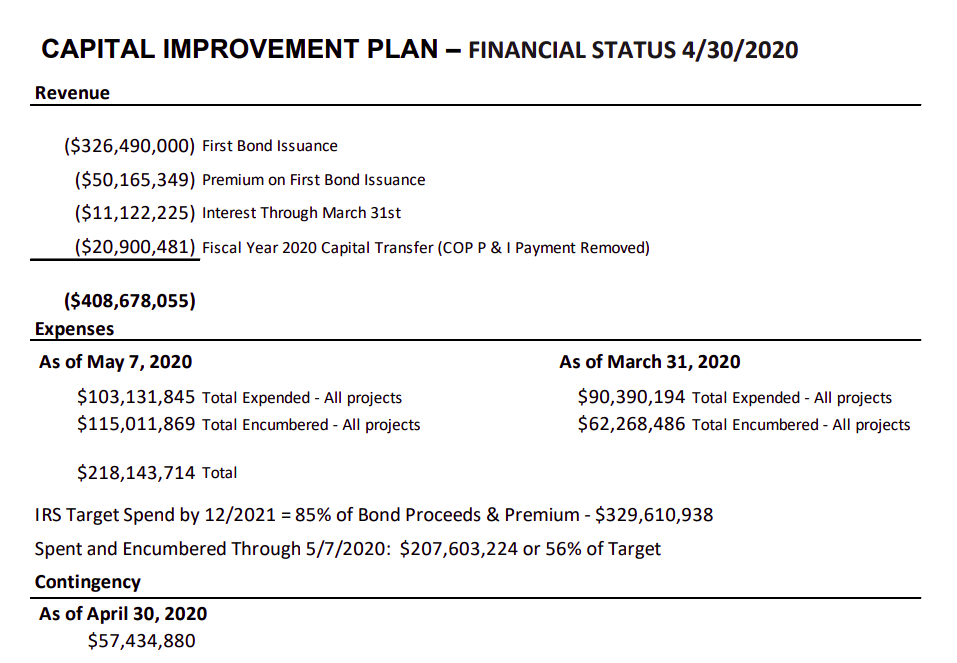

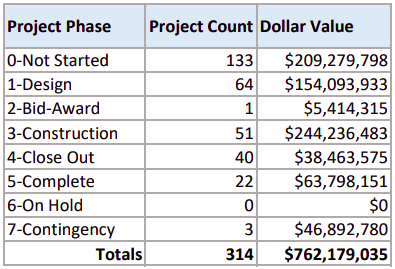

1. $57M over budget. On its own, a program that is $57M over budget less than 2 years into a 6 year plan should automatically trigger a Performance Audit. Just to recap, voters were told the Capital Improvement Program would cost $705M. At the CAAC’s last meeting in November, it had a $762,179,035 price tag.

2. Projected $32M Contingency Shortfall. At the October 7th Board Study Session, Tim Reed told the Board that $68M in contingency had been used to date.

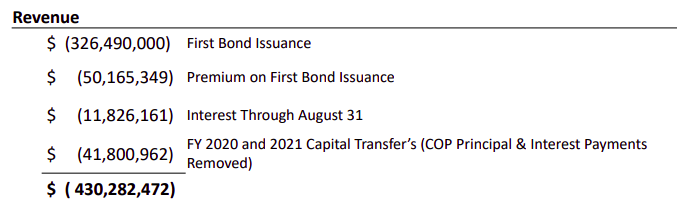

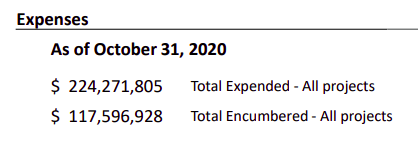

At the CAAC’s November meeting Tim presented the following numbers for funds Expended and Encumbered, totaling $341M.

Subtracting the $68M of contingency from this value means that $273M of the $595M in total program costs are currently Expended or Encumbered, leaving $322M in remaining projects. If that same rate of contingency usage continues, that would require remaining contingency of over $79M. Yet, there is only $47M in contingency remaining, a $32M shortfall.

| Expended as of Oct 31, 2020 | $224,271,805 |

| Encumbered as of Oct 31, 2020 | +$117,596,928 |

| Total Expended & Encumbered | =$341,868,733 |

|

|

|

| Less Contingency Used to date | -$ 68,000,000 |

| Project Work Encumbered or Expended | =$273,868,733 |

|

|

|

| Contingency usage rate ($68M/$273M) | 24.83% |

|

|

|

| Remaining Project Work ($595M – $273M) | $321,113,267 |

| Projected Contingency Required ($321,113,267 * .2483) | $ 79,736,893 |

| Less Contingency Remaining as of Oct 31, 2020 | -$ 46,892,780 |

| Projected Contingency Shortfall | $ 32,844,113 |

|

|

|

| Total Projected Contingency Usage ($68M + $80M) | $147,736,893 |

Do the math. The numbers don’t lie. This is not a healthy Program.

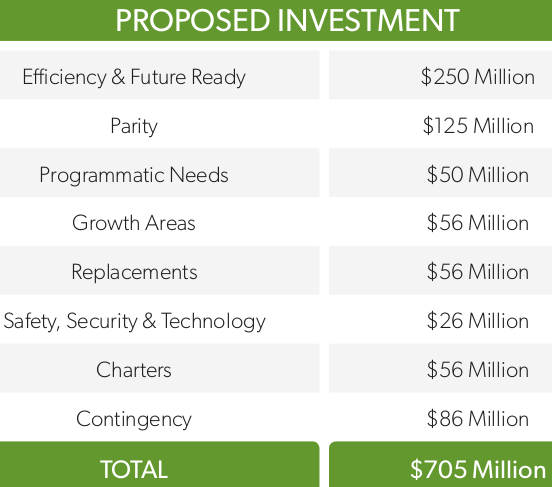

3. Deceptively adding $31M to Flipbook costs. District project costs were presented to voters as $563M. You can arrive at that number by subtracting the Charters $56M and the Contingency $86M from the Flipbook presentation.

This can be verified by adding the costs of individual projects in the original Flipbook (Plus approx. $17M in costs for Trailblazer, North Transportation Hub, OELS and Preschools projects which were withheld from voters).

However, sometime after the Bond passed, the District changed the Flipbook. The cost of nearly every project increased. Here are some examples:

Alameda HS – an increase of $1,430,902 to $19,434,000

Green Mountain HS – an increase of $754,078 to $14,361,000

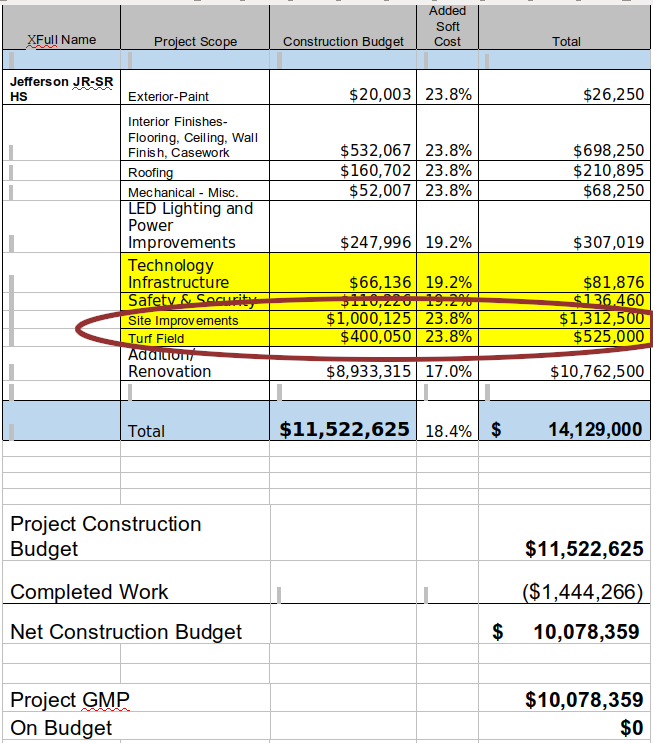

Jefferson Jr/Sr HS – an increase of $672,810 to $14,129,000

This had the net effect of raising BASE costs by a total of $31,967,419. Essentially hiding $31M of cost increases.

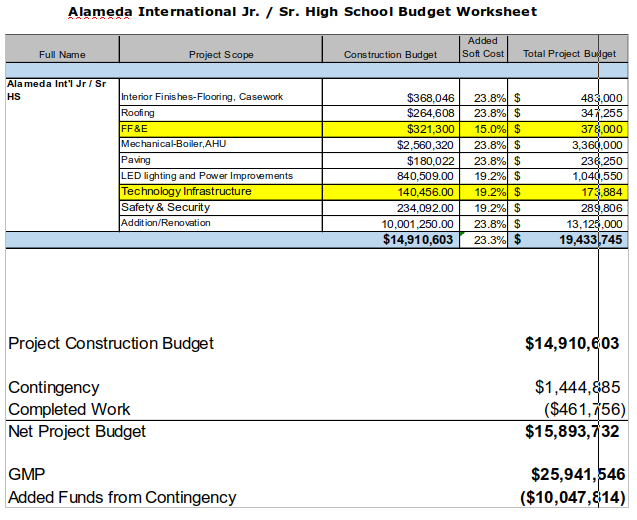

For example, when the construction budget for Alameda was presented to the Board, contingency usage of $10,047,814 was based on the updated Base cost of $19,433,745, instead of the original cost estimate of $18,033,098. This usage of the revised cost estimate deceptively hid the totality of the increase, and the additional use of Contingency, of $1,430,902.

Therefore, cost estimates for all projects have now increased by $100M; the $68M in Contingency that Tim Reed freely told the Board PLUS the $31M in hidden cost estimate increases.

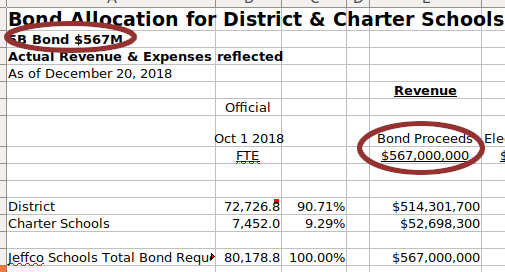

4. Failure to Share Bond Premium with Charter Schools. As recently as of the end of October, the District still had not shared Bond Premium with Charter schools, in violation of the Board’s October 2018 Sharing Resolution. The District spreadsheet widely circulated to Charter Schools show that the District only calculated sharing revenue based on the Bond par of $567M.

Yet, at the November 11th Board Study Session, Steve Bell told the Board that Bond Premium is shared with Charters.

Therefore, at this point, Charters are owed approximately $4.6M, PLUS interest – which will subsequently reduce the Contingency available for District projects by a corresponding amount.

Brian Ballard, Chair of the District’s Financial Oversight Committee, has said that it is the CAAC that has responsibility for overseeing 5B Bond funds. If that is the case, why hasn’t the CAAC ensured that District Charters have been given their complete share of the funds?

5. Out of Scope Projects. There are multiple projects that can be identified that were not in the scope presented to voters. Several easily identifiable, high-cost projects include: Ralston Valley HS Roof, Lakewood HS Track, West Jefferson MS Track, etc. The following images were taken from the Original Flipbook presented to voters and clearly do not show these projects.

Was there any discussion relating to the addition of scope and reduction of contingency for these and other added scope projects? What was involved with this process? Were these prioritized over replacement schools? Was there a vote?

6. Deceptively Hiding the True Cost of Alameda HS Cost Overruns. Similar to Jefferson Jr/Sr HS, Alameda HS is slated for Track and Field Upgrades. When the Jefferson project was submitted to the Board for approval, the Track and Field upgrades were included in the project costs and subtracted from the remaining budget.

This was not the case when Alameda was presented to the Board. The cost for the Track and Field upgrades were left off of the presented costs, effectively deceiving the Board that total overages are at least $1.5M over what was shown. Was that intentional deception, or merely incompetence?

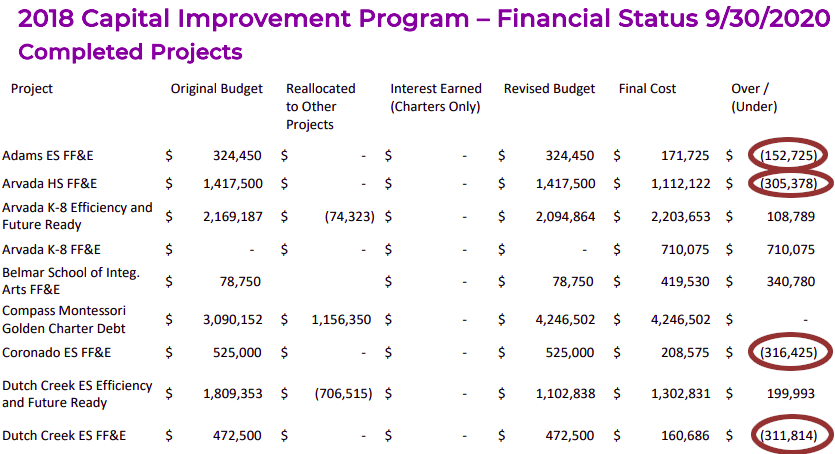

7. Recent Large Underspend on FF&E Projects. We all like to get good deals. However, the cost savings on several recent FF&E projects go beyond the definition of good deals, suspiciously into the realm of scope reductions. Look at some of the “savings” generated from some of these FF&E projects that were recently presented to the Board, $150k, $300k, $315k and $310k.

These “savings” are 47%, 22%, 60% and 66% less than the original cost estimates. That’s far more than a reasonable person would expect from a “good” deal. What happened here? Was scope cut at these schools?

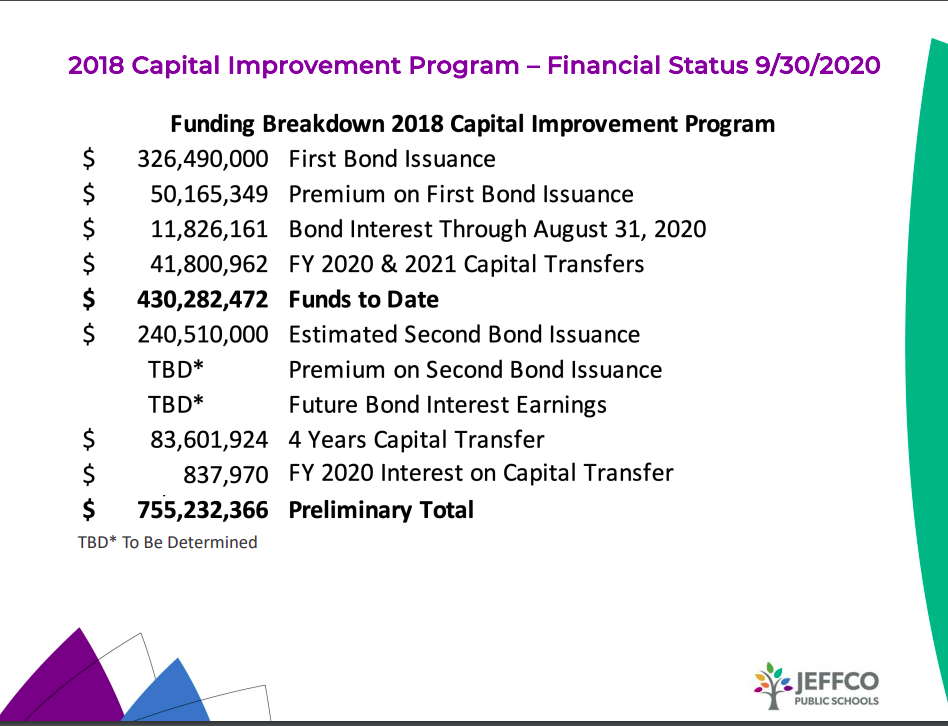

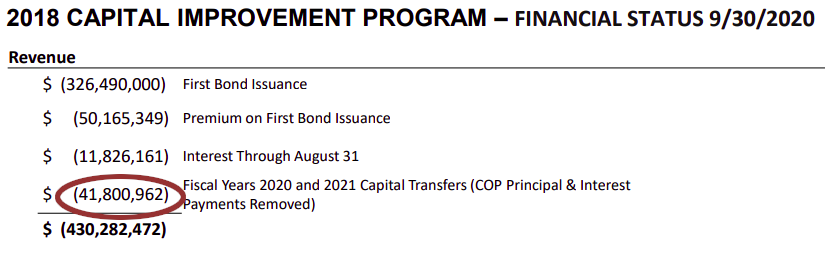

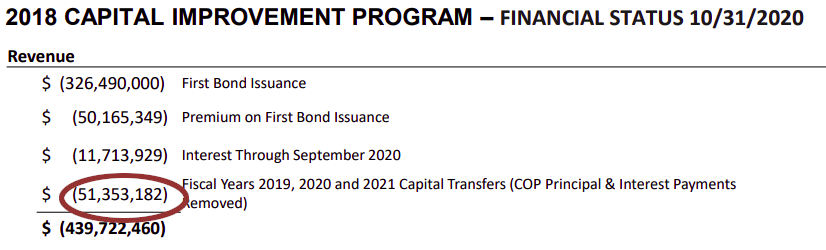

8. Unexplained Recent Increase to Capital Transfer Revenue. At the October CAAC meeting, members were shown Capital Transfers into the Capital Improvement Program of $41.8M. Yet, in November, they were shown $51.3M. Where did that additional $9.5M come from?

(On a side note, how does Interest Revenue DECREASE by $110,000 from August to September? Can you trust any numbers that are presented?)

Approximately $3M appears to come from the movement of the contingency in prior capital improvement programs such as 18M and 19M. This contingency decrease can be seen in documents presented to the CAAC.

But, the source of the remaining $6.5M is unexplained as the value of the 18M, 19M, 20M programs remain the same. And this happened mere days after Steve Bell told the Board that the capital transfers would be $20M/year over 6 years for a $120M total.

9. Questionable Use of $50M in Bond Premium for Contingency. Recently, Tim Reed and Steve Bell told the Board that during initial 5B discussions the bond ask amount was decreased and 2 replacement schools were removed from the list of projects.

If this was the case, why then, when the District received $50M in bond premium, weren’t replacement schools immediately added to the list of projects? Instead, it appears that the $50M in bond premium has merely been added to the $86M already allocated to program contingency. What was the process in determining that the additional $50M in contingency should be used for contingency instead of being used for replacement schools, particularly when taxpayers voters were told that Jeffco had $1.3B in deferred maintenance needs?

10. Failure of CAAC Members to Maintain Independence. Tim Reed recently sent members of the CAAC a document relating to the Purpose and Membership of the committee. This document clearly states that members must be:

Independent and free from any relationship that would interfere with independent judgment

Gordon Callahan, a CAAC member, has a relationship with the District. His firm has been the recipient of nearly $1M in contracts over the past year and a half.

This is not the appearance of independent judgment.

For taxpayers to fully trust the Capital Asset Advisory Committee ALL members of the committee must be completely independent and free of District relationships. Unfortunately, that is not currently the case. His continued membership on the committee is ethically questionable and erodes taxpayer trust.