Jeffco’s Capital Improvement Program is running $165M over original cost estimates. In 2018, Jeffco told voters that their Capital Improvement Program would provide $563M in upgrades to district facilities and provide an additional $56M to Charters to upgrade their facilities. Jeffco also received additional revenue of $118M in bond premium and over $16M in earned interest giving the program a current total of $836M to work. Over the course of the program the Board approved $56.5M in new projects and $12M of original projects were dropped leaving $44.5M in net new projects. All of this means that Jeffco burnt through their $86M in program contingency and the district’s $122M share of premium and interest with only $44.5M in new projects to show for it.

What happened to that $165M? Certainly some of it was caused by inflation, but the fact of the matter is that Jeffco apparently didn’t plan for ANY inflation. That is malpractice. However, even projects at the beginning ran over budget, so inflation isn’t anywhere near the real reason for the overages. Certainly, there was added scope, but since the Board didn’t approve that added scope who did, and what was the process for those additions? Unfortunately, no one knows. That is not a good thing. Shouldn’t there have been a Board and community discussion on how to prioritize the use of the bond premium and interest instead of it just disappearing in some black hole? Best practice says that should have happened, but in Jeffco the money just disappeared and no one can explain where it went on who approved it. All of that is shady and plain wrong in my book. Unfortunately, neither the CAAC nor the Board seem to care. That means that neither of those two groups should be trusted when they want to make promises when asking for the next bond.

Here is my calculation in obtaining the $165M in overages number. $165M is just ridiculous, not just in the shear number, but also in the percentage of the entire program.

In order to calculate district overages associated with the CIP, I started with the program’s current revenue and removed costs associated with Charters. I then took the program’s initial estimated cost which was $563M and adjusted it by adding Board approved additions to the program and removing projects that were canceled. For projects that were canceled, I adjusted the amount by the 5% that was added to all project costs at the beginning of the program. For ROTS I, I used the Net addition amount of $12M that was initially told to the Board during the approval process. Detail is listed below.

Here are the steps:

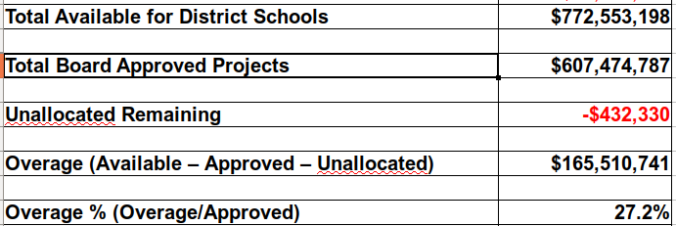

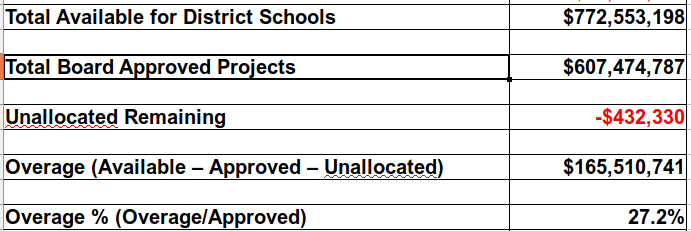

1. Start with the current projected program revenue, $836M.

2. Remove the amount allocated to Charters, $64M.

3. This will leave the funds available for district projects, $772M.

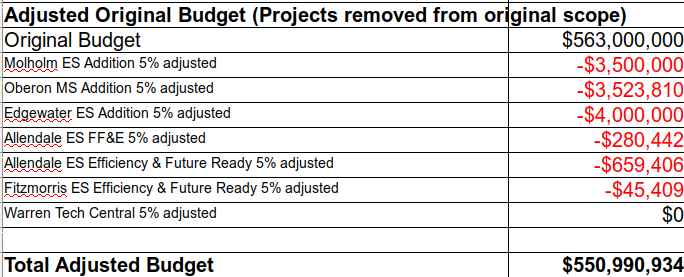

4. Determine the program’s current adjusted budget

a. Reduce the original $563M program budget by projects that were canceled (not including closed schools that were part of ROTS I and II). Adjust for 5% cost increases that were added after the program was started.

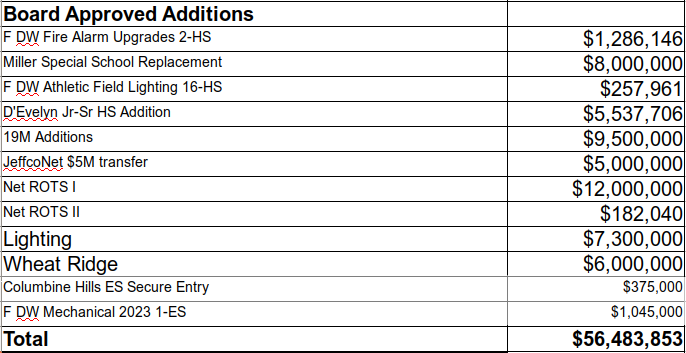

b. Add back in the original estimates for projects that the Board approved. For ROTS, this is the net increase for the affected schools. For example, that would be $12M for ROTS I.

5. Subtract adjusted program budget from district funds available to get an Overage amount, $165M, since there are no funds remaining.

6. Adjust Overage amount by Unallocated remaining. Since there is currently a deficit in Unallocated remaining, that increases the Overage. This total is $165.5M.

7. Divide Overage by Adjusted Budget to get Overage percentage, or 27.2%.

Note: Non-Board approved additions totaling $23,048,093 are categorized as Overages.