audit would give the program a

clean bill of health and end, once and for all, all questions. By

continuing to refuse to conduct a Performance Audit it only

perpetuates the assumption that there really is something to hide.

That is not a good look!

In addition, the

highly touted Citizens’ Capital Asset Advisory Committee is not

doing its job either. CAAC meeting notes reveal that only until

recently they have remained silent and allowed the program to go

tens of millions of dollars over budget without asking any questions

whatsoever. They have provided poor oversight of our money.

After initially observing a high usage rate of program contingency funds and subsequently numerous other instances of extremely questionable observations regarding the transparency, management and fiscal practices of the program I sent an email

to members of the CAAC on November 24, 2020 highlighting 10 very specific instances which raised questions with the management and transparency of the program and urging them to call for a Performance Audit conducted by a truly independent firm. Tim Reed replied on December 10, 2020 and I sent a rebuttal to Tim’s response to members of the CAAC on January 4, 2021.

On each of my letters I clearly include an offer to discuss my concerns and my telephone number. The fact that no one has taken me up on my offer speaks loudly in and of itself.

Finally, on January 4, 2021 I sent a copy of my original letter to the CAAC, Tim Reed’s response and my rebuttal to the Board of Education

The Board of Ed Secretary’s reply was far from confidence building:

Dear Mr. Greenawalt,

Members

of the Board of Education received your January 4, 2021 email

correspondence regarding our Capital Improvement Program. Thank you

for bringing your concerns forward. You are correct that the Board of

Education will be receiving feedback from the Capital Asset Advisory

Committee and your concerns are noted.

Sincerely,

Stephanie

Schooley

Secretary,

Jeffco Public Schools

with no further

communication from the Board.

Over a series of

posts I will outline some of the issues I have seen with regard to

the transparency and fiscal management of the 5B bond program and

take a look at some of the unbelievable and incredulous responses Tim

Reed provided in a weak attempt to address my concerns. Here are some

of the topics that I will cover:

Over budget

($57M as of November 2020)

Projected

$32M Contingency Shortfall

Deceptively

adding $31M to Flipbook costs

Failure to

Share Bond Premium with Charter Schools

Out of Scope

Projects

Deceptively

Hiding the True Cost of Alameda HS Cost Overruns

Recent Large

Underspend on FF&E Projects

Unexplained

Recent Increase to Capital Transfer Revenue

Questionable

Use of $50M in Bond Premium Contingency

Failure of

CAAC Members to Maintain Independence

Failure of

Jeffco to Provide $23M in Capital Transfer as Promised to Taxpayers

Jeffco needs to put

these concerns and questions to rest.

Jeffco needs to

conduct the independent Performance Audit that voters thought they

were going to get.

1. $57M over budget. On its own, a program that is $57M over budget less than 2 years into a 6 year plan should automatically trigger a Performance Audit. Just to recap, voters were told the Capital Improvement Program would cost $705M. At the CAAC’s last meeting in November, it had a $762,179,035 price tag.

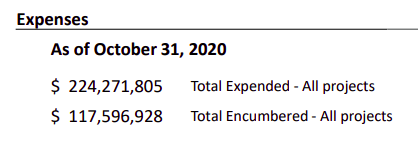

2. Projected $32M Contingency Shortfall. At the October 7th Board Study Session, Tim Reed told the Board that $68M in contingency had been used to date.

At the CAAC’s November meeting Tim presented the following numbers for funds Expended and Encumbered, totaling $341M.

Subtracting the $68M of contingency from this value means that $273M of the $595M in total program costs are currently Expended or Encumbered, leaving $322M in remaining projects. If that same rate of contingency usage continues, that would require remaining contingency of over $79M. Yet, there is only $47M in contingency remaining, a $32M shortfall.

Do the math. The numbers don’t lie. This is not a healthy Program.

3. Deceptively adding $31M to Flipbook costs. District project costs were presented to voters as $563M. You can arrive at that number by subtracting the Charters $56M and the Contingency $86M from the Flipbook presentation.

This can be verified by adding the costs of individual projects in

the original Flipbook (Plus approx. $17M in costs for Trailblazer,

North Transportation Hub, OELS and Preschools projects which were

withheld from voters).

However, sometime after the Bond passed, the District changed the

Flipbook. The cost of nearly every project increased. Here are some

examples:

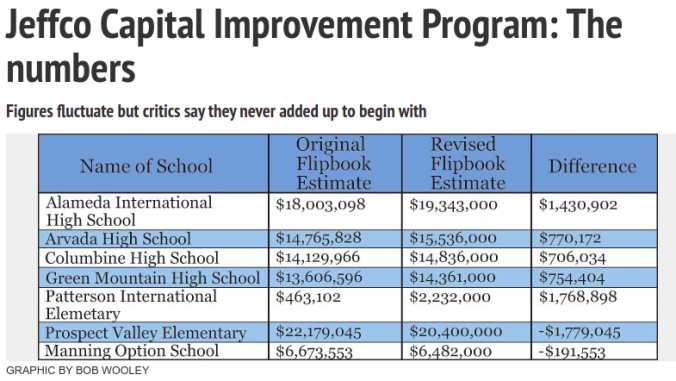

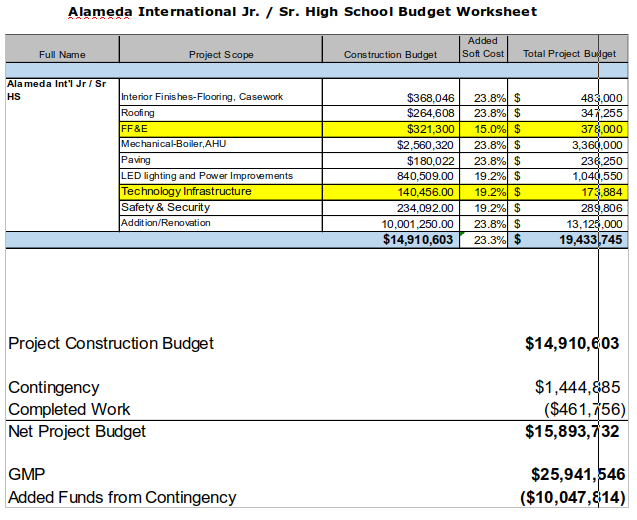

Alameda HS – an increase of $1,430,902 to $19,434,000

Green Mountain HS – an increase of $754,078 to $14,361,000

Jefferson Jr/Sr HS – an increase of $672,810 to $14,129,000

This had the net effect of raising BASE costs by a total of

$31,967,419. Essentially hiding $31M of cost increases.

For example, when the construction budget for Alameda was presented to the Board, contingency usage of $10,047,814 was based on the updated Base cost of $19,433,745, instead of the original cost estimate of $18,033,098. This usage of the revised cost estimate deceptively hid the totality of the increase, and the additional use of Contingency, of $1,430,902.

Therefore, cost estimates for all projects have now increased by

$100M; the $68M in Contingency that Tim Reed freely told the Board

PLUS the $31M in hidden cost estimate increases.

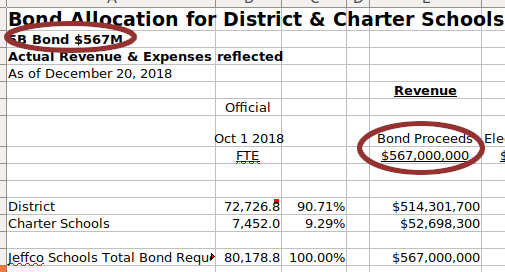

4. Failure to Share Bond Premium with Charter Schools. As recently as of the end of October, the District still had not shared Bond Premium with Charter schools, in violation of the Board’s October 2018 Sharing Resolution. The District spreadsheet widely circulated to Charter Schools show that the District only calculated sharing revenue based on the Bond par of $567M.

Yet, at the November 11th Board Study Session, Steve Bell told the Board that Bond Premium is shared with Charters.

Therefore, at this point, Charters are owed approximately $4.6M, PLUS interest – which will subsequently reduce the Contingency available for District projects by a corresponding amount.

Brian Ballard, Chair of the District’s Financial Oversight

Committee, has said that it is the CAAC that has responsibility for

overseeing 5B Bond funds. If that is the case, why hasn’t the CAAC

ensured that District Charters have been given their complete share

of the funds?

5. Out of Scope Projects. There are multiple projects that can be identified that were not in the scope presented to voters. Several easily identifiable, high-cost projects include: Ralston Valley HS Roof, Lakewood HS Track, West Jefferson MS Track, etc. The following images were taken from the Original Flipbook presented to voters and clearly do not show these projects.

Was there any discussion relating to the addition of scope and

reduction of contingency for these and other added scope projects?

What was involved with this process? Were these prioritized over

replacement schools? Was there a vote?

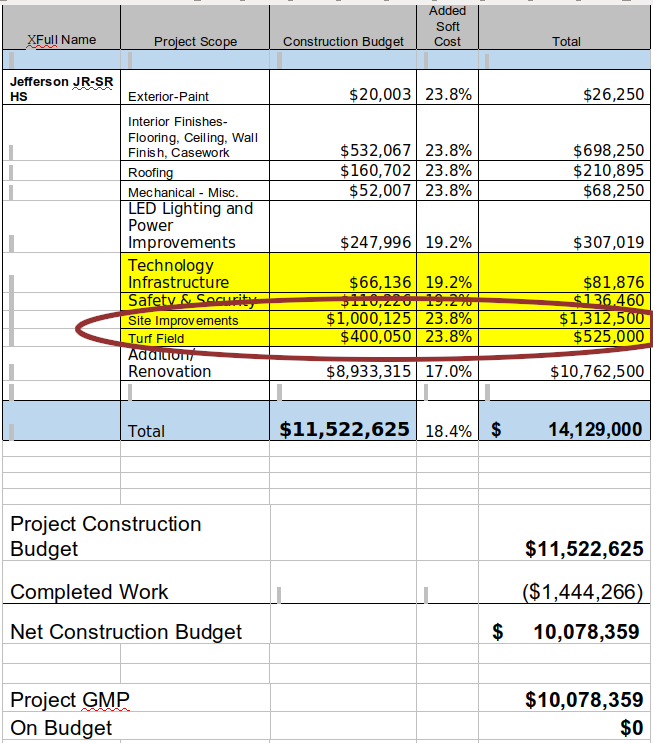

6. Deceptively Hiding the True Cost of Alameda HS Cost Overruns. Similar to Jefferson Jr/Sr HS, Alameda HS is slated for Track and Field Upgrades. When the Jefferson project was submitted to the Board for approval, the Track and Field upgrades were included in the project costs and subtracted from the remaining budget.

This was not the case when Alameda was presented to the Board. The cost for the Track and Field upgrades were left off of the presented costs, effectively deceiving the Board that total overages are at least $1.5M over what was shown. Was that intentional deception, or merely incompetence?

7. Recent Large Underspend on FF&E Projects. We all like to get good deals. However, the cost savings on several recent FF&E projects go beyond the definition of good deals, suspiciously into the realm of scope reductions. Look at some of the “savings” generated from some of these FF&E projects that were recently presented to the Board, $150k, $300k, $315k and $310k.

These “savings” are 47%, 22%, 60% and 66% less than the original

cost estimates. That’s far more than a reasonable person would

expect from a “good” deal. What happened here? Was scope cut at

these schools?

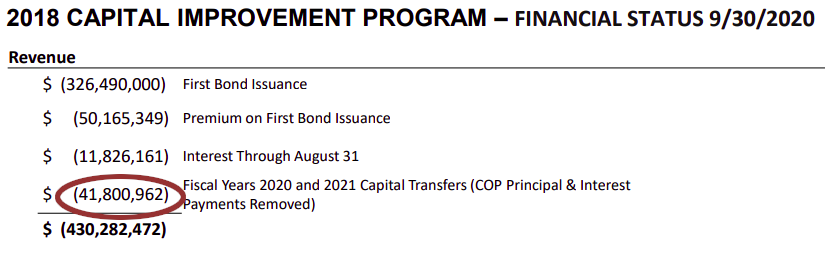

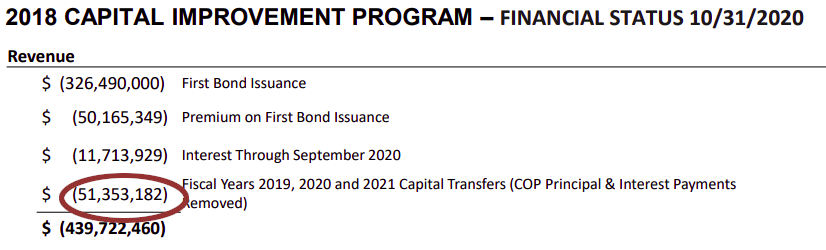

8. Unexplained Recent Increase to Capital Transfer Revenue. At the October CAAC meeting, members were shown Capital Transfers into the Capital Improvement Program of $41.8M. Yet, in November, they were shown $51.3M. Where did that additional $9.5M come from?

(On a side note, how does Interest Revenue DECREASE by $110,000 from August to September? Can you trust any numbers that are presented?)

Approximately $3M appears to come from the movement of the contingency in prior capital improvement programs such as 18M and 19M. This contingency decrease can be seen in documents presented to the CAAC.

But, the source of the remaining $6.5M is unexplained as the value of

the 18M, 19M, 20M programs remain the same. And this happened mere

days after Steve Bell told the Board that the capital transfers would

be $20M/year over 6 years for a $120M total.

9. Questionable Use of $50M in Bond Premium for Contingency. Recently, Tim Reed and Steve Bell told the Board that during initial 5B discussions the bond ask amount was decreased and 2 replacement schools were removed from the list of projects.

If this was the case, why then, when the District received $50M in bond premium, weren’t replacement schools immediately added to the list of projects? Instead, it appears that the $50M in bond premium has merely been added to the $86M already allocated to program contingency. What was the process in determining that the additional $50M in contingency should be used for contingency instead of being used for replacement schools, particularly when taxpayers voters were told that Jeffco had $1.3B in deferred maintenance needs?

10. Failure

of CAAC Members to Maintain Independence. Tim Reed

recently sent members of the CAAC a document relating to the Purpose

and Membership of the committee. This document clearly states that

members must be:

Independent and free from any relationship that would interfere

with independent judgment

Gordon Callahan, a CAAC member, has a relationship with the District.

His firm has been the recipient of nearly $1M in contracts over the

past year and a half.

This is not the appearance of independent judgment.

For taxpayers to fully trust the Capital Asset Advisory Committee ALL members of the committee must be completely independent and free of District relationships. Unfortunately, that is not currently the case. His continued membership on the committee is ethically questionable and erodes taxpayer trust.

Jeffco schools failed to share all 5B bond proceeds with District Charter schools

As we saw in Part II, Jeffco’s Board of Education unanimously adopted a Bond Proceed Sharing Resolution that clearly states “the Board of Education will allocate a percentage of the bond proceeds equal to the percentage of full-time district students enrolled in district-authorized charter schools”.

Yet, Jeffco did NOT allocate ANY of the bond premium to District Charters. That was a loss of at least 9.29% of the Bond Premium of $50M or $4,660,360. If the share percentage was calculated correctly with 2019 student count numbers as explained in Part II, that revenue share loss is $4,745,642.

Why didn’t Jeffco schools share the Bond Premium? We weren’t part of the conversations and no discussion took place at the Board table, but we can only surmise that Jeffco is attempting to make a distinction between Bond “proceeds” and Bond “premium”, essentially saying that the bond premium is not part of the bond proceeds in order to keep the $4.7M for District projects.

That is just plain wrong!

While this attempted distinction has worked to silence the meek District Charter schools who are afraid of losing their Charter authorizations, the District knows that the IRS does not make that same distinction.

Sale proceeds means any amounts actually or constructively received from the sale of the issue, including amounts used to pay underwriters’ discount or compensation and accrued interest other than pre-issuance accrued interest. Sale proceeds also include, but are not limited to, amounts derived from the sale of a right that is associated with a bond, and that is described in 1.148-4(4). See also 1.148-4(h)(5) treating amounts received upon the termination of certain hedges as sale proceeds.

Jeffco agrees with this definition as in a May Alameda presentation to the BoE, Tim Reed included the Bond Premium in his calculation used to determine arbitrage requirements.

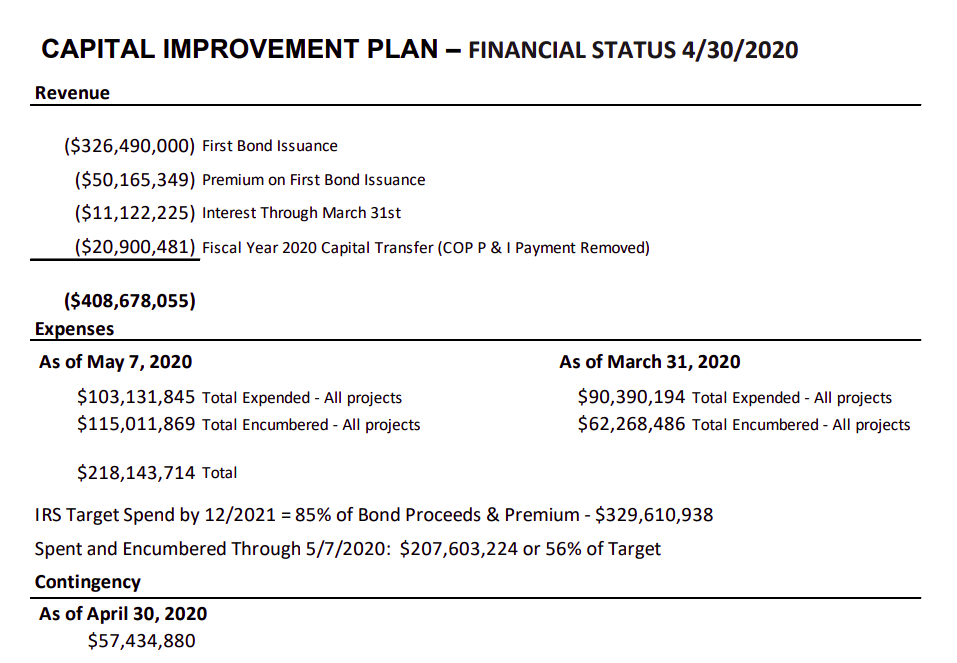

IRS Target Spend by 12/2021= 85% of Bond Proceeds & Premium $329,610,938

It is obvious that Jeffco knows that the IRS considers Bond Premium to be part of Bond proceeds.

Therefore, Jeffco has violated its own Sharing Resolution and defrauded the District Charters of over $4.6M by not sharing all of the Bond Proceeds, in this case the Bond Premium, with them.

In essence, Jeffco got the Charters to support, and campaign for, 5B, but in the end isn’t holding up its end of the bargain.

The positive impact

of high-quality curriculum in K-12 education is undisputed.

Nowhere is this more

evident than in Reading Curriculum.

Phonics has long

been known to be a key ingredient in teaching reading since the

National Reading Panel released its report in April 2000.

In September 2018 Emily Hanford published “Hard Words” her article on the Science of Reading, igniting a national conversation relating to how schools teach reading.

In August 2019 Emily Hanford followed up with “At a Loss for Words” – what’s wrong with how schools teach reading and the national conversation relating to the teaching for reading continued.

Recently, Colorado’s SB 19-199 strengthened the READ Act and the CDE identified quality reading instructional programs that were to be used in state schools.

The discussion surrounding the Science of Reading, curriculum and products that support the Science of Reading is not new.

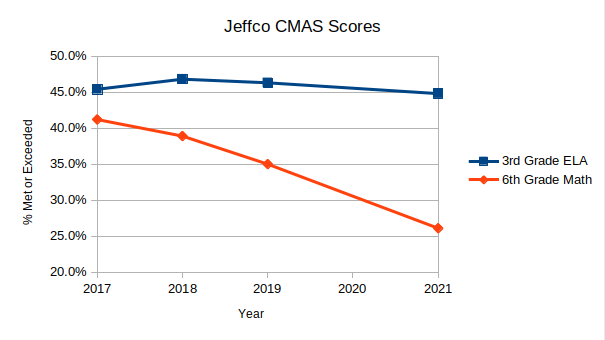

The question then is

why, with only 44% of 3rd graders meeting state reading

expectations, aren’t Jeffco Schools using Science based, proven,

high-quality reading curriculum?

Jeffco’s Chief Academic Officer, Matt Flores, who has been with Jeffco a long time , should know the answer.

His salary cost to the District is $147,000, plus benefits per year.

I would expect

someone, who makes that kind of money to be relatively competent at

their job and provide real value.

Unfortunately, that’s not the case. Flores has overseen the continuing decline in reading proficiency in the District.

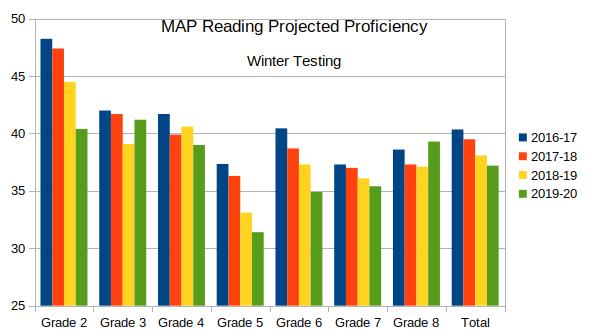

Jeffco’s MAP Predictive Reading Winter scores

He has not overseen a migration to a proven, scientific based reading curriculum at the continuing permanent harm to 1,000s of students each year and has no plan to do so.

Jeffco’s reading proficiency is atrocious. Colorado is essentially mandating the use of approved curriculum and it is a virtual known that high-quality curriculum is a key ingredient in education, yet Matt Flores, Jeffco’s CAO, doesn’t know what curriculum is being used in the District.

That is not the

answer you want to hear from a CAO. In fact, in my opinion, that is

grounds for immediate termination for incompetence and malpractice.

On top of this,

Flores blatantly avoided answering the reporter’s question on when

the District would transition to state approved curriculum.

I would think that

anyone who is even half-way competent would have already planned this

transition/migration and could have easily and instantaneously told

the reporter the answer. Isn’t it reasonable to expect highly paid

executives, responsible for the education of 84,000 kids, to keep up

with the Science and conversations in their profession? Absolutely!

Instead, Jeffco’s students are left with at least another year of being taught with discredited and debunked curriculum harming 1,000s of kids and no one, particularly highly paid and ineffective Matt Flores, will be fired.