Jeffco’s Flipbook (and here if Jeffco deletes or changes it) is declaring multiple schools are under their bond program budget when they clearly aren’t.

I will document two of the schools here, Fremont ES and Belmar, but there are many more, including Arvada K-8, Columbine Hills, West Jeff MS, Welchester, Eiber and Semper.

Why

is this happening? There are only two answers, either complete

incompetence on the part of staff or a desire to mislead the public

into believing the management of the program is not as bad as it

really is.

Belmar

–

tagged

with a green arrow in the Flipbook

The Flipbook states that Belmar has a budget of $1,068,000.

This

is nearly $250,000 over budget and does not include additional costs

such as security glass, site lighting, IT cameras and network

upgrades.

Fremont

ES

The Flipbook states that Fremont has a budget of $1,289,000.

The

current CAAC report shows Fremont costs as:

Efficiency

& Future Ready

$1,087,700

FF&E

Costs

$334,083

Hazmat

Costs

$102,186

Total

$1,523,969

or

more than $230,000 over budget, not including additional costs such

as security glass, site lighting, IT cameras and network upgrades.

Jeffco

is lying to the public to present a picture that they are good

managers and stewards of our money, when the exact opposite is true.

This is not a good look.

Jeffco should fix this immediately. In addition, Jeffco should show the total costs for each school project so that voters and taxpayers can see the truth.

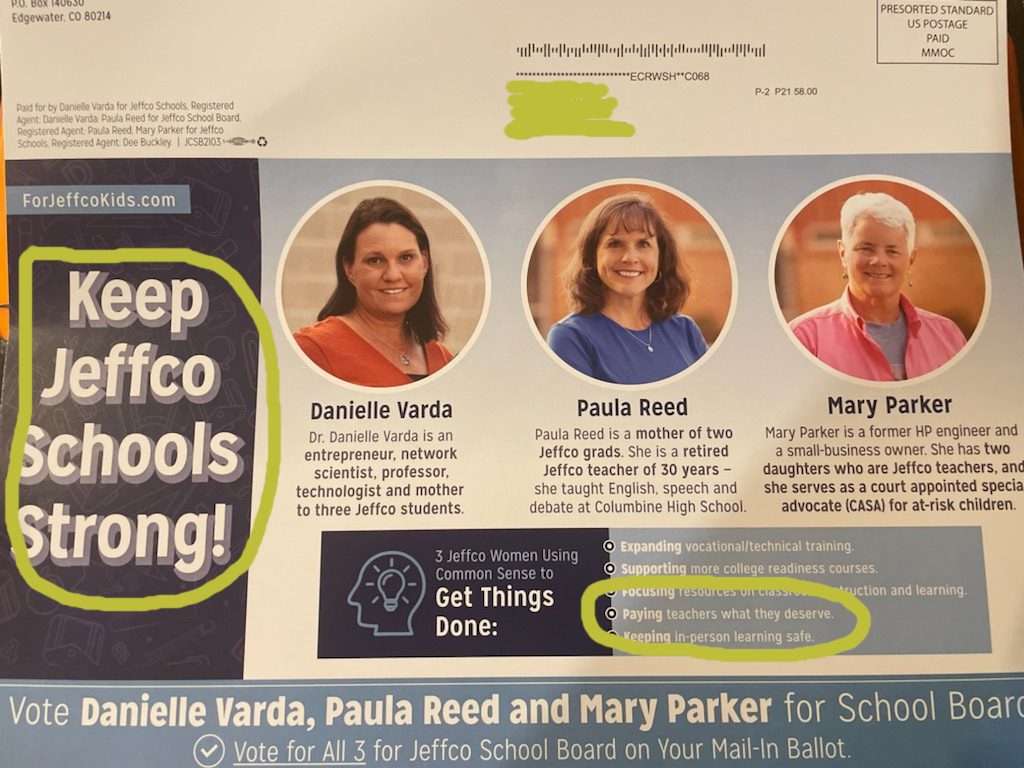

Varda, Reed and Parker are running on a platform of “Paying Teachers What They Deserve”.

Obviously, they want people to believe that teachers are underpaid for what they are doing. But, what does that really mean in an era of declining results in Jeffco Schools?

In any private company I’ve ever been at a salary increase would be looked at very closely when organization objectives weren’t met. In many instances, annual increases would be limited to COLA increases or less, and it would stay that way until objectives were met.

For instance, taking last year’s DUIP, how can anyone justify salary increases when Jeffco wasn’t even close to achieving their goals, that were set during the pandemic?

Yet, Varda, Parker and Reed think that teachers “deserve’ more pay. Their definition of “deserve” is far different than mine. A salary increase above COLA would be hard to justify in my mind.

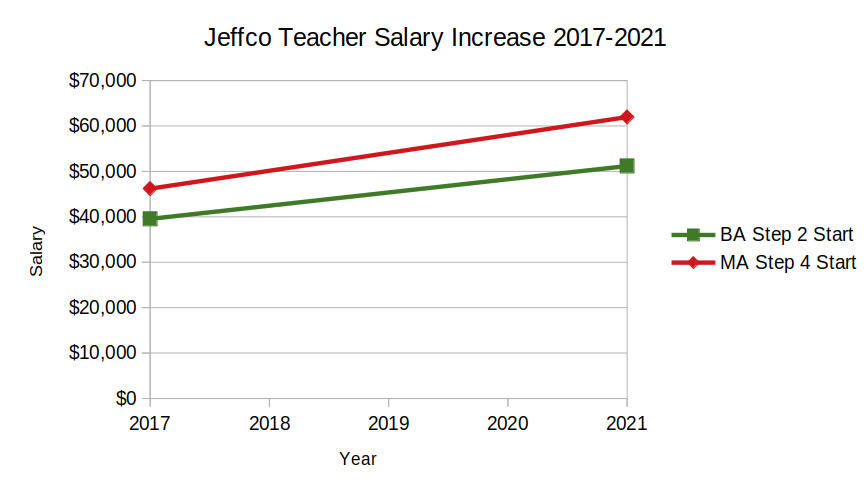

In fact, over the past 4 years teachers’ salaries have increased significantly, far outpacing the 11% Denver inflation rate.

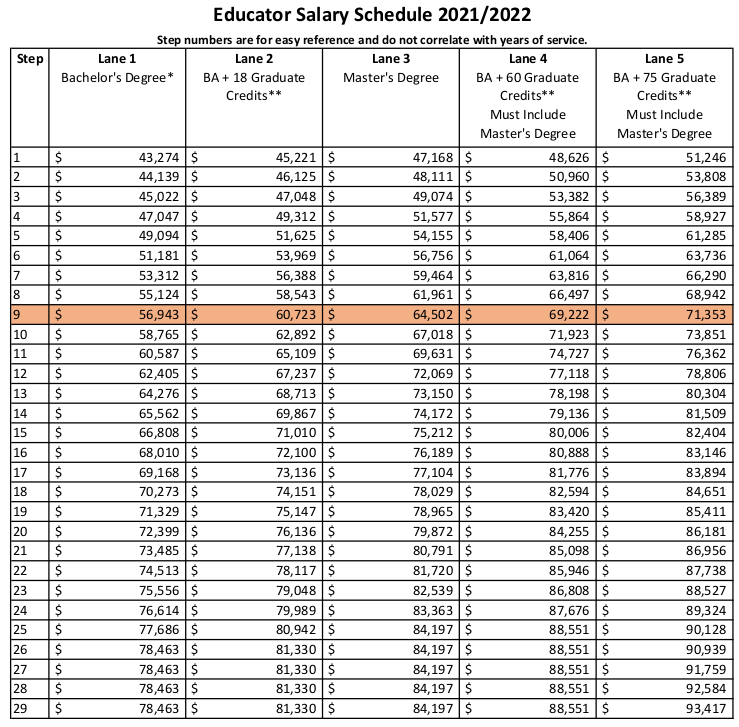

For example, a teacher w/BA @ Step 2 and a teacher w/MA @ Step 4 would have each seen salary increases of approx. 30% including the 4 steps awarded by Jeffco. These teachers now make $51k and $61k respectively, before benefits.

Approximately

40% of Jeffco teachers have salaries over $70k and 20% make over

$80k.

That’s

not bad for:

185 working days

Job Security

Ability to retire w/75% salary @55 & 30 years

In

addition, Jeffco currently pays teachers based on their level of

education along with years of service. Yet, study after study show

that, with only limited exceptions (e.g. math and science), advanced

degrees do not correlate to increased teacher effectiveness.

(https://www.mhec.org/sites/default/files/resources/teacherprep1_20170301_2.pdf)

Therefore, why is Jeffco paying more to teachers with those degrees?

Do those teachers really “deserve” higher salaries? Not in my

mind.

With

year

after year of

declining education results, just how

much do Varda, Parker and Reed think these teachers deserve in

salary? They’re

not saying, but you can be darn sure a salary increase wouldn’t be

the topic of discussion on any corporate Board.

Jeffco schools is not an organization that is showing that it “deserves” salary increases for teachers and admin. It’s time to take a realistic look at total teacher compensation, not just salaries. It’s time to push back on the same old union rhetoric that teachers are underpaid because they aren’t for the results they are delivering.

And

it is absolutely wrong for teacher pay to be one of Varda, Reed and

Parker’s top priorities when Jeffco’s education results are so

atrocious.

They

aren’t a good fit for what Jeffco’s kids need now.

In 2017-18 the

Educational Research & Design department of Jeffco Schools, led

by Chief Academic Officer Matt Flores had a $23M budget. By 2021-22

that budget increased nearly 40%, $9M, to $32M.

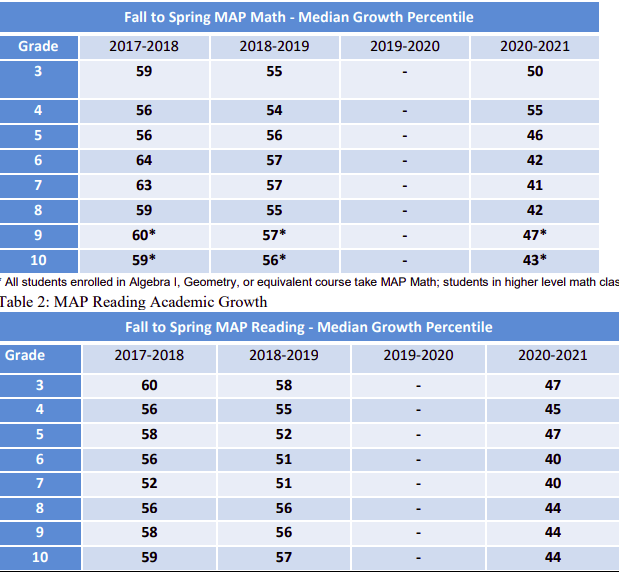

Yet during that same time period both growth and achievement fell dramatically in Jeffco Schools.

It’s obvious that

more money and continuing to keep Matt Flores as CAO are not the

solutions to what is now a very real and urgent problem. Flores is

responsible for these atrocious results and it is evident he doesn’t

have the skills to reverse the slide that has permanently harmed

10,000s of kids.

Dorland needs to

fire Flores immediately. He is providing no useful value to Jeffco.

The fact that after 6 months she hasn’t already done this is a

yellow flag on whether she has the ability to recognize the rot in

Jeffco and the fortitude to do what is necessary.

Dorland and the

Board next need to scrutinize EVERY single penny in the $32M ER&D

budget. Clearly, that money is not being spent on programs that are

improving achievement and growth. It’s time to find programs that

work and spend taxpayers money in a manner that will truly improve

the schools.

It’s time for the

old, status quo, way of doing things to end. It is plainly obvious

that the same people are incapable of effecting positive change. It

is time for drastic and decisive decisions and actions to keep Jeffco

schools from spiraling from its current state of mediocrity into the

terrible category and to keep even more kids from being permanently

harmed.

Taxpayers and

students deserve Board members who will ask tough questions and hold

Dorland accountable for big improvements, people like

Jeff Wilhite

Theresa Shelton

Kathy Miks

More money isn’t

necessarily the answer to the problem. Even District staff admit

that.

Yet, Parker, Varda

and Reed want people to believe that repealing TABOR and eliminating

the BS factor will solve all of the the District’s problems. They

want people to believe that paying the same teachers even more money

will somehow, miraculously, improve education in Jeffco. They want to

“keep Jeffco strong”, when in fact Jeffco isn’t strong and has

been on a downward trend for years. They have their heads buried in

the sand.

Jeffco needs change.

Parker, Varda and Reed are not going to provide that change.

Jeffco's Capital Improvement Program is currently $110M over initial cost estimates

Recently, Colorado Community Media, including Jeffco Transcript and Arvada Free Press printed an article by writer Bob Wooley about Jeffco’s Capital Improvement Program.

For

the most part, Wooley did a good job of attempting to explain a

financially complex program. However, there were some comments and

statements made by Jefferson Public Schools’ officials that were

misleading or downright false.

I’ve

outlined several of those areas below:

1.

The article states:

After

the Bond passed, the project’s estimated costs were increased by

nearly $32 million for a revised total of just under $737 million for

the program.

TRUE

– $32M

in hidden

costs were added to the program

After

the bond passed, $32M in costs were added to the flipbook for

the same list of projects.

The

use of $32M in contingency to

cover these costs was

essentially hidden.

2.

The article states:

District

officials say the increase was a result of changes in scope, market

conditions, incorrect estimates or various other factors like

asbestos removal, which were determined once the District was able to

perform more in-depth evaluations of each individual project.

While I agree that factors such

as scope changes, market conditions and incorrect estimates can

result in changed estimates, that doesn’t fully explain the extent

of the cost estimate changes between the first and second flipbooks.

The project costs for 81 schools, or nearly 60% of the total,

increased by EXACTLY 5%. This is not indicative of changes in

scope or incorrect estimates. That’s indicative of using Excel to

pad costs.

3.

The article states:

“We

told voters we would accumulate six

years of approximately $20 million

at the back-end to fill up the program,” Reed says.

FALSE

– Voters were told $23M

Voters

were told that exactly

$23M

annually in Capital Transfer would be accumulated. In reality only

$20.9M

annually is currently being transferred. That means

there is a

$12.6M shortfall in

stated revenue, again made up with Contingency.

4.

The article states:

“and

over $3.5 million was spent on hazmat expenses (which technically, do

not count as overages).”

FALSE

– Hazmat

costs ARE overages

Why

aren’t $3.5M in hazmat expenses considered overages? Any

decent construction project manager with 50 year old buildings

knows there is asbestos in those

buildings that will have to be mitigated. Mitigation costs should

have been factored into the original estimates.

Where

is the money coming from to pay for the hazmat expenses? It’s

coming from the District’s program contingency. Therefore,

technically, and for all intents and purposes, hazmat expenses are

program costs that reduce available contingency This is merely an

attempt by Reed to put lipstick on a pig to make $3.5M in overages

not seem like the $3.5M in overages hazmat costs really are.

5.

The

article states:

In

a document Reed says is now posted to the Capital Asset Advisory

Committee (CAAC) website, all budget variances are listed with

specific overage amounts and the reason for the cost variance.

FALSE

– This

document

lists variances against revised cost estimates, not original

estimates

This

document hides $32M in cost increases. That’s deception.

6.

The article states:

Therefore,

the precise amount of contingency that’s been spent on actual

projects thus far is $65,815,424.

FALSE

– The amount of contingency allocated is currently over $110M

$65M

from what Reed wants people to believe is the contingency spent, plus

$3.5M in hazmat, plus $32M in increased estimates plus $9M from

recent fields project = $110M in contingency allocated.

7.

The article states:

“I’m

not a construction guy,” Bell said. “But we have a construction

guy and I was speaking to him this morning and he said “you know, a

year ago the cost of steel was $53 a ton — today it’s $79.” A

year ago did anybody know it was going to go from $53 to $79? No.”

MISLEADING

– Cost of steel is only one small component of cost increases

Both Tim and Steve have told the Board on several occasions that they have been getting good pricing due to the pandemic. And, this report shows that non-residential construction costs have been relatively flat in Denver for the last 2 years, increasing by only 2.1% total over that time. In addition, there are numerous projects that had no steel involved that are significantly over budget. This is a misleading and deceptive statement.

8.

The

article states:

“According

to Tim Reed, Jeffco’s Executive Director Facilities &

Construction, the amount of contingency that had been spent as of

Feb. 22, was just over $81 million, of which nearly $12 million went

to charter schools…”

MISLEADING

to FALSE – $12M to Charters came from Bond Premium

The

agreement with District Charters was that Jeffco would share

approximately 10% of all bond proceeds with Charter schools. The $12M

Tim Reed is referring to is based on Charters’ share of accrued

interest and bond premium. This has nothing to do with District

contingency.

The

bottom line is that the Capital Improvement Program has already

spent

or allocated $24M over its original $86M contingency budget ($110M

total) only

2.5 years into the program. In addition, Jeffco has hidden

a $12M revenue shortfall from

Capital Transfer.

The

amount

of deception and lack of accountability for large cost increases is

truly unbelievable.

Where is the promised annual independent audit of Jeffco's Capital Improvement Program?

To assure voters

that the $705M 2018 bond program would be well managed, Jeffco wrote

into the ballot language that the program would be subject to an

“annual independent audit”. The implication being that the

program would be scrutinized on a yearly basis by a firm without

financial ties to the District. Yet, two and a half years into what

is now an $832M program only a very basic financial audit has been

conducted, by the same firm that has deep and long standing ties to

the District.

The ballot language

implied that voters would get more than that. Now, with multiple

questionable practices and current cost estimates $110M over what

were presented to voters, Jeffco’s staff, Board and CAAC have all

balked at providing the transparency and accountability that we all

thought we would get when we entrusted Jeffco with our money. It is

just incomprehensible to me that there is so much resistance to

providing the transparency that was promised. It seems that if there

was nothing to hide a Performance Audit would give the program a

clean bill of health and end, once and for all, all questions. By

continuing to refuse to conduct a Performance Audit it only

perpetuates the assumption that there really is something to hide.

That is not a good look!

In addition, the

highly touted Citizens’ Capital Asset Advisory Committee is not

doing its job either. CAAC meeting notes reveal that only until

recently they have remained silent and allowed the program to go

tens of millions of dollars over budget without asking any questions

whatsoever. They have provided poor oversight of our money.

After initially observing a high usage rate of program contingency funds and subsequently numerous other instances of extremely questionable observations regarding the transparency, management and fiscal practices of the program I sent an email

to members of the CAAC on November 24, 2020 highlighting 10 very specific instances which raised questions with the management and transparency of the program and urging them to call for a Performance Audit conducted by a truly independent firm. Tim Reed replied on December 10, 2020 and I sent a rebuttal to Tim’s response to members of the CAAC on January 4, 2021.

On each of my letters I clearly include an offer to discuss my concerns and my telephone number. The fact that no one has taken me up on my offer speaks loudly in and of itself.

Finally, on January 4, 2021 I sent a copy of my original letter to the CAAC, Tim Reed’s response and my rebuttal to the Board of Education

The Board of Ed Secretary’s reply was far from confidence building:

Dear Mr. Greenawalt,

Members

of the Board of Education received your January 4, 2021 email

correspondence regarding our Capital Improvement Program. Thank you

for bringing your concerns forward. You are correct that the Board of

Education will be receiving feedback from the Capital Asset Advisory

Committee and your concerns are noted.

Sincerely,

Stephanie

Schooley

Secretary,

Jeffco Public Schools

with no further

communication from the Board.

Over a series of

posts I will outline some of the issues I have seen with regard to

the transparency and fiscal management of the 5B bond program and

take a look at some of the unbelievable and incredulous responses Tim

Reed provided in a weak attempt to address my concerns. Here are some

of the topics that I will cover:

Over budget

($57M as of November 2020)

Projected

$32M Contingency Shortfall

Deceptively

adding $31M to Flipbook costs

Failure to

Share Bond Premium with Charter Schools

Out of Scope

Projects

Deceptively

Hiding the True Cost of Alameda HS Cost Overruns

Recent Large

Underspend on FF&E Projects

Unexplained

Recent Increase to Capital Transfer Revenue

Questionable

Use of $50M in Bond Premium Contingency

Failure of

CAAC Members to Maintain Independence

Failure of

Jeffco to Provide $23M in Capital Transfer as Promised to Taxpayers

Jeffco needs to put

these concerns and questions to rest.

Jeffco needs to

conduct the independent Performance Audit that voters thought they

were going to get.

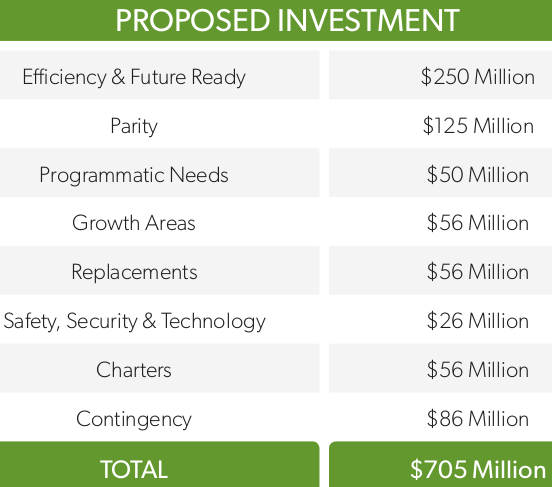

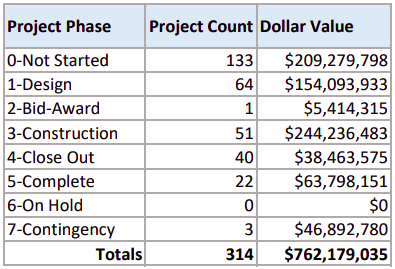

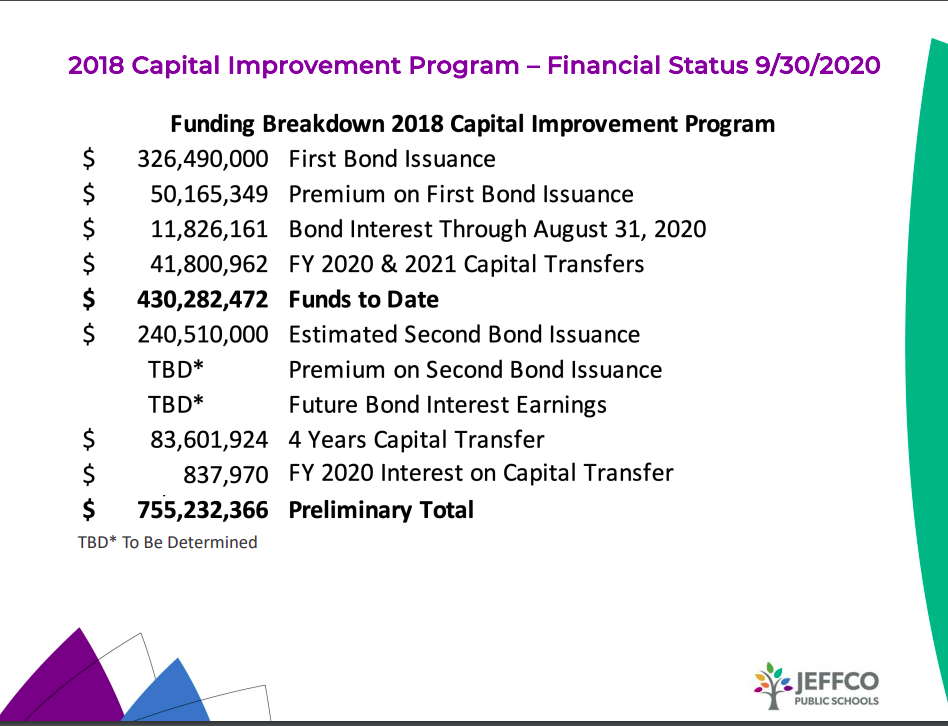

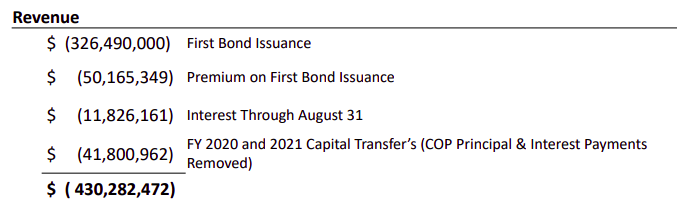

1. $57M over budget. On its own, a program that is $57M over budget less than 2 years into a 6 year plan should automatically trigger a Performance Audit. Just to recap, voters were told the Capital Improvement Program would cost $705M. At the CAAC’s last meeting in November, it had a $762,179,035 price tag.

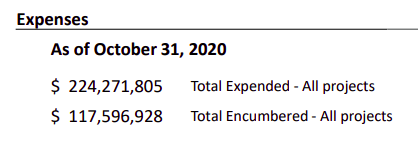

2. Projected $32M Contingency Shortfall. At the October 7th Board Study Session, Tim Reed told the Board that $68M in contingency had been used to date.

At the CAAC’s November meeting Tim presented the following numbers for funds Expended and Encumbered, totaling $341M.

Subtracting the $68M of contingency from this value means that $273M of the $595M in total program costs are currently Expended or Encumbered, leaving $322M in remaining projects. If that same rate of contingency usage continues, that would require remaining contingency of over $79M. Yet, there is only $47M in contingency remaining, a $32M shortfall.

Do the math. The numbers don’t lie. This is not a healthy Program.

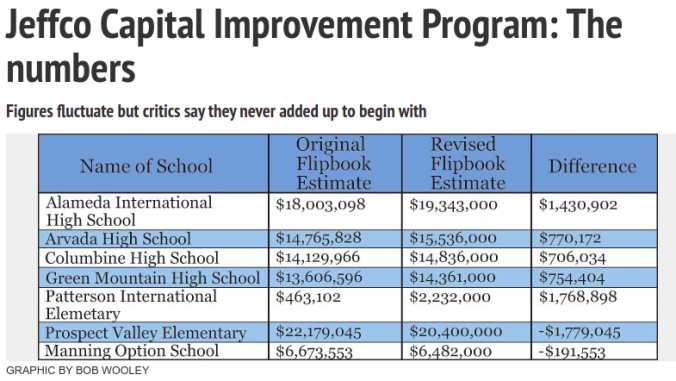

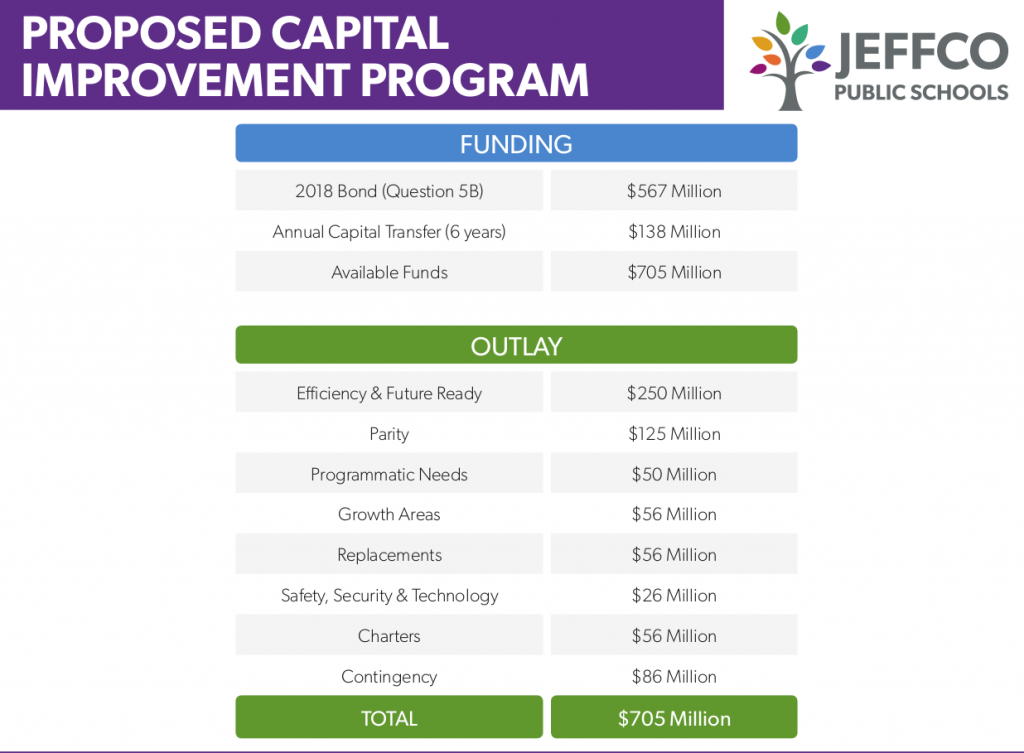

3. Deceptively adding $31M to Flipbook costs. District project costs were presented to voters as $563M. You can arrive at that number by subtracting the Charters $56M and the Contingency $86M from the Flipbook presentation.

This can be verified by adding the costs of individual projects in

the original Flipbook (Plus approx. $17M in costs for Trailblazer,

North Transportation Hub, OELS and Preschools projects which were

withheld from voters).

However, sometime after the Bond passed, the District changed the

Flipbook. The cost of nearly every project increased. Here are some

examples:

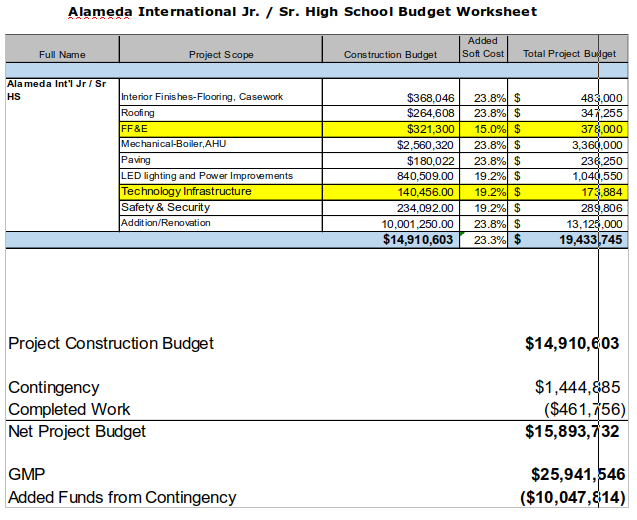

Alameda HS – an increase of $1,430,902 to $19,434,000

Green Mountain HS – an increase of $754,078 to $14,361,000

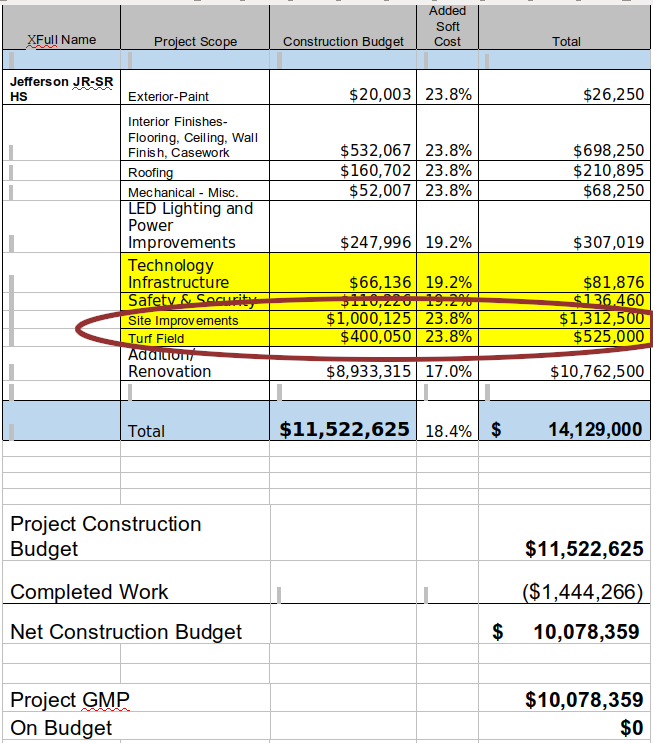

Jefferson Jr/Sr HS – an increase of $672,810 to $14,129,000

This had the net effect of raising BASE costs by a total of

$31,967,419. Essentially hiding $31M of cost increases.

For example, when the construction budget for Alameda was presented to the Board, contingency usage of $10,047,814 was based on the updated Base cost of $19,433,745, instead of the original cost estimate of $18,033,098. This usage of the revised cost estimate deceptively hid the totality of the increase, and the additional use of Contingency, of $1,430,902.

Therefore, cost estimates for all projects have now increased by

$100M; the $68M in Contingency that Tim Reed freely told the Board

PLUS the $31M in hidden cost estimate increases.

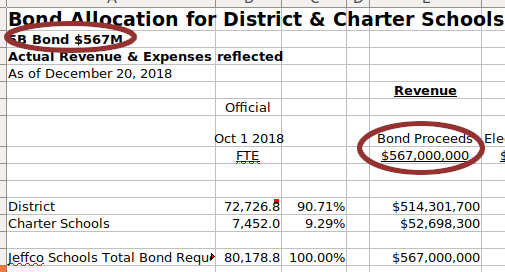

4. Failure to Share Bond Premium with Charter Schools. As recently as of the end of October, the District still had not shared Bond Premium with Charter schools, in violation of the Board’s October 2018 Sharing Resolution. The District spreadsheet widely circulated to Charter Schools show that the District only calculated sharing revenue based on the Bond par of $567M.

Yet, at the November 11th Board Study Session, Steve Bell told the Board that Bond Premium is shared with Charters.

Therefore, at this point, Charters are owed approximately $4.6M, PLUS interest – which will subsequently reduce the Contingency available for District projects by a corresponding amount.

Brian Ballard, Chair of the District’s Financial Oversight

Committee, has said that it is the CAAC that has responsibility for

overseeing 5B Bond funds. If that is the case, why hasn’t the CAAC

ensured that District Charters have been given their complete share

of the funds?

5. Out of Scope Projects. There are multiple projects that can be identified that were not in the scope presented to voters. Several easily identifiable, high-cost projects include: Ralston Valley HS Roof, Lakewood HS Track, West Jefferson MS Track, etc. The following images were taken from the Original Flipbook presented to voters and clearly do not show these projects.

Was there any discussion relating to the addition of scope and

reduction of contingency for these and other added scope projects?

What was involved with this process? Were these prioritized over

replacement schools? Was there a vote?

6. Deceptively Hiding the True Cost of Alameda HS Cost Overruns. Similar to Jefferson Jr/Sr HS, Alameda HS is slated for Track and Field Upgrades. When the Jefferson project was submitted to the Board for approval, the Track and Field upgrades were included in the project costs and subtracted from the remaining budget.

This was not the case when Alameda was presented to the Board. The cost for the Track and Field upgrades were left off of the presented costs, effectively deceiving the Board that total overages are at least $1.5M over what was shown. Was that intentional deception, or merely incompetence?

7. Recent Large Underspend on FF&E Projects. We all like to get good deals. However, the cost savings on several recent FF&E projects go beyond the definition of good deals, suspiciously into the realm of scope reductions. Look at some of the “savings” generated from some of these FF&E projects that were recently presented to the Board, $150k, $300k, $315k and $310k.

These “savings” are 47%, 22%, 60% and 66% less than the original

cost estimates. That’s far more than a reasonable person would

expect from a “good” deal. What happened here? Was scope cut at

these schools?

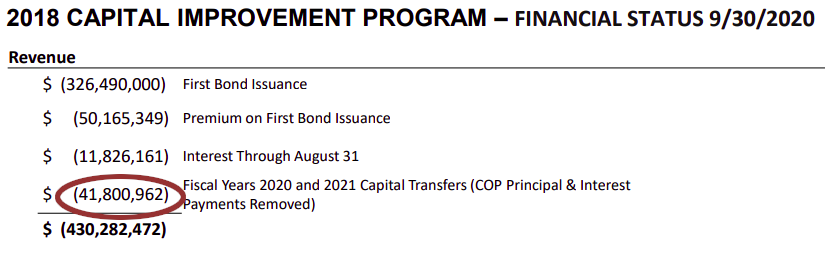

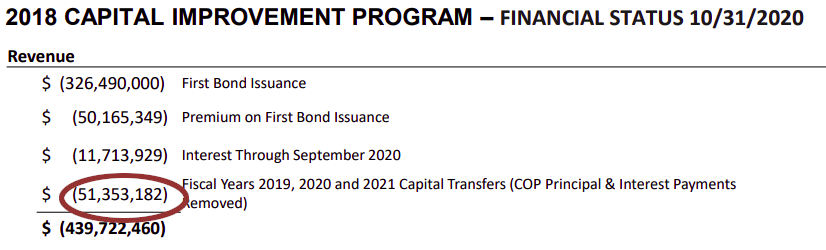

8. Unexplained Recent Increase to Capital Transfer Revenue. At the October CAAC meeting, members were shown Capital Transfers into the Capital Improvement Program of $41.8M. Yet, in November, they were shown $51.3M. Where did that additional $9.5M come from?

(On a side note, how does Interest Revenue DECREASE by $110,000 from August to September? Can you trust any numbers that are presented?)

Approximately $3M appears to come from the movement of the contingency in prior capital improvement programs such as 18M and 19M. This contingency decrease can be seen in documents presented to the CAAC.

But, the source of the remaining $6.5M is unexplained as the value of

the 18M, 19M, 20M programs remain the same. And this happened mere

days after Steve Bell told the Board that the capital transfers would

be $20M/year over 6 years for a $120M total.

9. Questionable Use of $50M in Bond Premium for Contingency. Recently, Tim Reed and Steve Bell told the Board that during initial 5B discussions the bond ask amount was decreased and 2 replacement schools were removed from the list of projects.

If this was the case, why then, when the District received $50M in bond premium, weren’t replacement schools immediately added to the list of projects? Instead, it appears that the $50M in bond premium has merely been added to the $86M already allocated to program contingency. What was the process in determining that the additional $50M in contingency should be used for contingency instead of being used for replacement schools, particularly when taxpayers voters were told that Jeffco had $1.3B in deferred maintenance needs?

10. Failure

of CAAC Members to Maintain Independence. Tim Reed

recently sent members of the CAAC a document relating to the Purpose

and Membership of the committee. This document clearly states that

members must be:

Independent and free from any relationship that would interfere

with independent judgment

Gordon Callahan, a CAAC member, has a relationship with the District.

His firm has been the recipient of nearly $1M in contracts over the

past year and a half.

This is not the appearance of independent judgment.

For taxpayers to fully trust the Capital Asset Advisory Committee ALL members of the committee must be completely independent and free of District relationships. Unfortunately, that is not currently the case. His continued membership on the committee is ethically questionable and erodes taxpayer trust.

Jeffco schools failed to share all 5B bond proceeds with District Charter schools

As we saw in Part II, Jeffco’s Board of Education unanimously adopted a Bond Proceed Sharing Resolution that clearly states “the Board of Education will allocate a percentage of the bond proceeds equal to the percentage of full-time district students enrolled in district-authorized charter schools”.

Yet, Jeffco did NOT allocate ANY of the bond premium to District Charters. That was a loss of at least 9.29% of the Bond Premium of $50M or $4,660,360. If the share percentage was calculated correctly with 2019 student count numbers as explained in Part II, that revenue share loss is $4,745,642.

Why didn’t Jeffco schools share the Bond Premium? We weren’t part of the conversations and no discussion took place at the Board table, but we can only surmise that Jeffco is attempting to make a distinction between Bond “proceeds” and Bond “premium”, essentially saying that the bond premium is not part of the bond proceeds in order to keep the $4.7M for District projects.

That is just plain wrong!

While this attempted distinction has worked to silence the meek District Charter schools who are afraid of losing their Charter authorizations, the District knows that the IRS does not make that same distinction.

Sale proceeds means any amounts actually or constructively received from the sale of the issue, including amounts used to pay underwriters’ discount or compensation and accrued interest other than pre-issuance accrued interest. Sale proceeds also include, but are not limited to, amounts derived from the sale of a right that is associated with a bond, and that is described in 1.148-4(4). See also 1.148-4(h)(5) treating amounts received upon the termination of certain hedges as sale proceeds.

Jeffco agrees with this definition as in a May Alameda presentation to the BoE, Tim Reed included the Bond Premium in his calculation used to determine arbitrage requirements.

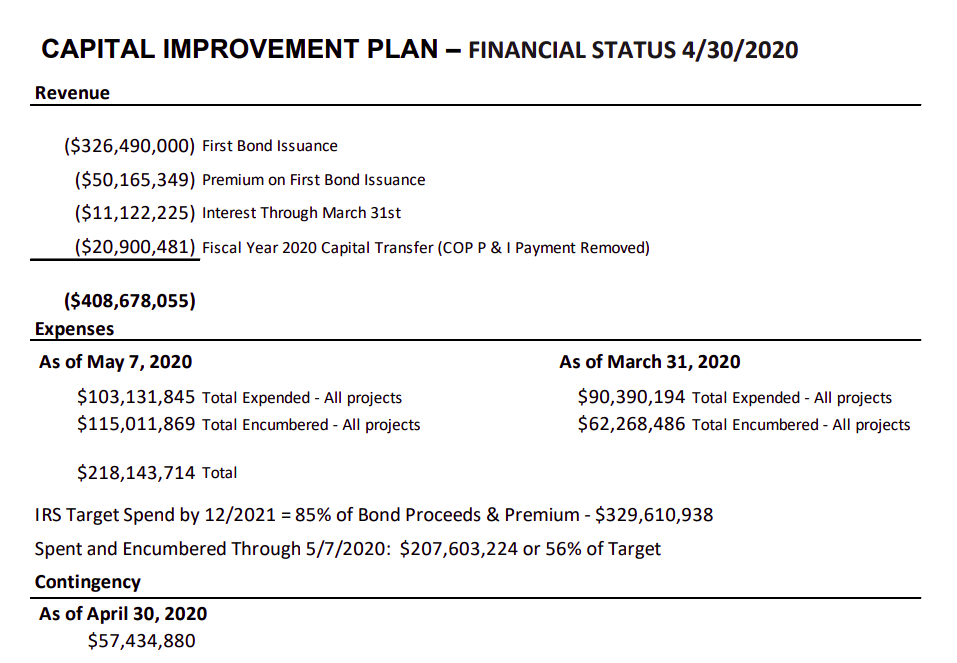

IRS Target Spend by 12/2021= 85% of Bond Proceeds & Premium $329,610,938

It is obvious that Jeffco knows that the IRS considers Bond Premium to be part of Bond proceeds.

Therefore, Jeffco has violated its own Sharing Resolution and defrauded the District Charters of over $4.6M by not sharing all of the Bond Proceeds, in this case the Bond Premium, with them.

In essence, Jeffco got the Charters to support, and campaign for, 5B, but in the end isn’t holding up its end of the bargain.

Shame on Jeffco schools!

10 Things we learned from Jeffco Schools Board Study Session on 5B Bond

Here are the 10 things we learned from the October 7, 2020 Jeffco Board Study Session on the District’s Capital Improvement Program.

None of these things is good!

1. HS Parity – We were told during the Wednesday meeting that one of the goals of the bond program was to achieve High School building parity. Someone might want to tell the staff, parents and students at Pomona, Wheat Ridge, Arvada and Green Mountain that. Even after the program finishes, these schools will still have Facility Condition Indexes above 15% while schools such as Bear Creek, Golden, Arvada West and Lakewood will have FCIs below 4%. That’s not parity/equity in my mind. Once again, Jeffco talks equity, but never, ever delivers.

2. Capital Transfer – We learned that in 2 years Jeffco has transferred $41.8M from general funds to the Capital Program and that over the next 3 years another $83.6M will be transferred for a total of $125.4M.

But, Steve Bell made that sound worse by stating that only $120M in total would be transferred over 6 years.

Jeffco voters were promised $23M/year would be transferred for a total 6 year transfer of $138M.

This is now an expected shortfall of $12.6M. This shortfall will need to be made up by either allocating contingency or reducing project scope. I don’t even think that the Board is aware of this shortfall at this point. Bell and Reed will use Wednesday’s presentation to say that they informed the Board, but this is a pretty weak argument. In reality, it was the CFO’s job to ensure that 2019-20 and 2020-21 budgets presented to the Board of Education included transfers of this promised money, OR, to inform the Board of Education of this shortfall. The former CFO Kathleen Askelson failed to do either. She failed in her fiduciary responsibilities to both taxpayers and the Board. It’s no wonder she suddenly decided to leave Jeffco. Once this came to light she should have been fired.

3. 19M Projects – During the meeting Reed casually mentioned that $9.5M worth of projects were transferred from the District’s 19M facilities maintenance program to the Bond program because they were ready to go and it would assist in meeting the arbitrage requirements of the bond.

What he failed to say was that these projects were funded straight from the contingency of the Capital Improvement Program and that this was in reality an increase of scope. Complete and utter deception on the part of Reed and Bell.

4. Missing $41M – $41M is missing from Bell and Reed’s presentation. Where is that money? Jeffco voters were told that the program came with $86M in contingency built into it (see image above). $50M was added through bond premium and another $12M added through interest.

That’s a total of $148M above and beyond the $563M in project cost estimates presented to voters. Reed and Bell told the Board that they are carrying $107M in program contingency.

In that case, where did $41M go?

$ 86M in

contingency presented in original Flipbook

+$ 50M in bond

premium

+$ 12M in interest

=$148M total available above cost estimates

– $107M in stated

contingency

=$ 41M missing

5. % of contingency usage – Bell told the Board that $68M in contingency has been spent (video above). That contingency was spent during the completion of $264M ($332 expended and encumbered from Board docs – $68M in contingency used) in project work. Since there is (now) $594M in total work that needs to be completed for the program that means 44% of the total program work has been done against 64% of the total contingency ($68M of $107M in total contingency). At the current rate, available contingency will be used before all projects are completed and scope will have to be reduced. Calculated a different way, continuing to use contingency at the current rate would mean that Jeffco needs $153M in total contingency, $46M more than what is currently allocated. This is not a good position to be in.

6. Construction increases – We learned that there are several Board member apologists who want to blame inflation and the length of the program (6 years) for cost overruns. I don’t agree with that. A timeline for project work was clearly laid out in the Flipbook. District staff knew when projects would be worked on and SHOULD have incorporated inflation based increases into their cost estimates. If they didn’t do that, then they are incompetent and should be fired, not given a free pass as Rupert and Mitchell want to do. Besides, Jeffco is only 2 years into the program. Inflation based cost increases shouldn’t be responsible for over $68M in cost increases at this point.

7. Contingency use between May and September – In May Reed told the Board that there was $57M in remaining contingency.

May Contingency

Since that time the Board has approved approx. $11M in contingency usage, mostly at Alameda. Now, Reed is now telling the Board that there is only $37M in contingency remaining. What did that additional $9M in contingency get used for in such a short period of time? Where did it go in only a few short months without Board knowledge?

8. Questions about use of $50M bond premium – The bond premium was a bonus. In my mind, it should be used to provide real value to the taxpayers. During the meeting Reed told the Board that to get the total bond package down to something reasonable for taxpayers for the 2018 vote they had to remove two replacement schools.

Now, when Jeffco received bond premium, why did $50M just get consumed to pay for added contingency? Why weren’t 2 replacement schools added into the program? This is pure mismanagement and an atrocious use of taxpayer money. People should be fired for using $50M this way!

9. Where was the Citizens Capital Asset Advisory Committee? Members of the CAAC were supposed to be at the meeting to answer questions regarding their oversight and monitoring of the program. They are definitely aware (here and here) of the depth and degree of the $100M in cost overruns to date. It is suspicious that at the last moment they decided not to show up.

10. Board President Harmon and Directors Rupert and Mitchell will go to great lengths to cover-up waste and mismanagement and protect the District from criticism or scrutiny. When Director Miller brought up questionable practices regarding the use of the $50M bond premium, instead of addressing that issue first, Harmon attacked Director Miller and then Rupert and Mitchell went into a full on defense of the District. It’s not their money, so why should they care?

This Wednesday’s

study session was enlightening, to say the least. It raised, and

never answered, numerous questions regarding the management of a $3/4

Billion Capital Improvement Program. The degree of deception on the

parts of Reed and Bell is just unbelievable.

The Program is a

disaster – way over budget and heading further in that direction.

That is not how you get taxpayers to approve your next bond request.

It is clearly evident that, as promised to taxpayers, a full and complete performance audit on the program must be conducted immediately!

Jeffco manipulated student count numbers to short-change Charters

The Board of Education’s Bond Revenue Sharing Resolution clearly states that “the Board of Education will allocate a percentage of the bond proceeds equal to the percentage of full-time district students enrolled in district-authorized charter schools”.

A reasonable person would have read this resolution at face value and come to the conclusion that the percentage would have been calculated based on the count of full-time enrolled Charter students divided by the count of total full-time enrolled District students. In fact, a spreadsheet presented to Charter schools (attached) to show how the distributions were calculated clearly displayed the following text referring to FTE (Full time Equivalent) in 2 locations:

1. Official Oct 1

2018 FTE

2. Note: October 1,

2018 Official FTE count (audited)

Yet, the District did not use FTE numbers. In its calculations, the District actually used the state calculated Funded Student Count numbers for total District student count number, which is higher. This effectively increases the denominator for the percentage calculation and reduces the Charters’ shares. State Funded student count numbers are higher because, in an environment of decreasing student enrollment, the state reduces impact of revenue decreases by computing a 5 year average of student enrollment. For the school year 2018-2019 this increased the total District funded student count number by 1,397 and resulted in a loss of nearly $1M to Charter schools.

Not only did the

District perpetrate this loss of agreed upon revenue to District

Charters, but they

Charter parents

campaigned very hard for a Bond that barely passed. How short-sighted

is it of Jeffco to not see this? I doubt Charter parents will be as

willing to expend as much effort and energy the next time Jeffco

wants to pass a bond when Charters will know that Jeffco will be out

to take advantage of them.

Jason Glass and

Jeffco Schools promised transparency when they put a $567M Bond to

the vote of taxpayers in 2018.

To great fanfare, Glass rolled out what was called a Flipbook that explained sources of revenue for the District’s 6 year Capital Improvement Program and exactly how much would be spent at each school.

There was one big problem though. The Flipbook did NOT show where nearly $17M in bond proceeds would be used. I even wrote about it in October 2018 – http://improvejeffcoschools.org/index.php/2018/10/ A year and a half later, through CORA requests, I’ve been able to piece together the uses of that $17M, now blossomed to over $19M, in spending:

Project

Est. Cost

North Transportation-Joyce Renovation

$349,400

Trailblazer Stadium

$4,415,250.00

581 Conference Place Reopen

$518,877.00

Mount Evans OELS Efficiency

$3,210,190

Windy Peaks OELS Efficiency

$3,340,982

Anderson Preschool Efficiency

$117,794

Irwin Preschool Efficiency

$48,935

Free Horizon Montessori

$174,682

Litz Preschool Efficiency

$77,479

North Transportation-Site Acquisition

$7,000,600

Total

$19,254,189

In looking at this

list, one can only guess at why these projects were not shown to

taxpayers – most are not directly related to schools. Trailblazer

stadium, North Transportation Site, 581 Conference Place – these

are not projects that would have encouraged me to vote Yes on the

Bond.

Even when asked a

question on his much touted Jeffco Generations Facebook page, Glass

failed to answer a question regarding the missing projects.

And, the most egregious thing was that shortly after the Bond was approved by taxpayers the Flipbook was quietly updated. Cost estimates increased from $563M to $594M, an increase of $31M in cost estimates.

Here are several examples of how project costs changed (you can see the complete list here):

School

Original Flipbook

Revised Flipbook

Difference

Alameda HS

$18,003,098

$19,434,000

$1,430,902

Patterson International ES

$463,102

$2,232,000

$1,768,898

West Jefferson Middle School

$2,323,535

$3,700,000

$1,376,465

Powderhorn Elementary

$5,756,358

$6,100,000

$343,642

Not only is there not a corresponding increase in revenue to fund these increases, but the impact of the changes turns out to be extremely important in the on-going deception of hiding the degree of cost overruns, which I will discuss in a future post.

The deception to

taxpayers regarding 5B funding and projects started early and appears

to be well thought out – not something that should be done if

Jeffco wants to get another Bond approved in the future.