Recently, Colorado Community Media, including Jeffco Transcript and Arvada Free Press printed an article by writer Bob Wooley about Jeffco’s Capital Improvement Program.

For

the most part, Wooley did a good job of attempting to explain a

financially complex program. However, there were some comments and

statements made by Jefferson Public Schools’ officials that were

misleading or downright false.

I’ve

outlined several of those areas below:

1.

The article states:

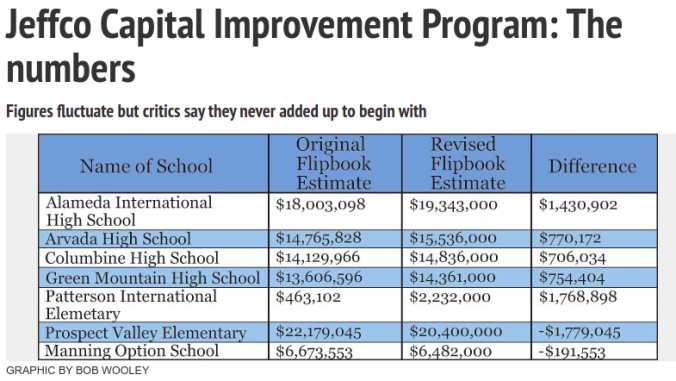

After

the Bond passed, the project’s estimated costs were increased by

nearly $32 million for a revised total of just under $737 million for

the program.

TRUE

– $32M

in hidden

costs were added to the program

After

the bond passed, $32M in costs were added to the flipbook for

the same list of projects.

The

use of $32M in contingency to

cover these costs was

essentially hidden.

2.

The article states:

District

officials say the increase was a result of changes in scope, market

conditions, incorrect estimates or various other factors like

asbestos removal, which were determined once the District was able to

perform more in-depth evaluations of each individual project.

PARTIALLY

TRUE – 81

schools’ cost estimates increased by EXACTLY 5%

While I agree that factors such

as scope changes, market conditions and incorrect estimates can

result in changed estimates, that doesn’t fully explain the extent

of the cost estimate changes between the first and second flipbooks.

The project costs for 81 schools, or nearly 60% of the total,

increased by EXACTLY 5%. This is not indicative of changes in

scope or incorrect estimates. That’s indicative of using Excel to

pad costs.

3.

The article states:

“We

told voters we would accumulate six

years of approximately $20 million

at the back-end to fill up the program,” Reed says.

FALSE

– Voters were told $23M

Voters

were told that exactly

$23M

annually in Capital Transfer would be accumulated. In reality only

$20.9M

annually is currently being transferred. That means

there is a

$12.6M shortfall in

stated revenue, again made up with Contingency.

4.

The article states:

“and

over $3.5 million was spent on hazmat expenses (which technically, do

not count as overages).”

FALSE

– Hazmat

costs ARE overages

-

Why

aren’t $3.5M in hazmat expenses considered overages? Any

decent construction project manager with 50 year old buildings

knows there is asbestos in those

buildings that will have to be mitigated. Mitigation costs should

have been factored into the original estimates.

-

Where

is the money coming from to pay for the hazmat expenses? It’s

coming from the District’s program contingency. Therefore,

technically, and for all intents and purposes, hazmat expenses are

program costs that reduce available contingency This is merely an

attempt by Reed to put lipstick on a pig to make $3.5M in overages

not seem like the $3.5M in overages hazmat costs really are.

5.

The

article states:

In

a document Reed says is now posted to the Capital Asset Advisory

Committee (CAAC) website, all budget variances are listed with

specific overage amounts and the reason for the cost variance.

FALSE

– This

document

lists variances against revised cost estimates, not original

estimates

This

document hides $32M in cost increases. That’s deception.

6.

The article states:

Therefore,

the precise amount of contingency that’s been spent on actual

projects thus far is $65,815,424.

FALSE

– The amount of contingency allocated is currently over $110M

$65M

from what Reed wants people to believe is the contingency spent, plus

$3.5M in hazmat, plus $32M in increased estimates plus $9M from

recent fields project = $110M in contingency allocated.

7.

The article states:

“I’m

not a construction guy,” Bell said. “But we have a construction

guy and I was speaking to him this morning and he said “you know, a

year ago the cost of steel was $53 a ton — today it’s $79.” A

year ago did anybody know it was going to go from $53 to $79? No.”

MISLEADING

– Cost of steel is only one small component of cost increases

Both Tim and Steve have told the Board on several occasions that they have been getting good pricing due to the pandemic. And, this report shows that non-residential construction costs have been relatively flat in Denver for the last 2 years, increasing by only 2.1% total over that time. In addition, there are numerous projects that had no steel involved that are significantly over budget. This is a misleading and deceptive statement.

8.

The

article states:

“According

to Tim Reed, Jeffco’s Executive Director Facilities &

Construction, the amount of contingency that had been spent as of

Feb. 22, was just over $81 million, of which nearly $12 million went

to charter schools…”

MISLEADING

to FALSE – $12M to Charters came from Bond Premium

The

agreement with District Charters was that Jeffco would share

approximately 10% of all bond proceeds with Charter schools. The $12M

Tim Reed is referring to is based on Charters’ share of accrued

interest and bond premium. This has nothing to do with District

contingency.

The

bottom line is that the Capital Improvement Program has already

spent

or allocated $24M over its original $86M contingency budget ($110M

total) only

2.5 years into the program. In addition, Jeffco has hidden

a $12M revenue shortfall from

Capital Transfer.

The

amount

of deception and lack of accountability for large cost increases is

truly unbelievable.