In 2018 Jeffco told the community that they would be undertaking $563M of capital projects at district facilities.

This included about $545M in projects at ~140 district schools that were very clearly identified in the 2018 Flipbook and another approximately $18M in undisclosed projects that later turned out to be for the Outdoor Labs, Trailblazer, North Transportation center and several other projects.

Sometime between November 2018 and late 2019 the estimated costs in the Flipbook increased by approximately $30M and those numbers are now used as the “Original” budget numbers. Now, every single “Original” budget estimate and Variance shown to the Board, CAAC and taxpayers is a blatant lie. Those aren’t the “original” numbers. This is because the numbers used are based on the costs already inflated by $30M, not the numbers that taxpayers voted on and expected from the program.

Moss Adams identified this as a major issue and recommended that all reports align back to the foundational documents such as the H Bond cash flow spreadsheet and 2018 Flipbook. Unfortunately, 15 months later that still hasn’t happened. In fact, the latest Flipbook published by Jeffco is more misleading, inaccurate and deceptive than ever.

Now, all of the $86M in program contingency has been used and only $50M of $118M in bond premium remained in November before ROTS savings started to impact the CAAC report. That is $154M over the original budget and until only recently the Board and CAAC have only approved one out-of-scope project, the D’Evelyn addition.

On Friday, CFO Copeland and Interim COO Suppes will continue with the cover-up of the overages and mismanagement and perpetuate the lies and deception that have been present in reports ever since the bond passed.

Here are some examples of the blatant lies in their report (here) or here if they update it.

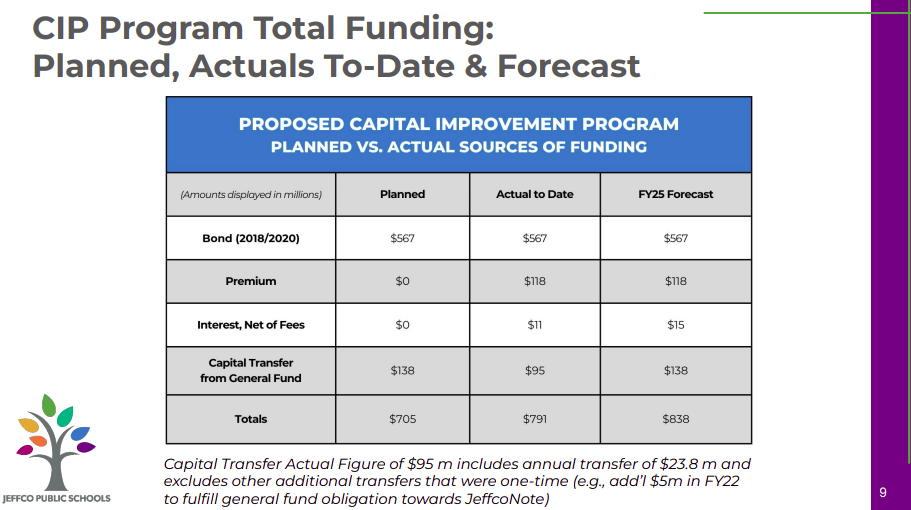

From Page 9 of the presentation.

Lie Number 1:

Capital Transfer into the CIP – $23.8M per year is NOT getting transferred into the Capital Improvement Program. $23.8M per year is going from the General Fund into the Capital Reserve Fund, but $3.2M/year is being siphoned off to pay for previous COPS, and in 2023-24 an additional $1.1M/year will be siphoned off for the Meyers Pool. Up until this year only $20.6M of the promised $23M transfer is making it into the CIP and next year that will be reduced to only $19.5M. This slide falsely represents what has actually happened with the Capital Transfer into the CIP. At the end of the program, the CIP will have been shortchanged by over $17M from the $138M that was originally promised to taxpayers.

Page 3 of the presentation states:

“We have added an estimated $82.8M in new scope and additional uses” and then list those. Most of the items they include in the new scope and additional uses are misleading and downright false. $34,102,610 more closely represents the amount of additional scope and new uses of funds, a far cry from the $82.8M staff want people to believe. See below for details on this deception

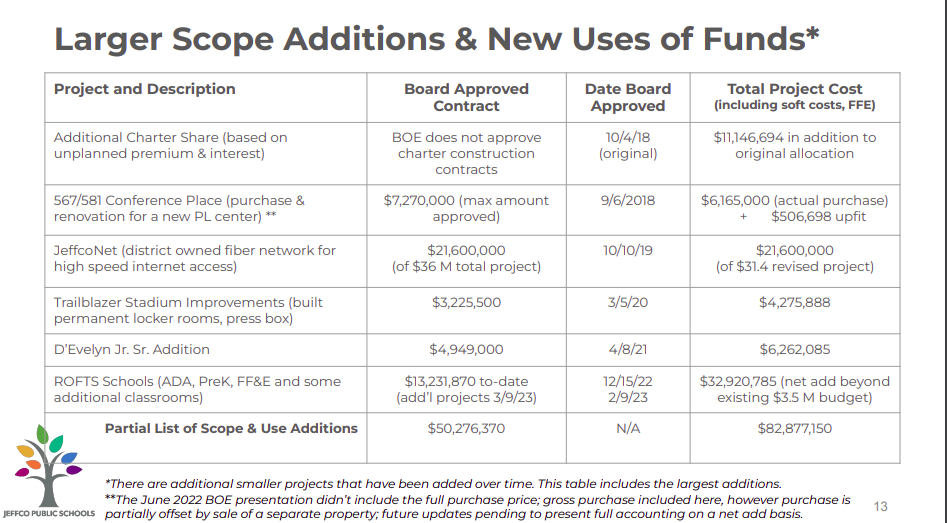

From page 13 of the Presentation:

There are numerous lies and deceptive comments on this page.

Deception Number 1:

Additional Charter Share – $11,136,694. The Board agreed that Charters would get their proportionate share of all bond proceeds. This is their rightful share of the bond premium and interest. To attempt to characterize this as New Scope or New Uses of Funds is deceptive and does not take-away from the fact that Jeffco is projecting that it will get nearly $122M in bond premium and interest over and above original revenue projections for just District projects. This is not a new use of funds, this is merely a reduction in revenue Jeffco received.

Lie Number 2:

567/581 Conference Place (purchase and renovation for a new PL center) – This is flat out lie. Note the date – 9/6/2018. This is before the bond passed in November 2018. In addition, this purchase has never appeared in ANY CAAC document relating to uses of CIP funds.

Lie Number 3:

JeffcoNet – $7M for JeffcoNet was included in the bond program budget reducing the amount that should be shown as Additional Scope or New Additions. Also, $5M was added in additional Capital Transfer in FY 22 to help offset the $14.6M remaining in JeffcoNet costs that were transferred to the CIP. Therefore the net Scope Additions and New Uses of Funds for JeffcoNet is actually $9.6M, not $21.6M as falsely stated in this presentation.

Lie Number 4:

Trailblazer Stadium – The renovation of Trailblazer stadium was always included in the original $563M in projects. It wasn’t disclosed to voters, but the January 2021 Askelson report and my own CORAs show that work for Trailblazer was included in the $18M in projects that were not originally disclosed to voters. This is not a Scope Addition or New Uses of Funds.

Deception Number 2:

D’Evelyn Addition- The D’Evelyn construction contract included not only the addition, but also already planned, and budgeted, Efficiency & Future Ready items that had a base bid of $777,000. CAAC reports show budgeted funding of $870,082. Therefore, the real cost of the D’Evelyn addition in added scope costs is $5,392,003, not what is shown on the presentation.

Deception Number 3:

ROTS Schools – This presentation wants everyone to believe that $32,920,785 in scope was added to the CIP. Yet, in every other presentation to the Board staff subtract from that number the amount saved from projects that are not going to be done at closing schools. In the February 9, 2023 presentation, staff told the Board that ROTS Schools were only going to cost the district $19,200,607 in additional costs. That is the same number that should be shown here.

The more accurate number for Scope Additions and New Uses of Funds is $34,102,610, not $82,877,150 that Jeffco staff wants people to believe. Jeffco staff is trying to inflate this number to hide the true magnitude of cost overruns and mismanagement in the CIP.

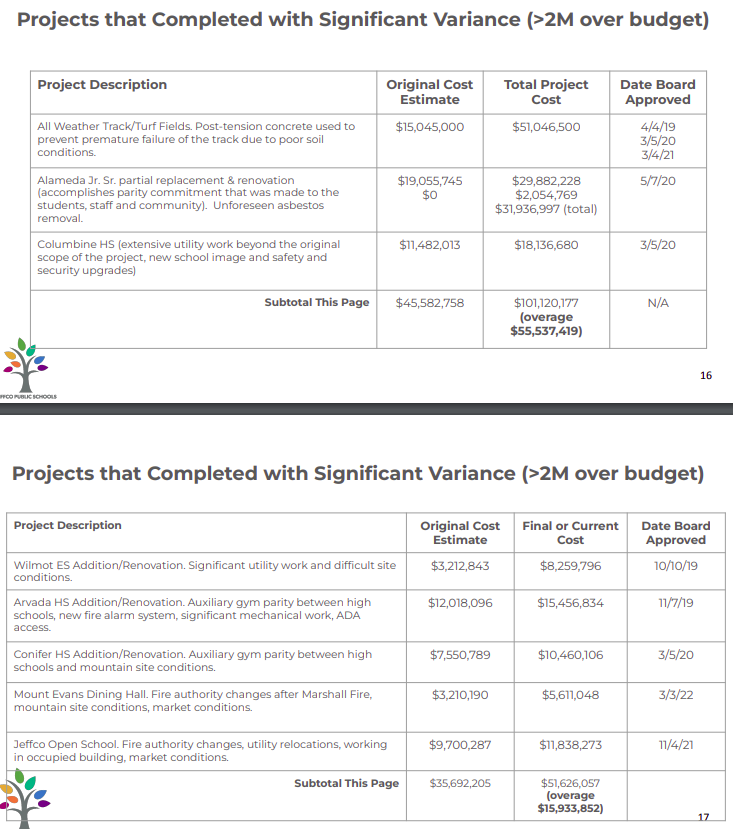

From Page 16 and 17 of the Presentation:

Lie Number 5:

Alameda Jr/Sr HS – The Original Cost Estimate shown to voters was $18,003,098, not the $19,055,745 shown in this presentation. This merely highlights how sometime in 2019 Jeffco inflated most project cost estimates and has been hiding $30M in cost overruns ever since.

Lie Number 6:

Jeffco Open School – The Original Cost Estimate shown to voters was $9,307,490, not the $9,700,287 shown in this presentation for the same reason described above for Alameda.

From Page 24 of the Presentation

Unbelievable Statement Number 1:

Jeffco is going to hire a consultant to reconcile the current actual and forecasted spend of all CIP projects.

What, after 4+ years of the program, Jeffco doesn’t have these numbers in a readily available format and that are reliable? This is just incredible. Basically, Jeffco is saying that everything they have told the Board and community over the past 4 years can’t be trusted at this point in time.

Unbelievable Statement Number 2:

Jeffco is going to engage a consultant to improve the program financial reporting.

This is just a shocking statement. Moss Adams Recommendation Number 5 said that Jeffco should improve the financial reporting. 15 months later Jeffco is just now getting around to say they may do something about this in the future? Better late than never people say. But wasn’t SE2 hired to do this exact same thing last April? What did they do for their $100k+ contract? Something is not right here.

Unbelievable Statement Number 3:

Jeffco is going to review all in-process and not-yet-started projects in the CIP and update the forecast-to-complete amounts.

To not already have this information only highlights the total incompetence of Jeffco staff. You can’t make sound financial decisions if you don’t update your forecasts when you have rampant inflation. This should have been done on a continual basis for all projects since the beginning of the program. The incompetence is truly unbelievable.

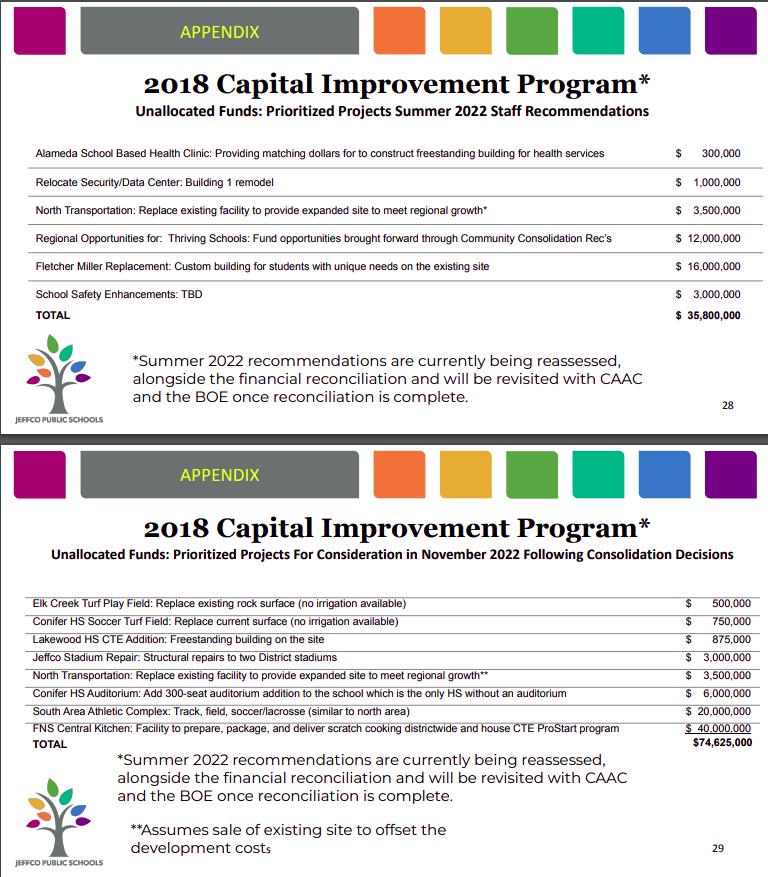

From Pages 28 & 29 of the Presentation:

Sad Fact:

The projects on these 2 pages total $110M. Jeffco is forecasting netting $122M for district projects from the bond premium and interest. How many of these Unfunded Priorities could have been completed if Jeffco had managed to its original budget and $86M in Program Contingency?

Most of them. We’ll see how little is left after the Friday presentation. Nonetheless, this is what the bond premium and interest should have been used for.

This presentation to the Board has so much deception, so many lies and so many unbelievable statements that Suppes and Copeland are either completely incompetent or they themselves are involved in the massive cover-up of the mismanagement and cost overruns in the program. In either case, they are demonstrating that they are clueless about the CIP and that the only way Jeffco is ever going to know the full truth about the CIP and prevent this from happening again is with a full Forensic Financial Audit and Performance Audit. After taking a critical look at this presentation I think we all know why Jeffco is resisting performing these standard oversight functions.