Three weeks ago, Jeffco Board of Education director Kenworthy went on a rant regarding trust and transparency within the District and the past. Once again, she was wrong. Take a look for yourself.

Below is the letter I sent to the Board in response to Kenworthy and her delusional outlook.

Good morning,

While I don’t know exactly who or what Kenworthy was talking about during her Monday night monologue at the end of the Partnership presentation (possibly JCEA among others), I do want to emphasize that the past IS extremely important when trust and transparency are concerned. She mentioned that she has been on the Board for 2 years, but the reality is that the Jeffco School Board — even though it was comprised of different members — has made promises to taxpayers in the past that DO still make a difference to voters today. I’m going to focus this email on the bond, because I am familiar with that. For example, in 2018, the District made several very explicit promises to convince Jeffco voters to approve the previous MLO and Bond. It is no conspiracy theory to state that the district failed to fulfill those promises. If taxpayers can’t trust the District to use the funds as promised in the past and nothing has changed, then there is no reason to trust that the District will use any new funds in the promised manner either.

Applegate can shed all of the tears she wants, but maybe the Board should have been thinking a little earlier about restoring trust through actions when issues were previously raised rather than completely ignoring taxpayer (and union?) concerns. Now, while Kenworthy may not have been specifically talking about bond issues that have been raised, she has certainly avoided hard conversations about the program and once again is flippantly and derogatorily dismissing dissenting views to hers as “conspiracy” theories. So, my answer, and my family’s answer is a resounding NO! In 2018 it was 4 votes for both the MLO and Bond, this time around it will be at least 2 NO votes and 2 non-votes (due to moving away), a swing of 6 votes AGAINST for those keeping track at home. If you are familiar with the 2018 bond, you know how close that vote was. Not only that, I will personally continue to write and inform people about the failed promises, lies and squandering of money surrounding the 2018 CIP. Because, as I just explained, IT MATTERS TODAY.

Here is why I think everyone should oppose the measures. I have made these points in the past and you have just ignored them. I hope that in what may be a new atmosphere of openness to listening to dissenting voices and learning from the past, you will read these points and take them to heart going forward:

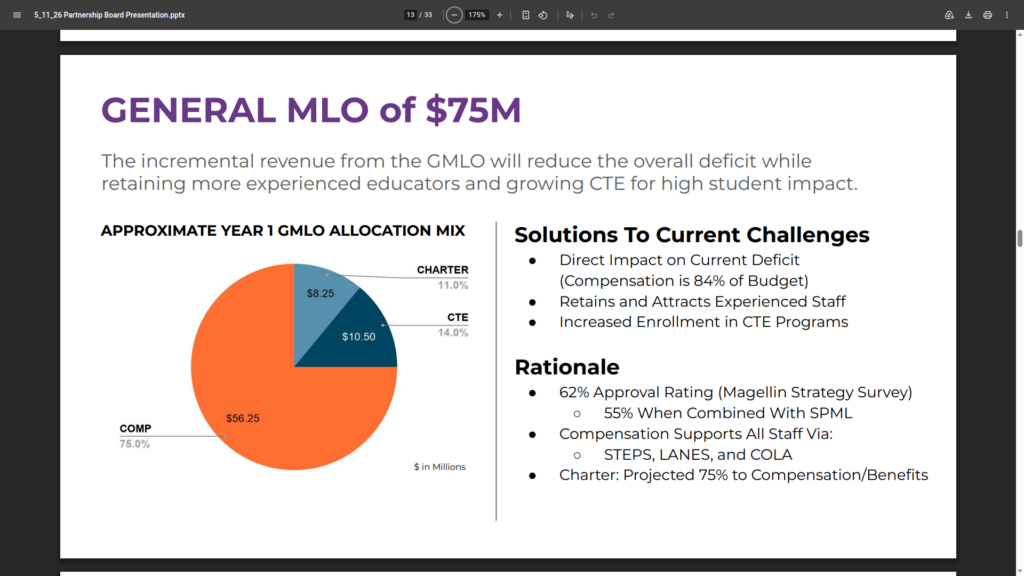

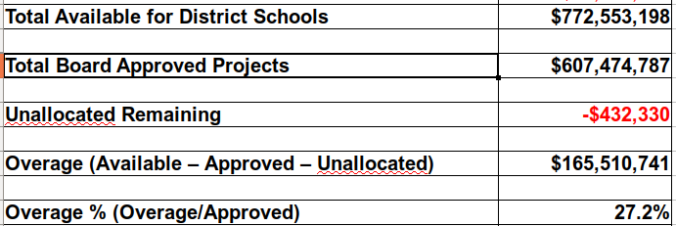

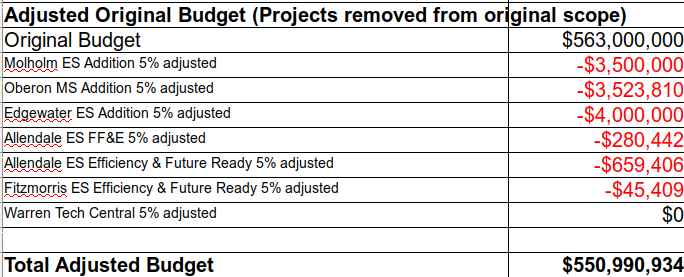

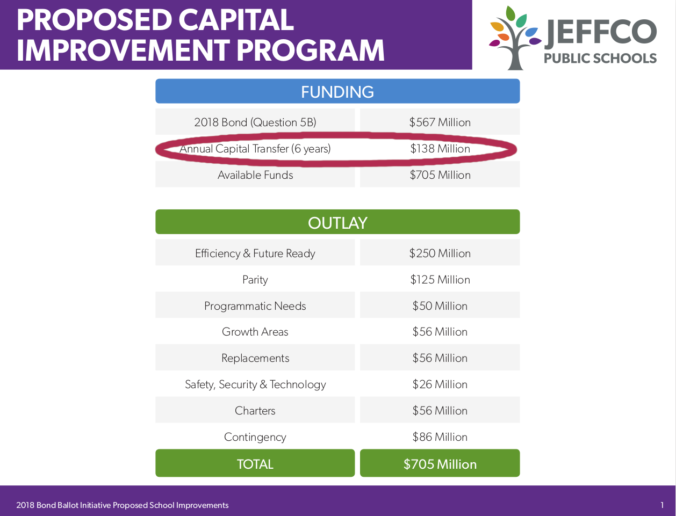

1. The District broke its promises relating to the bond, just like the MLO. Promised audits were not performed. A senior staff member of the District, in fact the Executive Director of the bond program, was paid with bond funds. The CAAC provided so little oversight that $118M in bond premium essentially disappeared and the program ran $150M over original cost estimates with no explanation.

2. The District failed to implement with fidelity the recommendations of the November 2021 Moss Adams report, including performing best practice yearly Performance Audits. Dorland publicly promised a 30-60-90 day plan to implement the recommendations, but it was never made public and the recommendations were never fully implemented. After that, I never trusted a thing that Dorland said or promised, and I never will. To make matters worse, the CAAC, supposedly responsible for CIP oversight, never ensured these simple recommendations were implemented either. Because of that, I will never, ever trust a citizen’s committee again.

3. Where did $118M in bond premium go, and why were the final costs at schools more than $150M over initial estimates? If someone can’t easily answer those questions and point to processes that have been incorporated to prevent it from happening in the future, the same thing will happen again and more money will be squandered. It would be stupid for taxpayers to give Jeffco even more money to waste.

4. The lies, the cover-up and the gaslighting. Kenworthy wants everyone to think that financial information is all just readily available. The facts are that I have had to submit more than 100 CORAs to obtain information relating to bond program information. That includes several recent ones, during her tenure, relating to final CIP costs at schools, something Moss Adams highlighted in their report. I have identified, and documented, multiple lies by the district and district staff relating to the program. These include project costs of closing schools presented to the Board and the still inaccurate original school budget costs shown on the Interactive Map on Jeffco Builds. That itself is an attempted cover-up of $30M in cost overruns. Regarding gaslighting, just ask Kenworthy and Applegate how many times they have responded or engaged with me regarding my well documented concerns. As far as the other 3 of you, it has been nothing but radio silence from Gibbens and Moeinian, making me wonder how truly interested they are in cleaning things up in the district.

The past matters when it comes to trust and transparency. As far as I’m concerned, it is going to take a lot for Jeffco to show me that things have changed and the District deserves any more of my money. I suspect a lot of other community members feel the same way. It’s time to step up and take actions to restore the trust that has been lost and show the community that things are changing, not just sit up there on the dais and act like you are somehow entitled to it.

P.S. I am prepared to fully support any numbers, analyses and conclusions I have previously sent to either the CAAC or Board with numbers and information that was publicly made available to me