Here are the 10 things we learned from the October 7, 2020 Jeffco Board Study Session on the District’s Capital Improvement Program.

None of these things is good!

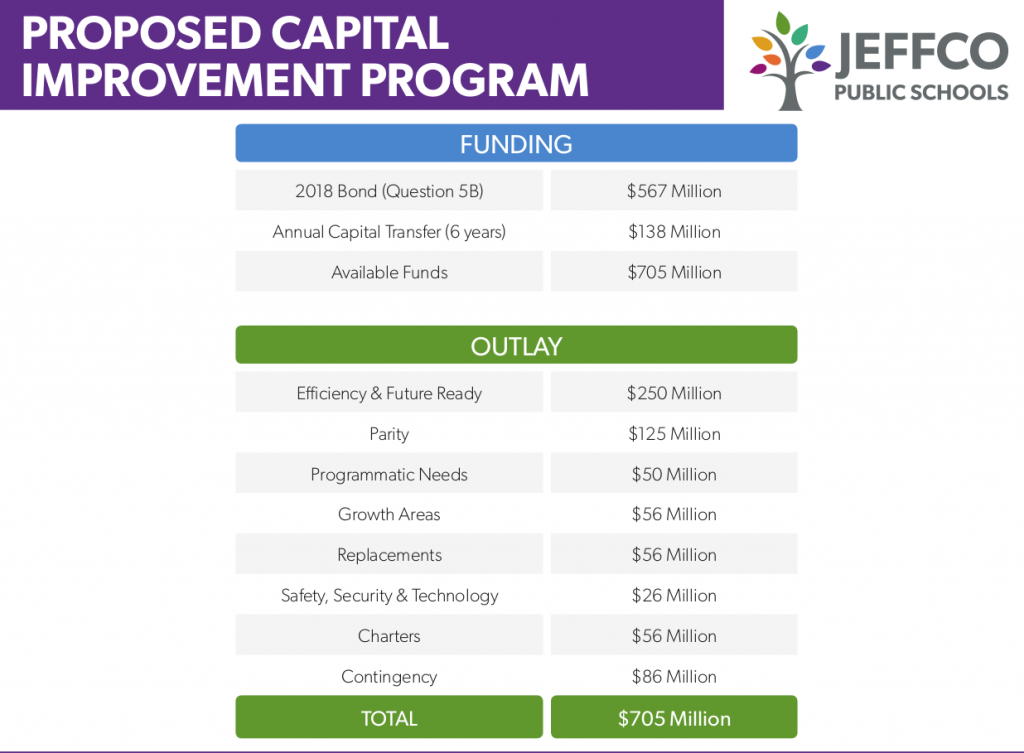

1. HS Parity – We were told during the Wednesday meeting that one of the goals of the bond program was to achieve High School building parity. Someone might want to tell the staff, parents and students at Pomona, Wheat Ridge, Arvada and Green Mountain that. Even after the program finishes, these schools will still have Facility Condition Indexes above 15% while schools such as Bear Creek, Golden, Arvada West and Lakewood will have FCIs below 4%. That’s not parity/equity in my mind. Once again, Jeffco talks equity, but never, ever delivers.

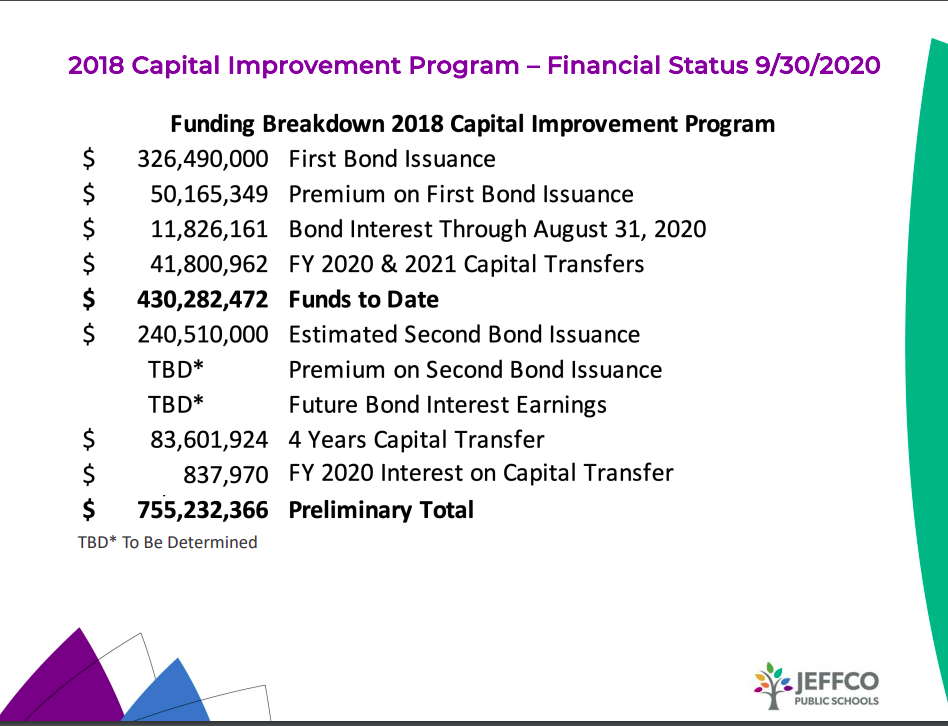

2. Capital Transfer – We learned that in 2 years Jeffco has transferred $41.8M from general funds to the Capital Program and that over the next 3 years another $83.6M will be transferred for a total of $125.4M.

But, Steve Bell made that sound worse by stating that only $120M in total would be transferred over 6 years.

Jeffco voters were promised $23M/year would be transferred for a total 6 year transfer of $138M.

This is now an expected shortfall of $12.6M. This shortfall will need to be made up by either allocating contingency or reducing project scope. I don’t even think that the Board is aware of this shortfall at this point. Bell and Reed will use Wednesday’s presentation to say that they informed the Board, but this is a pretty weak argument. In reality, it was the CFO’s job to ensure that 2019-20 and 2020-21 budgets presented to the Board of Education included transfers of this promised money, OR, to inform the Board of Education of this shortfall. The former CFO Kathleen Askelson failed to do either. She failed in her fiduciary responsibilities to both taxpayers and the Board. It’s no wonder she suddenly decided to leave Jeffco. Once this came to light she should have been fired.

3. 19M Projects – During the meeting Reed casually mentioned that $9.5M worth of projects were transferred from the District’s 19M facilities maintenance program to the Bond program because they were ready to go and it would assist in meeting the arbitrage requirements of the bond.

What he failed to say was that these projects were funded straight from the contingency of the Capital Improvement Program and that this was in reality an increase of scope. Complete and utter deception on the part of Reed and Bell.

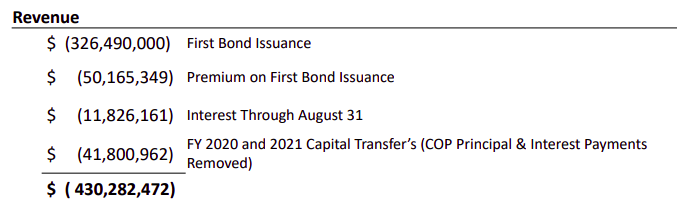

4. Missing $41M – $41M is missing from Bell and Reed’s presentation. Where is that money? Jeffco voters were told that the program came with $86M in contingency built into it (see image above). $50M was added through bond premium and another $12M added through interest.

That’s a total of $148M above and beyond the $563M in project cost estimates presented to voters. Reed and Bell told the Board that they are carrying $107M in program contingency.

In that case, where did $41M go?

$ 86M in contingency presented in original Flipbook

+$ 50M in bond premium

+$ 12M in interest

=$148M total available above cost estimates

– $107M in stated contingency

=$ 41M missing

5. % of contingency usage – Bell told the Board that $68M in contingency has been spent (video above). That contingency was spent during the completion of $264M ($332 expended and encumbered from Board docs – $68M in contingency used) in project work. Since there is (now) $594M in total work that needs to be completed for the program that means 44% of the total program work has been done against 64% of the total contingency ($68M of $107M in total contingency). At the current rate, available contingency will be used before all projects are completed and scope will have to be reduced. Calculated a different way, continuing to use contingency at the current rate would mean that Jeffco needs $153M in total contingency, $46M more than what is currently allocated. This is not a good position to be in.

6. Construction increases – We learned that there are several Board member apologists who want to blame inflation and the length of the program (6 years) for cost overruns. I don’t agree with that. A timeline for project work was clearly laid out in the Flipbook. District staff knew when projects would be worked on and SHOULD have incorporated inflation based increases into their cost estimates. If they didn’t do that, then they are incompetent and should be fired, not given a free pass as Rupert and Mitchell want to do. Besides, Jeffco is only 2 years into the program. Inflation based cost increases shouldn’t be responsible for over $68M in cost increases at this point.

7. Contingency use between May and September – In May Reed told the Board that there was $57M in remaining contingency.

Since that time the Board has approved approx. $11M in contingency usage, mostly at Alameda. Now, Reed is now telling the Board that there is only $37M in contingency remaining. What did that additional $9M in contingency get used for in such a short period of time? Where did it go in only a few short months without Board knowledge?

8. Questions about use of $50M bond premium – The bond premium was a bonus. In my mind, it should be used to provide real value to the taxpayers. During the meeting Reed told the Board that to get the total bond package down to something reasonable for taxpayers for the 2018 vote they had to remove two replacement schools.

Now, when Jeffco received bond premium, why did $50M just get consumed to pay for added contingency? Why weren’t 2 replacement schools added into the program? This is pure mismanagement and an atrocious use of taxpayer money. People should be fired for using $50M this way!

9. Where was the Citizens Capital Asset Advisory Committee? Members of the CAAC were supposed to be at the meeting to answer questions regarding their oversight and monitoring of the program. They are definitely aware (here and here) of the depth and degree of the $100M in cost overruns to date. It is suspicious that at the last moment they decided not to show up.

10. Board President Harmon and Directors Rupert and Mitchell will go to great lengths to cover-up waste and mismanagement and protect the District from criticism or scrutiny. When Director Miller brought up questionable practices regarding the use of the $50M bond premium, instead of addressing that issue first, Harmon attacked Director Miller and then Rupert and Mitchell went into a full on defense of the District. It’s not their money, so why should they care?

This Wednesday’s study session was enlightening, to say the least. It raised, and never answered, numerous questions regarding the management of a $3/4 Billion Capital Improvement Program. The degree of deception on the parts of Reed and Bell is just unbelievable.

The Program is a disaster – way over budget and heading further in that direction. That is not how you get taxpayers to approve your next bond request.

It is clearly evident that, as promised to taxpayers, a full and complete performance audit on the program must be conducted immediately!