Below is a note I sent to members of Jeffco CAAC relating to their supposed upcoming review of the November 2021 Moss Adams recommendations.

Dear members of the CAAC,

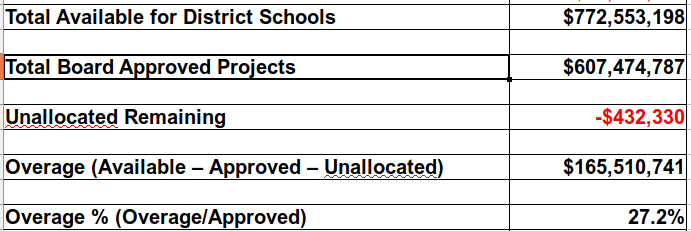

CAAC Notes and Agenda show that you may finally be getting around to performing a review of the now 3 year old Moss Adams recommendations. Reasonable people would have expected this review to have been done in early 2022 based on Superintendent Dorland’s November 2021 promise of a 30-60-90 plan to address the issues. However, I guess 3 years later is the best we can expect from a group of people who let the bond program proceed with more than $160M in overages with nary a peep.

Why review this 3 year old report now though? My guess is that District staff want you to fully participate in the cover-up of the overages, incompetence and mismanagement that ran rampant during the course of the bond program so that they can use you as cover to the community.

Moss Adams provided Jeffco with 14 Observations and 18 Recommendations. In critically looking at just the first 8 Observations below, it is hard to find any recommendations that were implemented completely and with fidelity. All of this begs the question of why Jeffco didn’t immediately address the recommendations? Will you ask that question? Jeffco certainly does a lot of talking about continuous improvement, but when they just blatantly ignore sound and best practice recommendations, you have to wonder why they did that.

It will be interesting to see whether you, with your report and questions, will be part of the problem, or part of the solution. Unfortunately, up to this point, you have been part of the problem in allowing the program to continue with its cost overruns, deception and mismanagement.

Anyway, below is a brief synopsis of the first 8 Moss Adams Observations. I doubt that you will read through them, but just in case you have a revelation and decide to do the job voters thought you would do, you might find these interesting, and probably far different than what the district is going to present to you.

Observation 1 – Bond Expenditure Management and Controls: Bond proceeds were used only for listed purposes as identified in 5B.

Recommendation – The District should continue doing what it is doing. Bond proceeds are being used appropriately.

Area of Concern – Unfortunately, Jeffco used bond proceeds for purposes that were not identified. Are you aware that a Bond Communication Specialist was hired at a cumulative cost of around $500,000? That would not be an appropriate use of bond funds in the eyes of many taxpayers.

Observation 2 – Non-Capital Bond Expenditures: The District allocated administrative costs to the Bond program. However, there are no formalized policies and procedures that define what positions constitute senior District administration.

Recommendation – Jeffco should consult bond counsel to determine what labor allocation components are allowable per the bond language.

Area of Concern – Jeffco attempted to deceive taxpayers. Taxpayers were told that the bond would not be used for salaries of senior Jeffco staff. However, bond proceeds were used to cover some, if not all, of Tim Reed’s salary. Tim is one of just a few Executive Directors in the district. Many people would consider an Executive Director to be part of the district’s senior leadership. Jeffco did not fulfill its promise to taxpayers and some after the fact policy can’t make up for that.

Observation 3 – Independent Bond Program Audit: The District has not required the completion of an annual independent financial audit which contradicts the requirements set forth in the bond program.

Recommendation A – The district should commission and complete an annual independent financial audit.

Recommendation B – The district should consider completing an independent performance audit of the bond program.

Area of Concern – Plain and simple. Jeffco did not fulfill these recommendations. Moss Adams thinks that Jeffco’s annual financial audit “does not validate the compliance of expenditures per the bond language or closely evaluate the Bond Program. Best practice suggests that an annual independent performance audit should be performed to ensure that funds are expended only on the specific projects listed in the bond measure.”

Voters’ expectations were that a separate and independent financial audit would have taken place. The former auditor, CLA’s Paul Niedermuller was not independent. He had a financial interest in keeping the district’s regular auditing business which a bad audit of the bond program might put into jeopardy.

At this point, no one knows how much of the bond program has been subjected to auditing. Over the past 5 years the bond program has not been mentioned once in the CAFR.

The second Moss Adams review was not an audit. It was also rife with errors, so many in fact that Moss Adams had to redo the initial report they gave to the Board of Ed. You can ask either me or CFO Copeland for my analysis of these reviews if you want more info.

Complete annual Financial and Performance Audits should have been conducted on the program as prescribed by Best Practice and Moss Adams. Failure to conduct these audits is a major Red Flag and is indicative of the district attempting to hide something. The district can never be trusted with another bond program if full Forensic Financial and Performance Audits are not conducted on this program.

Observation 4 – Bond Program Project Scope and Budget Establishment: Jeffco reported that the Bond program was based on the 2016 Master Plan. However, the planning documents did not align with the program’s budget or 2018 Flipbook which was shown to voters.

Recommendation A – Jeffco should ensure that all foundational documents and reporting align and can be reconciled.

Recommendation B – Jeffco should define and document processes in place for master planning budgets and estimate.

Area of Concern – Once again, Jeffco has not fulfilled this recommendation. Moss Adams – Nothing aligned. “Both the 2016 Master Plan and the 20190110 H Bond Cash Flow (version 1).xlsb documents provided insufficient information to support the suite of projects included in the Bond Program.”

The documents did not reconcile to the 2018 Flipbook.

None of the documents presented to the Board and public reconcile.

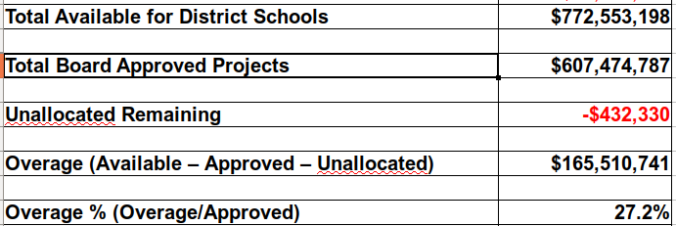

This is a huge issue. Nothing reconciles. 5+ years later and it is impossible to get any of the numbers that staff present to the CAAC or Board to even reconcile with the 2018 Flipbook. Impossible! That is not transparency and prevents a fair evaluation of the management of the bond program.

Observation 5 – Project Identification and Voter Transparency: Jeffco developed the Flipbook to inform parents and the community. However, the Flipbook did not reconcile to the bond issuance or key documents.

Recommendation – Jeffco should ensure that there is clear and consistent reporting that provides stakeholders with accurate information with clear reconciliation.

Area of Concern – Jeffco failed to fulfill this recommendation. Moss Adams – Nothing reconciled. Successful bond programs provide specific information. The Flipbook and community information should be up-to-date and consistent to promote accountability and transparency.

Even the latest Flipbook, developed 15 months after this recommendation, contained misleading, inaccurate and missing information. And it’s replacement, the interactive map, has an immense amount of missing information and budget numbers that do not align with the 2018 Flipbook. It is a Master Class in deception and cover-up.

Observation 6 – CAAC Oversight: No additional guidance related to the Bond Program oversight or reporting expectations was provided to the CAAC.

Recommendation A – There should be CAAC bylaws and a handbook

Recommendation B – Best practice is that there should be a CAAC Chair.

Area of Concern – Jeffco failed to fulfill this recommendation. Moss Adams – Bond language stated that the bond program would be monitored by the CAAC. Jeffco had no written guidance on monitoring of the bond program. Only projects with variances over $500,000 were eventually reviewed. Best practice is that projects with 10% or $1M in variances should be reviewed.

It took over 18 months to finally get CAAC bylaws and still the committee doesn’t have a Chair. Why isn’t there a Chair? There is no way a committee that didn’t follow the recommendations itself can evaluate the full extent of whether the district fulfilled the complete set of Moss Adams recommendations.

Observation 7 – Flipbook and System Data Comparison: Projects were not included in the Flipbook and budgets exceeded Flipbook budgets.

Recommendation A – District needs policies and procedures to ensure consistent estimating, reporting, accountability and communication.

Recommendation B – Reporting to stakeholders should be updated to accurately provide details on all projects as well as budget and scope changes.

Area of Concern – Jeffco failed to fulfill this recommendation. Moss Adams – Projects were not identified in Flipbooks, budgets weren’t adhered to. This continued on through the end of the program.

Observation 8 – Completed Project Budget Analysis: Majority of projects exceeded original budget, many by more than $500,000.

Recommendation – District should develop and provide specific reporting to help stakeholders understand budget and scope variances.

Area of Concern – Jeffco failed to fulfill this recommendation. Where is the specific reporting that helps stakeholders understand budget and scope variances? The monthly CAAC report doesn’t link back to the 2018 Flipbook. No one understands why the program is $160M over original, budget estimates.