Here is a video documenting how Jeffco schools is failing to fulfill its 2018 campaign promise of contributing $138M in Capital Transfer to the bond fund and subsequently embarked on a deliberate and deceptive scheme to hide that fact from the Board and public.

Watch this video to gain a better understanding of just some of the deception and lack of transparency that has been pervasive in the bond program since its inception.

I find this unacceptable. However, once I saw this I now fully understand why Dorland and the Board have avoided having full performance and forensic financial audits performed as recommended by the first Moss Adams report. Because of that inaction, they are now active participants in the cover-up of the mismanagement of the bond program.

This is also why it will be a very long time before Jeffco regains my trust to vote for another bond.

The latest version of the November Moss Adams report was inaccurate, delivered no value and provides even more evidence for why full forensic and performance audits are needed on the Capital Improvement Program. This doesn’t even take into account the version of the Moss Adams report that was given to the Board in November that was rife with literally dozens of errors.

For months the expectations were set that the Moss Adams report would give the Board and district an accurate number for the amount of money remaining in the Capital Improvement Program. Ideally, this number would have tied directly back to the monthly CAAC report and even better, it would have provided totals of how much has been spent on each school. The Moss Adams report achieved none of these expectations. Instead, what the Board got was a rambling 73 page document and a meaningless “$74M Remaining to be Committed” number.

That $74M “Remaining to be Committed” number was meaningless for a number of reasons:

It was 7 months old and was not accompanied by a staff reconciliation to bring it up-to-date

It was an aggregate remaining capital funds number and did not separate out CIP funds from regular Capital Reserve Fund funds

It did not factor in CIP committed projects that have not yet been started and entered into the district’s financial systems. For instance, until a formal decision is made otherwise, Jeffco is still committed to building 2 new elementary schools, for which Tim Reed has allocated $59.6M. These are accounted for in the CAAC report, but not the Moss Adams report. In addition, the Moss Adams report did not account for the $10M in upgrades for Bergen Valley for ROTS I or many other unstarted projects.

The report contained errors and its methodology did not align with the manner in which Tim Reed develops the monthly CAAC report. For instance, page 17 of the report lists a Meyers Pool project at more than $500k as a “School-Specific Project”. That is absolutely incorrect and calls into question the accuracy and validity of every other single number in the report.

A reasonable expectation would have been that Jeffco staff would have taken this report and reconciled it with the CAAC report to identify if there were any discrepancies and to arrive at exactly how much money was currently left in the bond program. Shockingly, that didn’t happen. The response I received when I asked for that reconciliation as part of CORA Request PR-2324-177 was the following:

Our subject matter expert provided that the transaction level detail that we’ve already shared with you is drawn directly from the accounting system – which is the same system driving the CAAC reports.

If there was no reconciliation, what was the purpose of the Moss Adams review? What exactly did Jeffco schools get out of the close to $200k that Moss Adams was paid?

Second, there were several discrepancies between the Moss Adams report and the CAAC report. Yes, I realize that the Moss Adams report was conducted from a point in time, but my examples transcend the time issue. Note also that I only looked at approximately 25 projects that were listed as “100%” on the April 2023 CAAC report, the month Moss Adams used as their baseline.

Moss Adams identified $185,156 in actual expenditures for the Sheridan Green ES FF&E project. Yet, from at least March 2023 to November 2023 the CAAC report states that the project only has a cost of $173,067 in costs. Did Moss Adams make up expenditures or is the CAAC report wrong? How many other discrepancies like this are there? A full reconciliation with the CAAC report should have been performed to identify issues such as this.

Moss Adams used Project Commitments, or “Costs approved with executed purchase orders or contracts” to determine the total project cost. There are numerous instances of where the Moss Adams number does not reconcile with numbers reported in the CAAC report. Take as one example the Kendrick Lakes FF&E project that was listed as “100% Complete” in the March 2023 CAAC report with a cost of $612,175. This project is still listed at that same cost in the November 2023 CAAC report. Yet, Moss Adams reported Commitments for that project at $628,563. This would result in the Moss Adams report over-stating project costs and under-stating the remaining available funds. Once again, this discrepancy is not identified unless a full reconciliation to the CAAC report is performed.

There are numerous instances of where costs listed on the CAAC report exceed project Commitments on the Moss Adams report. This is possibly understandable as project costs may have increased, but these discrepancies contribute to the inaccuracy of the Moss Adams number with relation to the CAAC reported number which, once again, are only resolved through a complete reconciliation.

Finally, the report highlighted some very troubling aspects of the bond and capital programs.

1. The report identified more than $34M in “Other Expenditures” from the Capital Fund and then went on to define “Other Expenditures” as:

OTHER EXPENDITURES

Other program charges not project-specific or not yet allocated to projects and debt service costs (i.e. ProjectID P91700P98A and P000000001). These costs include, but are not limited to, the following expenditurecategories: vacation, software and IT, interest payment, cell phone and telephone, printing and copying, loanpayoff, advertising, mileage, and payroll.

“Vacation”, “payroll”? Other than debt service, these expenditures sound very suspicious and have the indications of being an unaccountable slush fund.

2. Moss Adams identified close to an additional $55M in “Other Expenditures” just in the CIP projects. This money is not used for interest or debt service, so what was all of this money used for? Isn’t that a question that should be answered? That’s an awful lot of money.

3. There is an additional $12M in district projects where contract costs were less than $50k and were not validated by Moss Adams. These small expenditures and contracts are areas ripe for fraud. Has anyone seriously looked at them?

4. There are multiple questionable projects that show up in the Moss Adams report. Projects such as $212k for the Candelas Regional Trail and $115k for the Meyers Pool parking lot. Why is Jeffco spending one cent more than the $17.5M already committed for the Meyers Pool? Who approved these when Jeffco has to go begging for money to replace Fletcher Miller?

The bottom line is that the Moss Adams report provided absolutely zero insight into the key question of how much unallocated money remained in the CIP. It did however prove, once again, that both a full forensic audit and a performance audit, as recommended by Moss Adams in their first report, need to be performed as there are just far too many troubling aspects surrounding the $160M over budget Capital Improvement Program.

Jeffco is covering up a fraud allegation of the CIP

On April 18, 2023 I sent an allegation of fraud related to the movement of $21M of the JeffcoNet project into the CIP to Jeffco’s CFO for forwarding to members of the Financial Oversight Committee.

Specifically, in October 2019 the Jeffco Board approved a $36M contract for the construction of a district fiber network. The agenda item stated that 60% (or $21.6M) of the funding for the contract would come from the “Building Fund Capital Reserve”. The source of this funding was distinctly different than other agenda items that evening that stated their funding would come from the 2018 Capital Improvement Program. In other words, JeffcoNet would not be funded from the CIP.

However, more than 2 years later a $14.6M Network Upgrade project with an Original Budget of $0 appeared on the monthly CAAC report. And, upon closer examination, the CAAC’s financial report had been showing a similar, but funded, Network Upgrade project with a cost of $7M.

The total cost of these projects, $21.6M, is the exact same amount for JeffcoNet that should have been funded by the Capital Reserve Fund when the Board initially approved it.

To recap, the Board voted on an agenda item which stated the funding for the project would come from the Capital Reserve Fund, yet somehow, without public Board discussion or authorization the complete $21.6M made its way into the Capital Improvement Program.

To make matters worse, the line from the CAAC report shows a note of “BD’ implying to the CAAC that the addition of this project to the program was “Board Directed”. That does not appear to be the cases and is deceptive.

To be clear, I do not disagree that Jeffco has the ability to add and delete projects from the CIP. However, I do believe that it is a violation of trust and fraudulent to move the funding for a project that the Board explicitly directed to come from the Capital Reserve Fund into the CIP without Board approval. The Association of Certified Fraud Examiners would call this “Internal Organizational Fraud” or “Occupational Fraud”.

What this does is destroys trust. The Board can no longer trust District leadership to carry out their directions and instructions and the public can no longer trust anything the Board says or directs.

Therefore, in my note to the FOC, I requested that they initiate an independent external investigation of the transfer of the project which clearly violated the Board’s vote.

The FOC discussed my note at their April 25th, 2023 meeting. However, from the Meeting Minutes you would never know that it was an allegation of fraud. Here is what was written in the minutes:

Meeting Wrap-up

District leadership made committee members aware of communication that was sent regarding the JeffcoNet project. The committee discussed the issue raised with district leadership. The Board is aware of the communication and that district leadership is taking next steps to reconcile the Capital Improvement Program per the Board’s direction. District staff will continue to monitor the financial wellbeing of the Capital Improvement Program.

There was apparently no discussion of the potential fraud, no apparent discussion on whether the movement of the project into the CIP was supported by a vote or policy, only that the Board was aware of the communication and, in a complete misdirect, that the district is taking steps to reconcile the CIP.

That is a complete cover-up of the fraud allegation.

To make matters even worse, not one person contacted me, either before the meeting or afterward to let me know that my email had been discussed and its resolution even though they had my email address and I clearly included my telephone number. In addition, I had previously emailed the chair of the FOC, Jessica Keene, 3 times in November 2022, December 2022 and February 2023 about the same issue and she never once had the courtesy to even acknowledge receipt of my emails.

Jeffco’s FOC is a joke. They are providing ZERO oversight. They are now, along with meeting attendees Board member Danielle Varda, Superintendent Dorland and CFO Copland, complicit in an apparent cover-up of a fraud allegation in the district.

We can now add CFO Copland to the long list of people who have deceived the Board of Education on multiple aspects of the Jeffco Schools Capital Improvement Program.

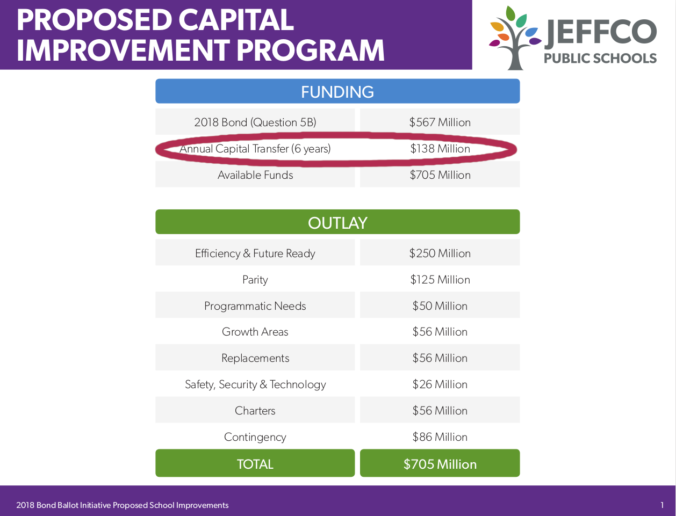

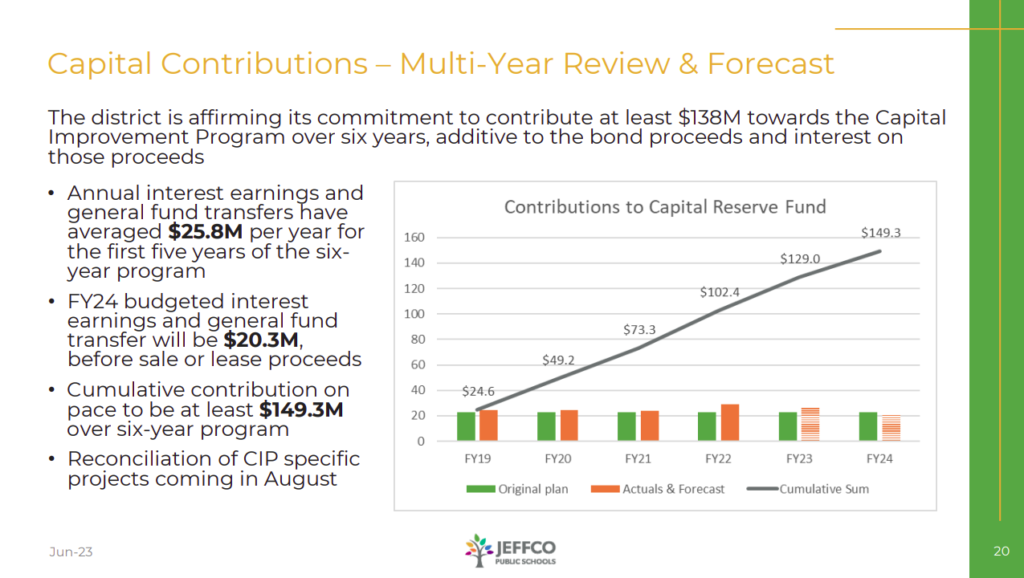

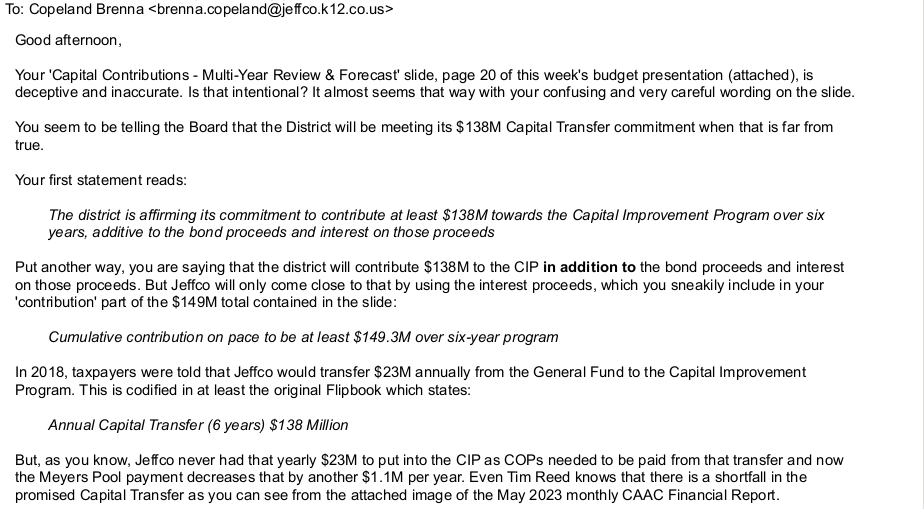

On June 7, 2023 she included the following slide in her budget update presentation.

She states:

“The district is affirming its commitment to contribute at least $138M towards the Capital Improvement Program over six years, additive to the bond proceeds and interest on those proceeds.”

Unfortunately, $138M in Capital Transfer is NOT going into the Capital Improvement Program.

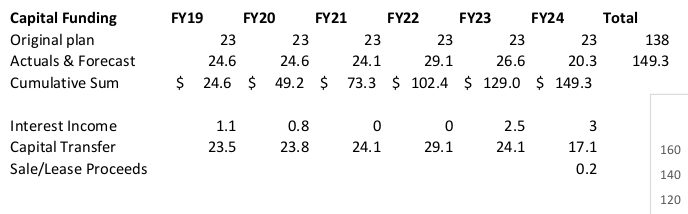

Here is an image of the CORA response I got from Jeffco when I asked for the data that CFO Copland used to create her chart.

You’ll see the annual Capital Transfer amounts.

However, this is NOT the amount that was transferred into the Capital Improvement Program.

The amount transferred into the CIP is less than the amount of Capital Transfer due to the fact that the capital transfer amount must also be used to pay for Certificates of Participation and starting this year the payment on the Arvada Community Pool loan.

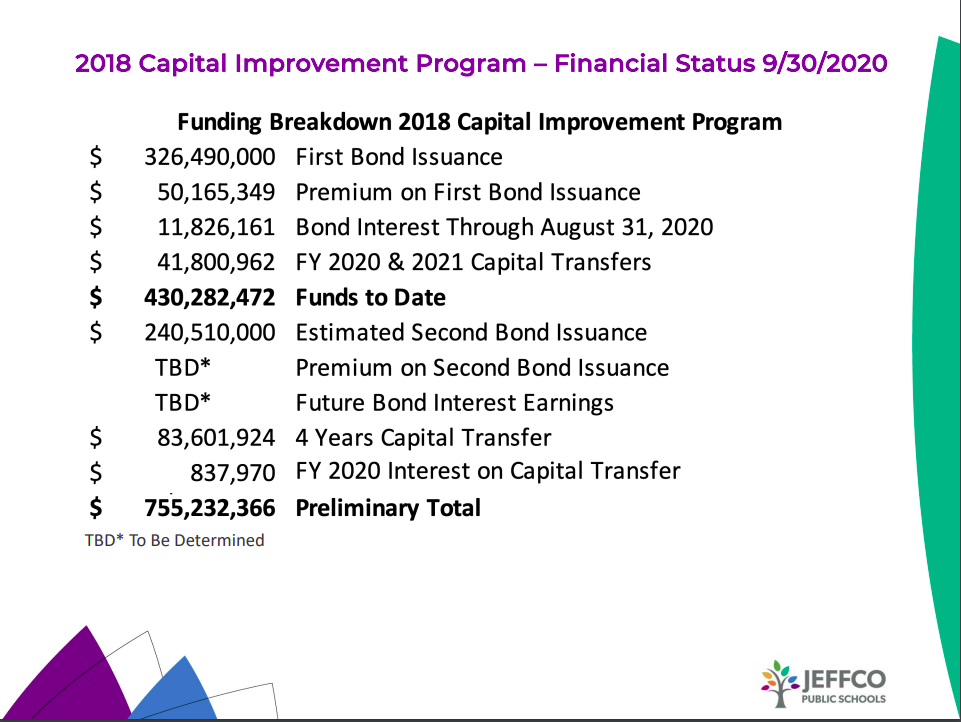

Even former CFO Askelson recognized this with her bond review document as well as Tim Reed with his monthly CAAC reports.

Here is Askelson’s report:

And here is Reed’s October 2020 Board presentation mentioned by Askelson:

You can see that Reed is telling the Board that $41.8M for FY 20 and FY 21 have been transferred into the Capital Improvement Program ($20.9M/year)

That does not align with what Copland recently told the Board in 2 ways.

First, Reed told the Board that the first year of Capital Transfer into the CIP was FY 20, not FY 19 that Copland is telling the Board.

Second, Reed, with the concurrence of Askelson, told the Board that $41.8M was transferred into the CIP for FY 20 and FY 21, not $48.7M that Copland is telling the Board.

Copland is making things up. She is flat-out deceiving the Board. There is something very, very wrong with that. She gets paid a lot of money to make sure numbers are correct and that the information she gives to the Board is accurate. Her June 7, 2023 presentation was pure deception. And, since I sent her an email about this well before the Board meeting she was aware of potential inaccuracies.

Yet, she went and presented the false information anyway. That’s lying in my book.

The truth is that now, due to the COPs and the Arvada pool, Jeffco will be short-changing the Capital Improvement Program more than $15M in promised Capital Transfer and Copland is trying very hard to hide that.

What else is she hiding in her fairy tale revisionist history and shell-game financial accounting? There is no excuse for any of this.

Jeffco's February 2023 CIP Update is full of deception, lies and unbelievable statements.

In 2018 Jeffco told the community that they would be undertaking $563M of capital projects at district facilities.

This included about $545M in projects at ~140 district schools that were very clearly identified in the 2018 Flipbook and another approximately $18M in undisclosed projects that later turned out to be for the Outdoor Labs, Trailblazer, North Transportation center and several other projects.

Sometime between November 2018 and late 2019 the estimated costs in the Flipbook increased by approximately $30M and those numbers are now used as the “Original” budget numbers. Now, every single “Original” budget estimate and Variance shown to the Board, CAAC and taxpayers is a blatant lie. Those aren’t the “original” numbers. This is because the numbers used are based on the costs already inflated by $30M, not the numbers that taxpayers voted on and expected from the program.

Moss Adams identified this as a major issue and recommended that all reports align back to the foundational documents such as the H Bond cash flow spreadsheet and 2018 Flipbook. Unfortunately, 15 months later that still hasn’t happened. In fact, the latest Flipbook published by Jeffco is more misleading, inaccurate and deceptive than ever.

Now, all of the $86M in program contingency has been used and only $50M of $118M in bond premium remained in November before ROTS savings started to impact the CAAC report. That is $154M over the original budget and until only recently the Board and CAAC have only approved one out-of-scope project, the D’Evelyn addition.

On Friday, CFO Copeland and Interim COO Suppes will continue with the cover-up of the overages and mismanagement and perpetuate the lies and deception that have been present in reports ever since the bond passed.

Here are some examples of the blatant lies in their report (here) or here if they update it.

From Page 9 of the presentation.

Lie Number 1:

Capital Transfer into the CIP – $23.8M per year is NOT getting transferred into the Capital Improvement Program. $23.8M per year is going from the General Fund into the Capital Reserve Fund, but $3.2M/year is being siphoned off to pay for previous COPS, and in 2023-24 an additional $1.1M/year will be siphoned off for the Meyers Pool. Up until this year only $20.6M of the promised $23M transfer is making it into the CIP and next year that will be reduced to only $19.5M. This slide falsely represents what has actually happened with the Capital Transfer into the CIP. At the end of the program, the CIP will have been shortchanged by over $17M from the $138M that was originally promised to taxpayers.

Page 3 of the presentation states:

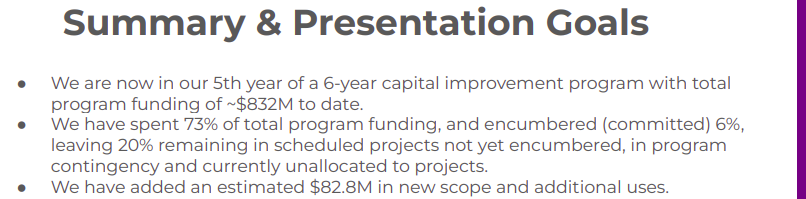

“We have added an estimated $82.8M in new scope and additional uses” and then list those. Most of the items they include in the new scope and additional uses are misleading and downright false. $34,102,610 more closely represents the amount of additional scope and new uses of funds, a far cry from the $82.8M staff want people to believe. See below for details on this deception

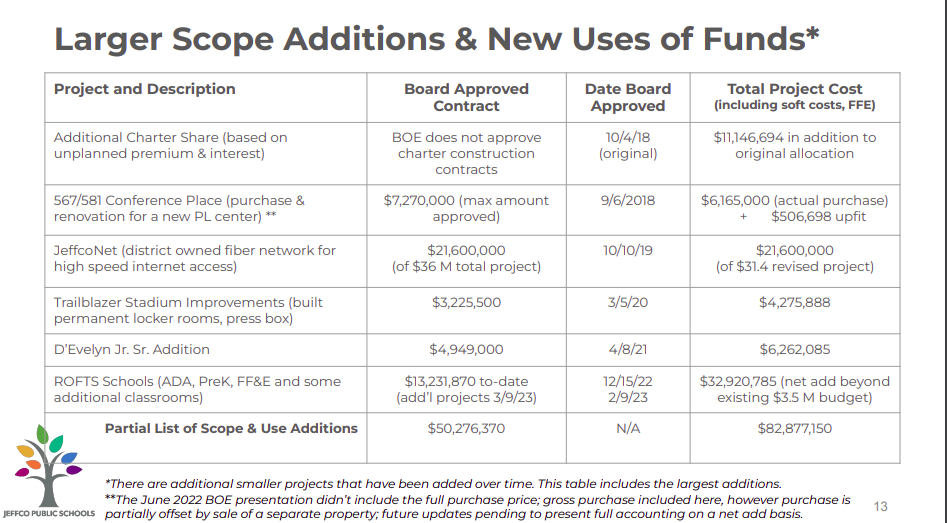

From page 13 of the Presentation:

There are numerous lies and deceptive comments on this page.

Deception Number 1:

Additional Charter Share – $11,136,694. The Board agreed that Charters would get their proportionate share of all bond proceeds. This is their rightful share of the bond premium and interest. To attempt to characterize this as New Scope or New Uses of Funds is deceptive and does not take-away from the fact that Jeffco is projecting that it will get nearly $122M in bond premium and interest over and above original revenue projections for just District projects. This is not a new use of funds, this is merely a reduction in revenue Jeffco received.

Lie Number 2:

567/581 Conference Place (purchase and renovation for a new PL center) – This is flat out lie. Note the date – 9/6/2018. This is before the bond passed in November 2018. In addition, this purchase has never appeared in ANY CAAC document relating to uses of CIP funds.

Lie Number 3:

JeffcoNet – $7M for JeffcoNet was included in the bond program budget reducing the amount that should be shown as Additional Scope or New Additions. Also, $5M was added in additional Capital Transfer in FY 22 to help offset the $14.6M remaining in JeffcoNet costs that were transferred to the CIP. Therefore the net Scope Additions and New Uses of Funds for JeffcoNet is actually $9.6M, not $21.6M as falsely stated in this presentation.

Lie Number 4:

Trailblazer Stadium – The renovation of Trailblazer stadium was always included in the original $563M in projects. It wasn’t disclosed to voters, but the January 2021 Askelson report and my own CORAs show that work for Trailblazer was included in the $18M in projects that were not originally disclosed to voters. This is not a Scope Addition or New Uses of Funds.

Deception Number 2:

D’Evelyn Addition- The D’Evelyn construction contract included not only the addition, but also already planned, and budgeted, Efficiency & Future Ready items that had a base bid of $777,000. CAAC reports show budgeted funding of $870,082. Therefore, the real cost of the D’Evelyn addition in added scope costs is $5,392,003, not what is shown on the presentation.

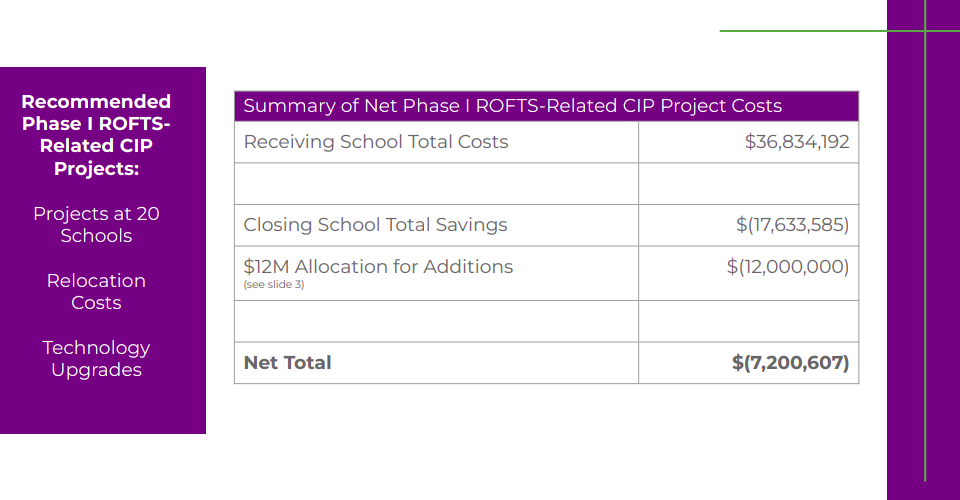

Deception Number 3:

ROTS Schools – This presentation wants everyone to believe that $32,920,785 in scope was added to the CIP. Yet, in every other presentation to the Board staff subtract from that number the amount saved from projects that are not going to be done at closing schools. In the February 9, 2023 presentation, staff told the Board that ROTS Schools were only going to cost the district $19,200,607 in additional costs. That is the same number that should be shown here.

The more accurate number for Scope Additions and New Uses of Funds is $34,102,610, not $82,877,150 that Jeffco staff wants people to believe. Jeffco staff is trying to inflate this number to hide the true magnitude of cost overruns and mismanagement in the CIP.

From Page 16 and 17 of the Presentation:

Lie Number 5:

Alameda Jr/Sr HS – The Original Cost Estimate shown to voters was $18,003,098, not the $19,055,745 shown in this presentation. This merely highlights how sometime in 2019 Jeffco inflated most project cost estimates and has been hiding $30M in cost overruns ever since.

Lie Number 6:

Jeffco Open School – The Original Cost Estimate shown to voters was $9,307,490, not the $9,700,287 shown in this presentation for the same reason described above for Alameda.

From Page 24 of the Presentation

Unbelievable Statement Number 1:

Jeffco is going to hire a consultant to reconcile the current actual and forecasted spend of all CIP projects.

What, after 4+ years of the program, Jeffco doesn’t have these numbers in a readily available format and that are reliable? This is just incredible. Basically, Jeffco is saying that everything they have told the Board and community over the past 4 years can’t be trusted at this point in time.

Unbelievable Statement Number 2:

Jeffco is going to engage a consultant to improve the program financial reporting.

This is just a shocking statement. Moss Adams Recommendation Number 5 said that Jeffco should improve the financial reporting. 15 months later Jeffco is just now getting around to say they may do something about this in the future? Better late than never people say. But wasn’t SE2 hired to do this exact same thing last April? What did they do for their $100k+ contract? Something is not right here.

Unbelievable Statement Number 3:

Jeffco is going to review all in-process and not-yet-started projects in the CIP and update the forecast-to-complete amounts.

To not already have this information only highlights the total incompetence of Jeffco staff. You can’t make sound financial decisions if you don’t update your forecasts when you have rampant inflation. This should have been done on a continual basis for all projects since the beginning of the program. The incompetence is truly unbelievable.

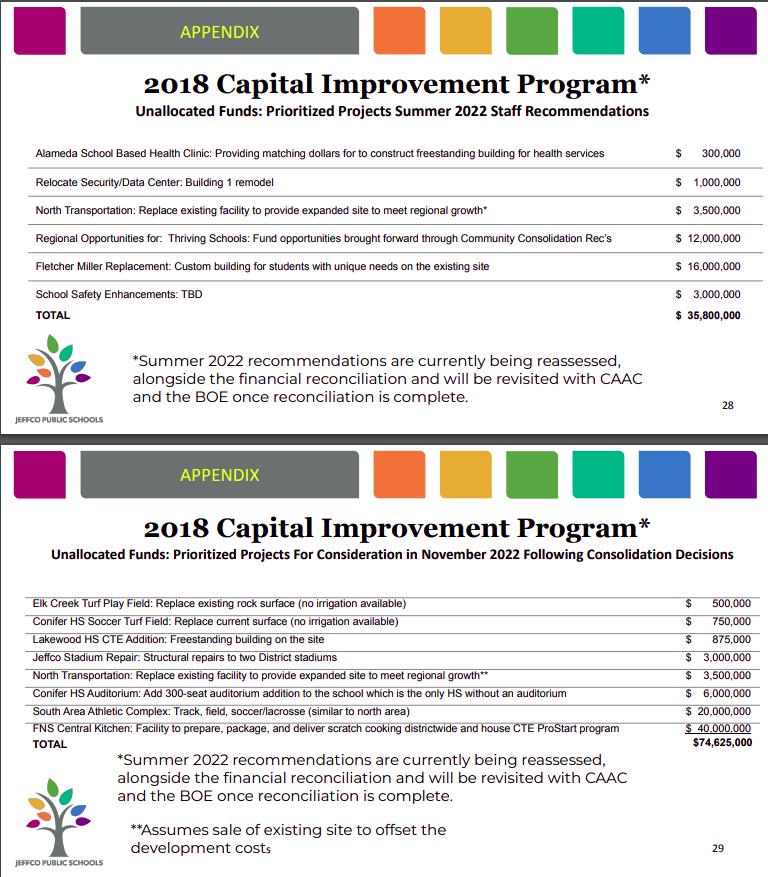

From Pages 28 & 29 of the Presentation:

Sad Fact:

The projects on these 2 pages total $110M. Jeffco is forecasting netting $122M for district projects from the bond premium and interest. How many of these Unfunded Priorities could have been completed if Jeffco had managed to its original budget and $86M in Program Contingency?

Most of them. We’ll see how little is left after the Friday presentation. Nonetheless, this is what the bond premium and interest should have been used for.

This presentation to the Board has so much deception, so many lies and so many unbelievable statements that Suppes and Copeland are either completely incompetent or they themselves are involved in the massive cover-up of the mismanagement and cost overruns in the program. In either case, they are demonstrating that they are clueless about the CIP and that the only way Jeffco is ever going to know the full truth about the CIP and prevent this from happening again is with a full Forensic Financial Audit and Performance Audit. After taking a critical look at this presentation I think we all know why Jeffco is resisting performing these standard oversight functions.

Jeffco's latest Flipbook is deceptive, inaccurate and incomplete

Jeffco’s bond program is currently $152M over budget, trending toward $170M, but you wouldn’t know that from Jeffco’s latest Flipbook .

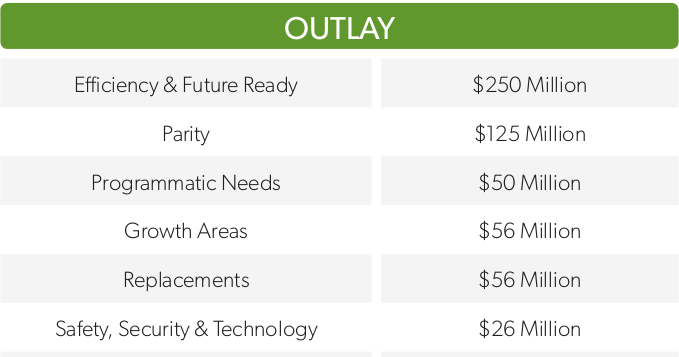

The original Flipbook told voters that Jeffco would be performing $563M worth of projects at District schools broken down into the following categories.

As of the October 2022 report to the CAAC, those $563M projects are now estimated to cost $715M.

That’s $152M over the original budget and the program is not yet complete.

The Moss Adams report came with a set of recommendations. Elements of 2 are highlighted below:

1. Recommendation 4 from the Moss Adams report very specifically stated:

A. To promote transparency and accountability, the District should ensure that all

foundational documents and reporting align and can be reconciled; updates

should be readily apparent in reporting documents through sufficiently detailed

project descriptions.

2. Recommendation 7 from the Moss Adams report very specifically stated:

B. Bond Program and management reporting to stakeholders, including the CAAC,

Board of Education, and community, should be updated to accurately provide

details on all projects as well as changes to project budget and scope from original

expectations communicated to the voters.

The 2016 District Wide Facilities Master Plan (2016 Master Plan) and the “20190110 H Bond Cash Flow (version 1).xlsb” were foundational to the establishment of project scope and budget and the Flipbook was the primary communication tool of the Bond Program to voters and interested stakeholders.

What we are going to see now, more than one year after Moss Adams delivered their damning report, is that Jeffco has not implemented these key report recommendations and continues to go out of their way to hide, obfuscate and deceive the public about key aspects of the Capital Improvement program.

Overall Budget

First and foremost, the latest Flipbook completely hides and ignores the original program budget number of $563M. Jeffco very carefully avoids using the word “budget” in this document, but appears to want to give the community the impression that the “budget” is $825M because $258M were added.

That’s not how budgets work. In 2018 voters were told that $563M of projects were going to be completed with $563M of revenue. The budget is $563M for those $563M worth of projects, no matter how much money Jeffco has or gets. That was the implied contract Jeffco made with taxpayers to obtain bond approval. To now imply that Jeffco is going to complete $563M worth of projects using $825M and attempt to deceive people into believing that is within budget flys in the face of all known business and financial management concepts. In actuality, it implies an attempted cover-up of mismanagement and over-spending.

As Moss Adams very clearly stated, all reporting should align and be reconciled to the original foundational documents. This new Flipbook doesn’t even come close with regard to the program’s overall budget.

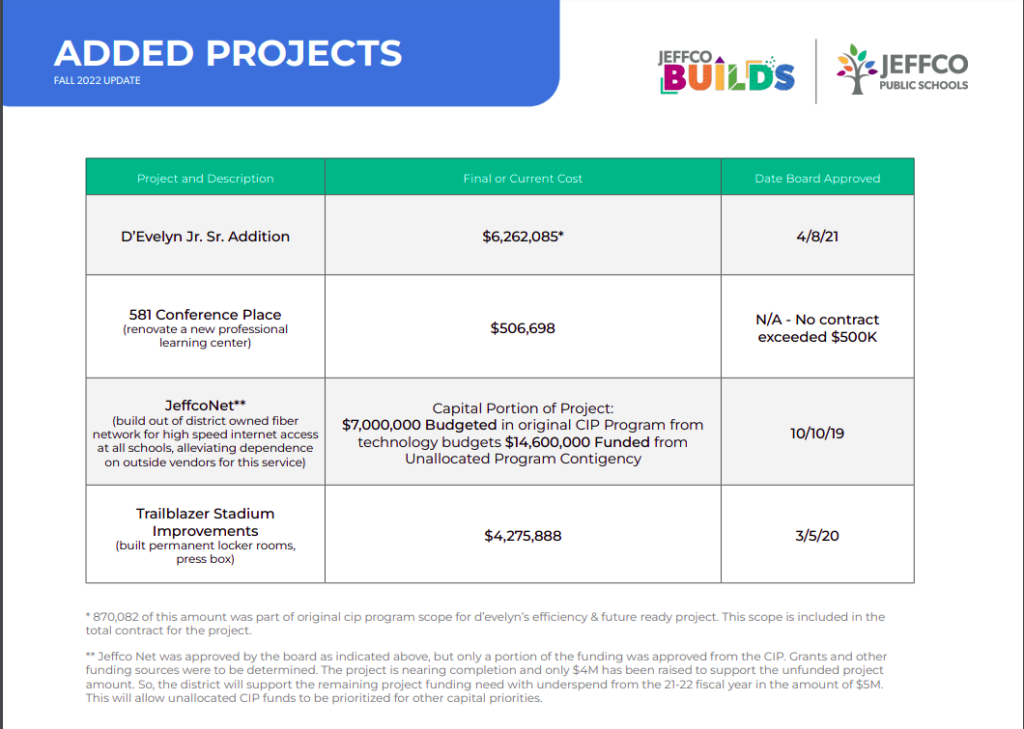

Added Projects

Jeffco’s latest Flipbook wants the community to believe that only 4 projects have been added to the program. That is completely false. The fact is that in the October 2022 CAAC report there are 33 projects that have a $0 Original Budget. That means that these projects weren’t part of the original plan and is a number that is far larger than the 4 shown in the new Flipbook.

To make matters worse, the Trailblazer Stadium project is NOT an added project. The Askelson report clearly stated that it was part of the program:

Central sites such as outdoor lab, stadiums and north transportation were not listed in

the flip book; however, the Board of Education was informed these sites were part of

the bond program. Meetings with Board members and the Chief Operating Officer

occurred May 4–11, 2018, to go over project scope in detail that included these central

projects. These projects were also in the 2016 District Wide Facility Master Plan which

served as the foundation for the 2018 Capital Improvement Program.

And if Jeffco now wants to claim that it wasn’t part of the program, what about the other 8 projects that Askelson says were part of the program that were not included in the original Flipbook? Why not show all of these projects, with estimated total costs of $19.5M, in the current Flipbook?

Projects not listed in the flip book:

North area transportation site

Trailblazer stadium

Windy Peak outdoor lab

Mt. Evans outdoor lab

20th & Hoyt

Patterson Cottages

Anderson Preschool

Litz Preschool

Irwin Preschool

In addition, it is an interesting admission that no approval was ever obtained to add the work at 581 Conference Place to the list of projects. Taxpayers were very specifically told that the bond money would be put into schools, yet the $7.4M for the North Transportation center, $4.3M for Trailblazer stadium and $500k for 20th and Hoyt/581 Conference Place were never disclosed to voters. That is the epitome of deception.

Finally, it is also interesting to note that $14.6M of the Jeffco Net project was never approved by the Board to come from the Capital Improvement Program. Read the word salad in the new Flipbook carefully. JeffcoNet project money should never have come from the CIP.

This is nothing but another attempt to deceive Jeffco voters and community members.

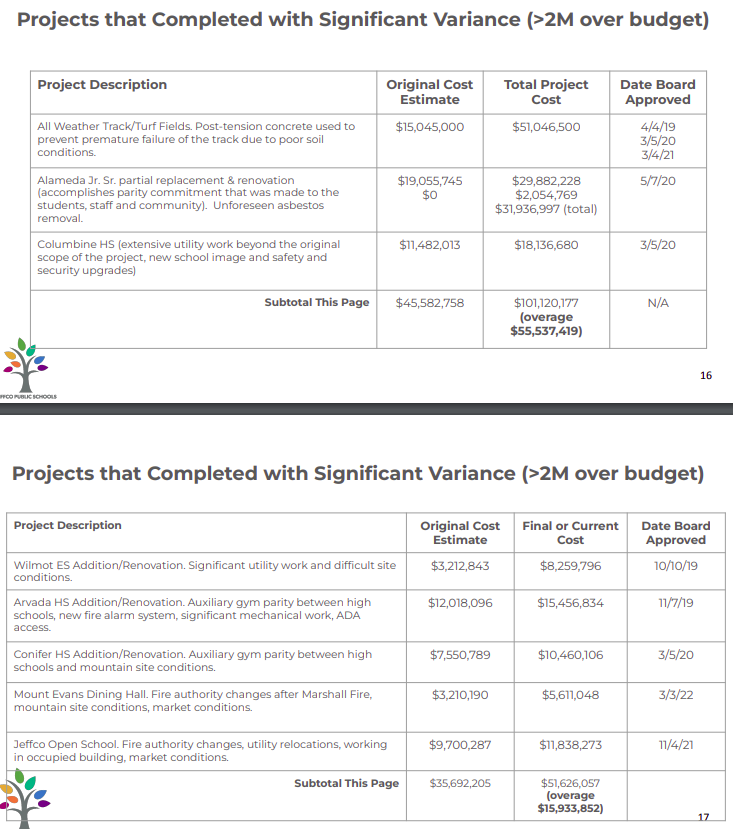

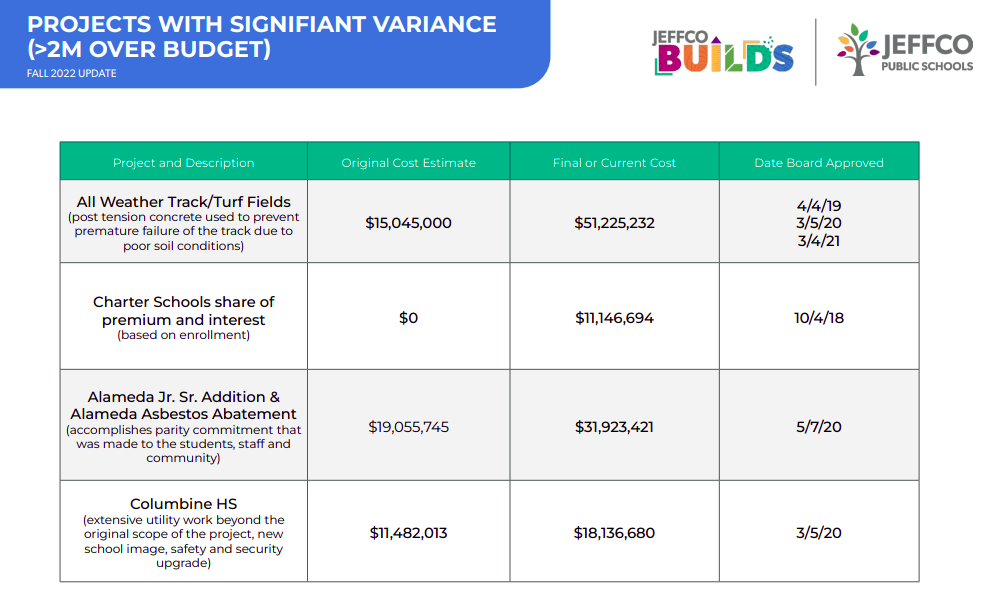

Over budget projects

It’s nice that Jeffco is making somewhat of an attempt to come clean with 8 projects that are more than $2M over budget each. But, $2M is just some large arbitrary number. Wouldn’t a more accurate measurement of how well the program is being managed be based on the number of projects that are some percentage over budget? There are currently 51 projects that are more than 50% over their original budget. That is more than 1 in every 5 projects coming in at over 50% over budget. That is just egregious and unacceptable. And every project already includes 10% contingency in the original budget. This ineptitude is what Jeffco is covering up by only showing projects that are $2M over.

To make matters worse, Jeffco wants people to believe that the $11.1M that Charter schools received from their rightful and Board directed share of bond premium and interest (on their own money) is somehow a “variance” and significantly contributes to Jeffco’s over budget bond program. That is far from the truth. That money belongs to the Charter schools and in no way contributes to the $152M in overages in Jeffco’s district run projects. Besides, this $11.1M is shared among 17 schools, so there is no $2M overage at any school. Deception, deception, deception – this new Flipbook is filled with it.

And where did Jeffco come up with the $15,045,000 Original Cost Estimate for the All Weather/Track/Turf Fields? The sum of the Original Costs for these 3 projects as shown in the October 2022 CAAC reports shows the Original Costs to be $23,445,000. Moss Adams said that everything should align and reconcile. This surely doesn’t. Is Jeffco incompetent or trying, once again, to hide something?

And it gets worse. Jeffco wants the community to believe that the original cost estimate for Alameda was $19,055,745. That is a complete lie. The Original Cost Estimate was $18,003,098. The same applies to Jeffco Open, where the Cost Estimate shown in the new Flipbook is larger than what was originally shown to voters in 2018. Once again, the new Flipbook is filled with lies and deception.

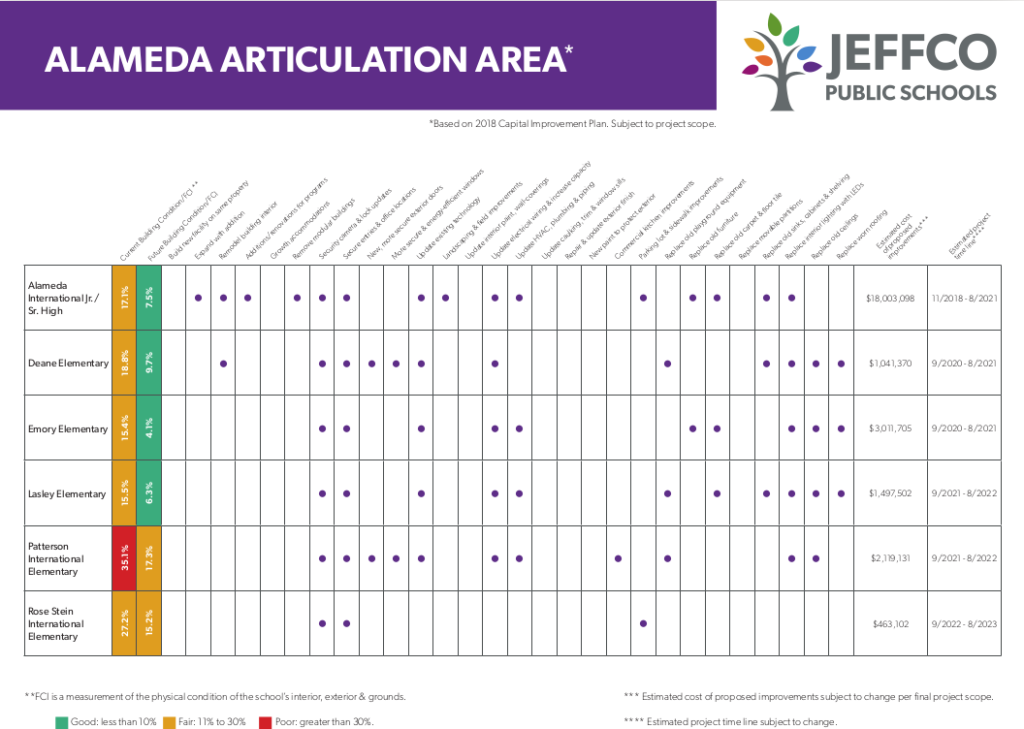

Lack of Costs by School and FCIs

The original Flipbook showed taxpayers estimated costs and FCIs by school as can be seen in the image above.

The most recent Flipbook does not.

This is not the transparency taxpayers were promised and is deceptive in that the community cannot determine if the projects and program is on budget and on track to deliver what was promised.

The latest Flipbook embodies everything that is wrong with Jeffco’s Capital Improvement Proram. It has inaccuracies, lies, deception, the removal of critical information people need to make their own evaluation of whether the program has been successful or not and doesn’t follow the Moss Adams recommendations of having data align and be able to be reconciled.

Jeffco schools should never be trusted again when they come and ask for another bond. Jeffco schools has not fulfilled its promises of transparency, honesty and good fiscal stewardship of our money.

It's false that $0 in bond money has been put into Bergen Meadow

Jeffco staff lied to the Board of Education and public regarding how much bond money was put into the ROTS closing schools.

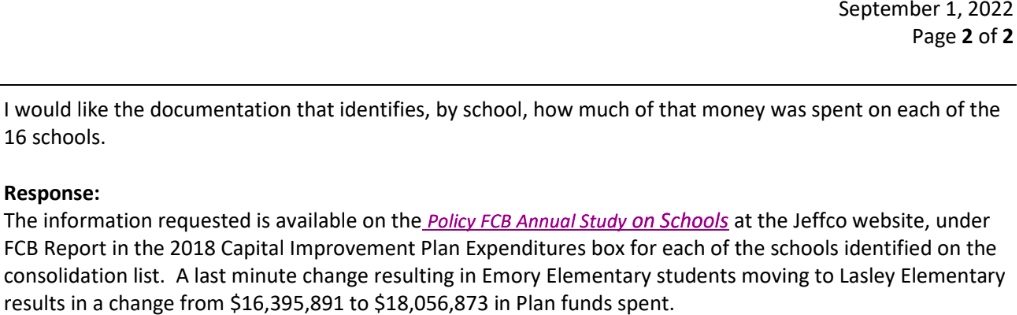

Jeffco staff told everyone that $16,395,891 in bond funds was put into the schools.

Staff falsely told Board that only $16M in bond money had been put into closing schools

Yet, in a September 1, 2022 CORA request Jeffco admitted that the information shown to the Board was incorrect and that the real amount was $18,056,873 due to a “last minute change”. The $18M number matches the sum of the amounts shown in the FCB for the closing schools.

But even after admitting this “error” staff never updated the information shown to the public and kept the $16M figure on their web site. That, in and of itself, is disingenuous and deceptive.

To make matters worse, the $18M isn’t the full amount of money put into the schools. It appeared that Jeffco only included costs associated with Efficiency and Future Ready projects at those schools and not costs associated with District wide projects. Therefore, I submitted a series of CORA requests for the breakout of costs of District wide projects that included the closing schools.

For example, I asked for a breakout of the by-school costs of the H DW Flooring project which included Bergen Meadow.

Jeffco’s CORA response was that this project included flooring that cost $289,188 that was installed at Bergen Meadow. Yet, Jeffco told the Board and the public that $0 of bond money was spent at Bergen Meadow.

This is just another flat-out lie.

To compound the issue there were numerous District wide projects that Jeffco could not or would not provide the by-school cost breakdowns. This prevents an accounting of the full amounts of bond money put into the closing schools. However, from what Jeffco did provide, the costs of District wide projects was more than $5M. Extrapolating for the projects in which costs were not provided means that the total was somewhere between $5M and $10M more than what Jeffco told the Board. This makes it likely that more than $25M of bond money, in total, was put into the closing schools. That is significantly more than the $16M told to the Board and community and taxpayers deserve to know that number.

The bottom line is that Jeffco staff repeatedly and knowingly lied to the Board and public. This is an egregious display of arrogance and deception.

Superintendent Dorland frequently says that she wants trust and transparency, yet she knowingly allows this type of deception to happen and does nothing to fix it. Because of this she is part of the problem and can’t be trusted.

Jeffco schools has a massive integrity and trust problem. There is nothing worse than that. Unfortunately, this problem won’t be fixed until the head of the snake is cut off and another round of cabinet members are fired and replaced with people who value integrity, honesty and transparency above all else.

Never Trust Anything Put Out by Jeffco!

The Jeffco Fiber Net project has $0 original budget, meaning it was not in the original scope.

In October 2019 Jeffco’s BoE approved a $36M contract, on the consent agenda without discussion, for the construction of a Jeffco Fiber Network. $21.6M of the funding for this would come from Jeffco’s Capital Reserve Fund with the remaining $14.4M from the IT dept’s budget and grants.

Board Docs very specifically stated that $21.6M would come from the Capital Reserve Fund, not the Capital Improvement Program. The bond had been approved by voters nearly a year before and numerous bond related projects up until that time flatly stated that their funding would come from the bond program. This item was different in that it stated funding was coming from Capital Reserve.

Yet, the ‘H DW Network Upgrades’ project subsequently appeared on the monthly bond program CAAC report in December 2019. When project costs first started to appear on the CAAC report in January 2021, this project came with a $7M price tag.

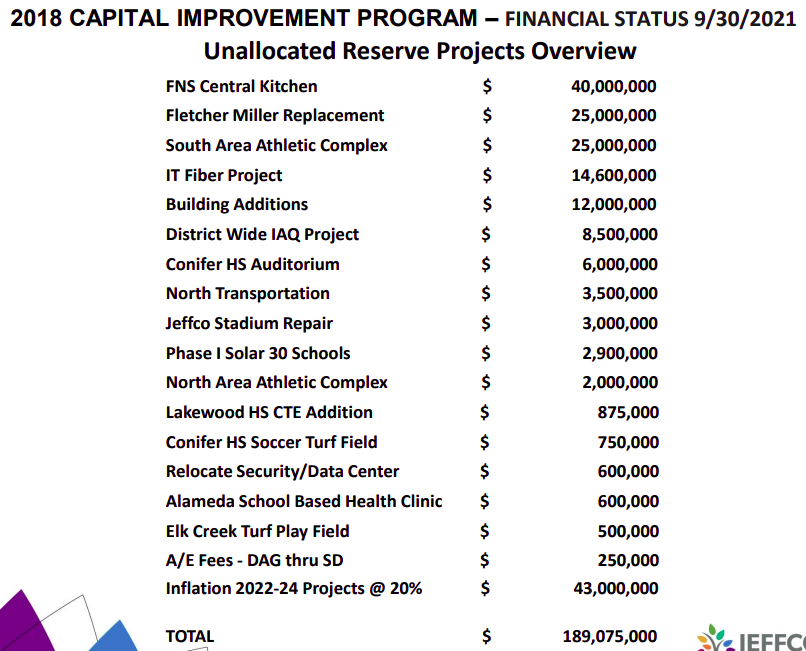

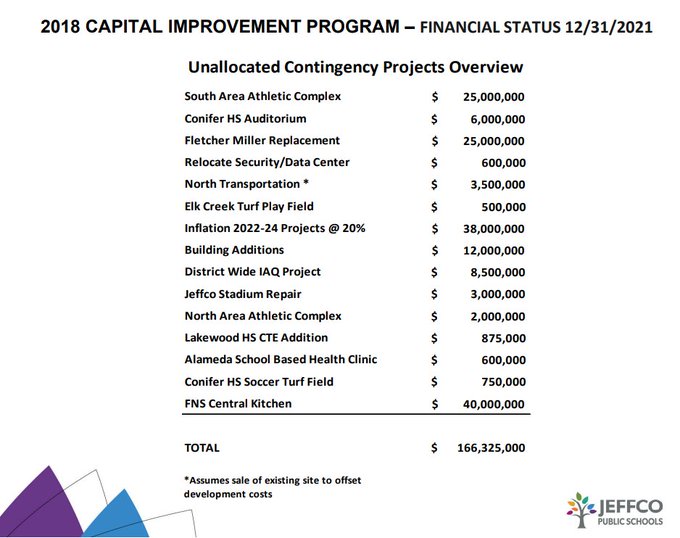

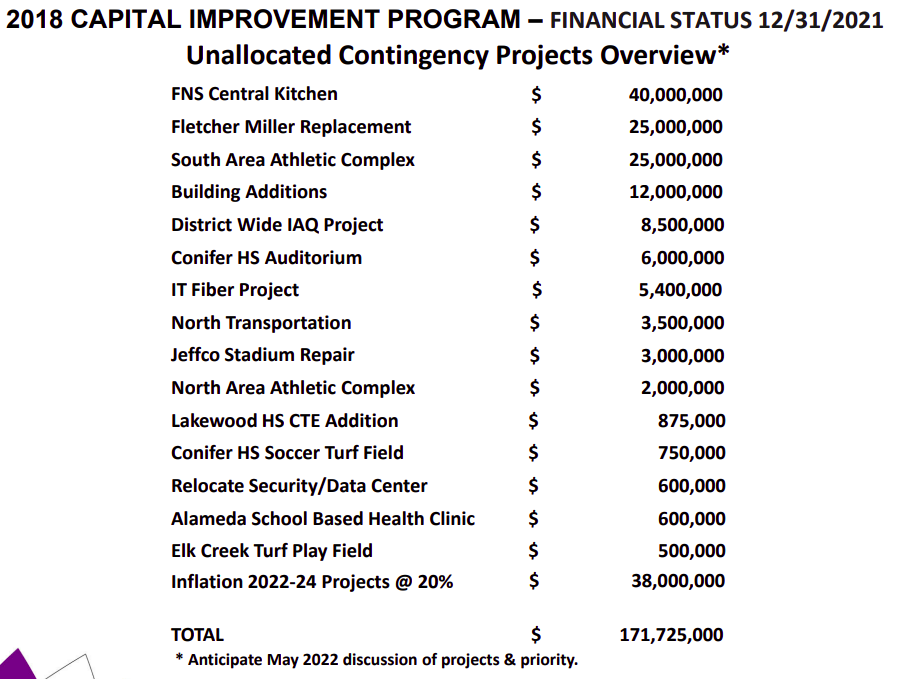

The project next magically appeared in a Reed presentation to the Board as a “possible” use of $14.6M unallocated contingency in October 2021.

But, it didn’t stay there long. By the December 2021 meeting that $14.6M suddenly showed up on the monthly CAAC report with a $0 original budget. That means it wasn’t planned to be in the scope of the Capital Improvement Program, but yet, there it is. Who approved that and why did they approve it?

And, as is usual in Jeffco schools, it only gets worse. In a presentation posted days before a Feb 2022 Board Meeting, the Fiber project was no longer on the list of potential projects for the CIP’s unallocated contingency.

But, it magically reappeared several days later during the actual presentation (revision 1), but with a price tag of $5.4M, while still appearing on the CAAC report for $14.6M. The only reasonable conclusion for this is that the project is either running significantly over budget, or the IT dept can’t totally fund its $14.4M portion of the project.

Something very strange is happening with the Fiber project. The 10+ schools, including Vivian, Mulholm and Lumberg, who will end the program with FCIs over 20% will continue to suffer in facilities with significant needs because the bond program is spending money on projects that were hidden from voters and not going directly into fixing classrooms.

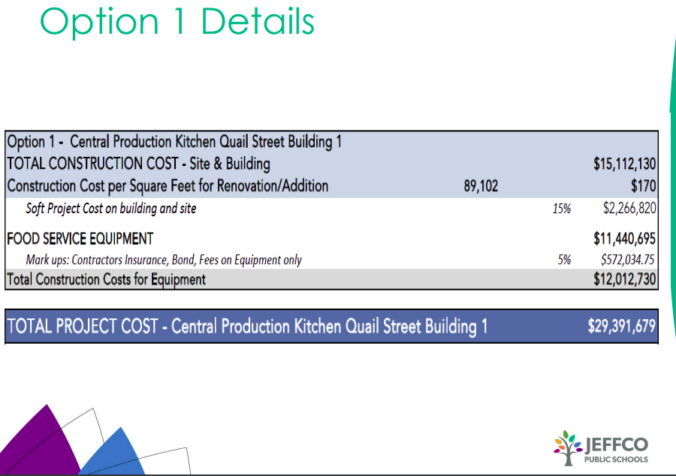

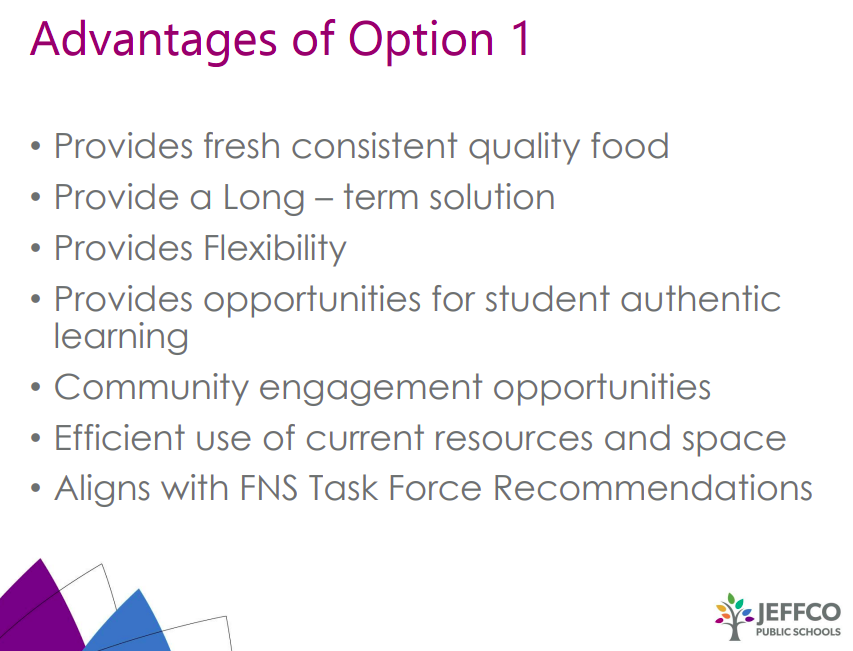

This plan included a recommendation that Jeffco construct a Central Production Kitchen at Quail Street, w/advantages such as providing fresh consistent food quality and alignment with the previous recommendations of the FNS Task Force.

Central Kitchen Advantages

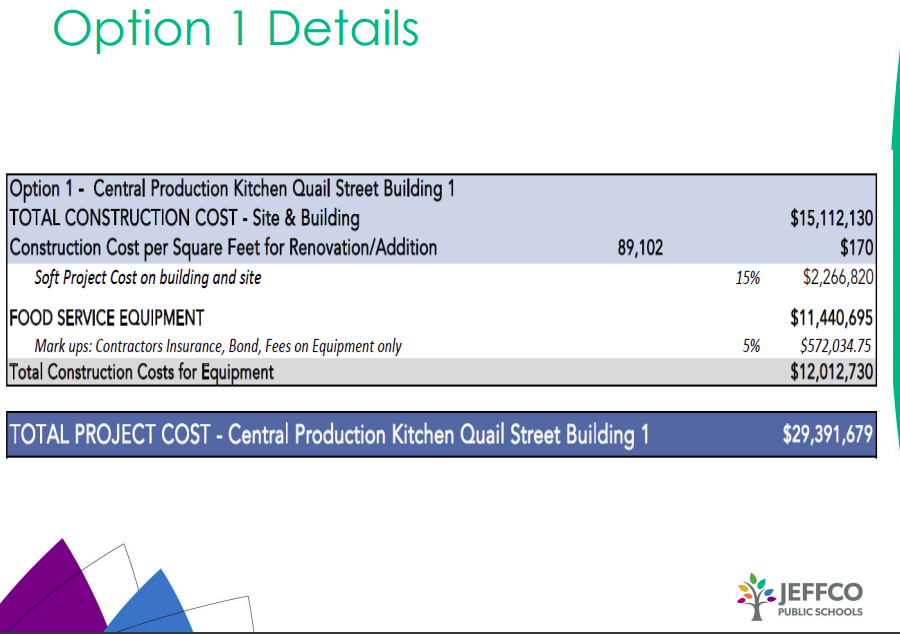

The cost to implement the Central Production Kitchen was $29.4M, including soft costs.

2020 projected Central Kitchen Costs

So what did @JeffcoSchoolsCo do?

Absolutely nothing!

Financial genius Brad Rupert noted that Jeffco didn’t have $30M lying around.

Entrepreneurial wizard Jason Glass noted that Jeffco could use the bottomless pit of Capital Reserve funds or ask voters to approve another bond for the funding.

And District COO Steve Bell, who oversees FNS, just sat there like a lump on a log.

The truth of the matter is that Jeffco DID have money for the project and for some reason either incomprehensibly didn’t realize it, or didn’t want to use it.

In December 2018, Jeffco received $50M in premium from the bond’s first issuance, with another $30M expected from the 2nd issuance. If Jeffco set aside $25M of that for a Fletcher Miller replacement school, which was removed from the bond program, that would leave $25M, almost the $29.4M needed.

Yet, the bond program included kitchen renovations for 41 schools and the construction of 5 new schools. It is not hard to imagine $4.4M in cost savings if a Central Production Facility was created, reducing planned construction and renovation costs.

But the Board didn’t take action and leadership, including Glass, Schuh, Dorland and Bell, did nothing to advance the project while estimated costs have now climbed $10.6M to $40M.

How does that even happen over the course of under 2 years? That’s an increase of 37%.

October 2021 Central Kitchen Costs

Let’s be perfectly clear. This is now a $15M mistake. Money that could have been used in classrooms.

$25M in overages were spent on fields while a plan for a central kitchen which would supply fresh food to kids was just forgotten and now, based on current program overages, it is doubtful Jeffco will have the money to complete.

More than 3 years after Jeffco received the first $50M in what eventually became $118M in bond premium there has never been a discussion on how to prioritize or utilize that money, and now it is nearly gone, for unexplainable reasons. That is shameful and fiscal malfeasance by everyone involved.

This is just one of the numerous examples of mismanagement and incompetence related to Jeffco’s bond program. Jeffco should never be trusted to be good stewards of bond money ever again.

Contractor Procurement in Jeffco's CIP. Not awarded to low bidders.

On November 10, 2020 the consulting firm of Moss Adams presented their findings from a mid-program assessment of Jeffco’s Capital Improvement Program. The report was not good.

Included in the report were areas that should raise serious concerns among the Superintendent, Board Members, District Staff and Jeffco taxpayers.

One of the areas that Moss Adams looked at was Contractor Procurement, essentially how contractors were chosen.

Moss Adams wrote:

… however, bid tabulations or evaluations for the selection and award of the projects were notavailable. Additionally, documentation was not available to demonstrate the selection process and awarding of professional services from the prequalified list of consultants. We were unable to determine whether or how the selection and award process for District projects included the factors outlined in the District’s policies and procedures.

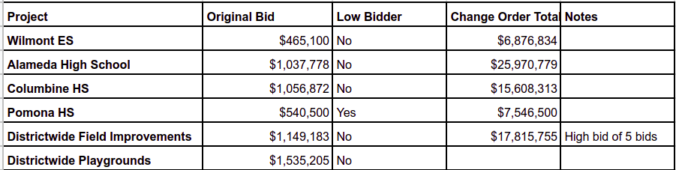

Essentially, Moss Adams is saying that there is no record of how winning bidders were chosen. Think about that for a minute. Of the 6 projects Moss Adams looked at from a Contractor Procurement perspective (Appendix H), only one was awarded to the low bidder and that there is zero documentation on why low bidders for the other 5 projects weren’t chosen. In addition, 5 of the bidders who were selected were subsequently issued change orders, the minimum value of which was over $6.5M.

Contractor Procurement in Jeffco’s CIP. Not awarded to low bidders.

This is just beyond belief. It is certainly not hard to imagine scenarios where a procedureless system like this can, and maybe has been abused.

Something similar happened with regards to Architect Procurement.

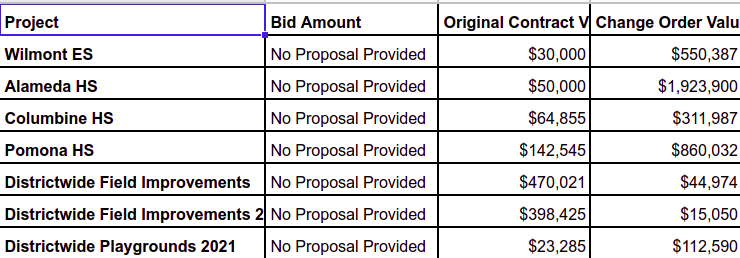

Moss Adams looked at 8 projects with respect to Architect Procurement (Appendix I). None of the 8 provided a proposal, with Moss Adams stating that these contracts appeared to be “sole source procurement”. How can anyone think that there is not the opportunity for fraud, favoritism or over pricing with so many sole source contracts? And, not to be outdone by the Contractor Procurement, all of these architecture firms were issued substantial change orders too.

Architect Procurement in Jeffco Schools CIP. Sole Source awards with no proposals and change orders.

This is not the way to run a capital program. The optics are that there is way too much opportunity for fraud and corruption.

These examples are only the tip of the iceberg if you take the time to critically read the full Moss Adams report, not just the cherry picked and sanitized sound bites District staff presented to the Board.

The program is out of control, not just from a cost perspective, but also from management and fraud mitigating perspectives.

Jeffco taxpayers and voters deserve nothing less than full Financial and Performance audits. Taxpayers were promised that Jeffco would be good stewards of their money. That isn’t happening.